A self-directed 401(k) is an employer-sponsored retirement savings plan that allows employees more freedom in their investment choices. It has many similarities with standard 401(k) plans but comes with more investment alternatives and additional guidelines. Regular 401(k) plans typically offer mutual funds, bonds, and stocks as investment choices. Meanwhile, self-directed 401(k)s allow employees to invest in more unorthodox items like real estate, precious metals, foreign currency, tax liens, equipment leasing, and private placements. Employees who choose to have a self-directed 401(k) can personally make the buying and selling decisions for their accounts. However, the transactions will be executed for the employee by their administrator, who is a qualified custodian from an investment firm or a brokerage. Self-directed 401(k)s offer both a traditional (pre-tax) and Roth (after-tax) option. This article will focus on the pre-tax, traditional version of the self-directed 401(k). Self-directed 401(k) plans have the same contribution limits as standard 401(k) plans. Both plans have an employee contribution limit of $22,500 in 2023, which has increased to $24,000 in 2024. Older employees aged 50 and above are entitled to make catch-up contributions of up to $7,500. Aside from this, employers can contribute more to their employee’s retirement plan, provided it does not exceed the total contribution limit when added to the employee’s contributions. The total contribution limit for the self-directed 401(k) and the standard 401(k) in 2023 is $66,000 or $73,500 for those 50 and older. This has increased in 2024 to $69,000 or $76,500, respectively. The withdrawal and rollover rules for self-directed 401(k) plans are the same as those for standard 401(k) plans. Both these plans were funded with pre-tax dollars. This means that contributions will grow on a tax-deferred basis, but most withdrawals are expected to be taxed. According to the Internal Revenue Service (IRS) guidelines, if an employee makes a withdrawal before the age of 59½, they will have to pay a 10% penalty on top of the deferred taxes. There are some exceptions to this rule, such as when an employee needs to take a hardship distribution. Employees also have 60 days to roll over a self-directed 401(k) plan to an Individual Retirement Arrangement (IRA) before the money withdrawn becomes tagged as a taxable withdrawal. With all of these rules to consider, individuals may seek advice from their custodian if they hope to process a tax and penalty-free rollover. Despite the relative freedom that a self-directed 401(k) brings, individuals still have to be careful not to engage in prohibited transactions, or they will lose their account's tax privileges. The following are some of the transactions that are considered prohibited by the IRS: Disqualified persons are individuals or groups who provide services or have a financial interest in the plan. This includes family members and account beneficiaries such as spouses, parents, grandparents, children, and grandchildren, It also includes the plan owner and anyone else who would financially benefit from the plan's success, such as the plan's custodian, administrator, or any company over which the plan owner has voting rights. If found to have participated in prohibited activities, the retirement plan will no longer enjoy tax benefits. Instead, all investments will be taxed immediately. In addition, disqualified persons who engaged in these activities will also be asked to pay a separate tax. Self-directed 401(k)s are appealing to some individuals for the following reasons: Like any retirement program, self-directed 401(k)s also have their drawbacks, which include: Individuals who wish to set up a self-directed 401(k) account may follow these steps: A self-directed 401(k) is an employer-sponsored retirement savings plan that allows employees more freedom in their investment choices. In addition to the mutual funds, bonds, and stocks offered by standard 401(k)s, self-directed 401(k)s allow employees to invest in more unorthodox items like real estate, precious metals, foreign currency, tax liens, equipment leasing, and private placements. Employees who choose to have a self-directed 401(k) can personally make the buying and selling decisions for their accounts. However, the transactions will be executed for the employee by their administrator, who is a qualified custodian from an investment firm or a brokerage. Self-directed 401(k)s have many similarities with standard 401(k) plans, including contribution limits, withdrawal rules, and rollover processes. However, it comes with more investment alternatives and additional guidelines on prohibited transactions. This type of plan has its benefits and drawbacks. Some advantages are enjoying pre-tax savings, having more control over investment decisions, and getting broader investment choices. The disadvantages include paying more fees, complicated transaction rules, and needing to allot more time and gain more expertise. If you are undecided about whether or not to avail of the self-directed 401(k) option, you may consult with a financial advisor who can guide you through your decision-making process.What Is a Self-Directed 401(k)?

Self-Directed 401(k) Contribution Limits

Self-Directed 401(k) Rollovers and Withdrawals

Prohibited Transaction Rules in a Self-Directed 401(k)

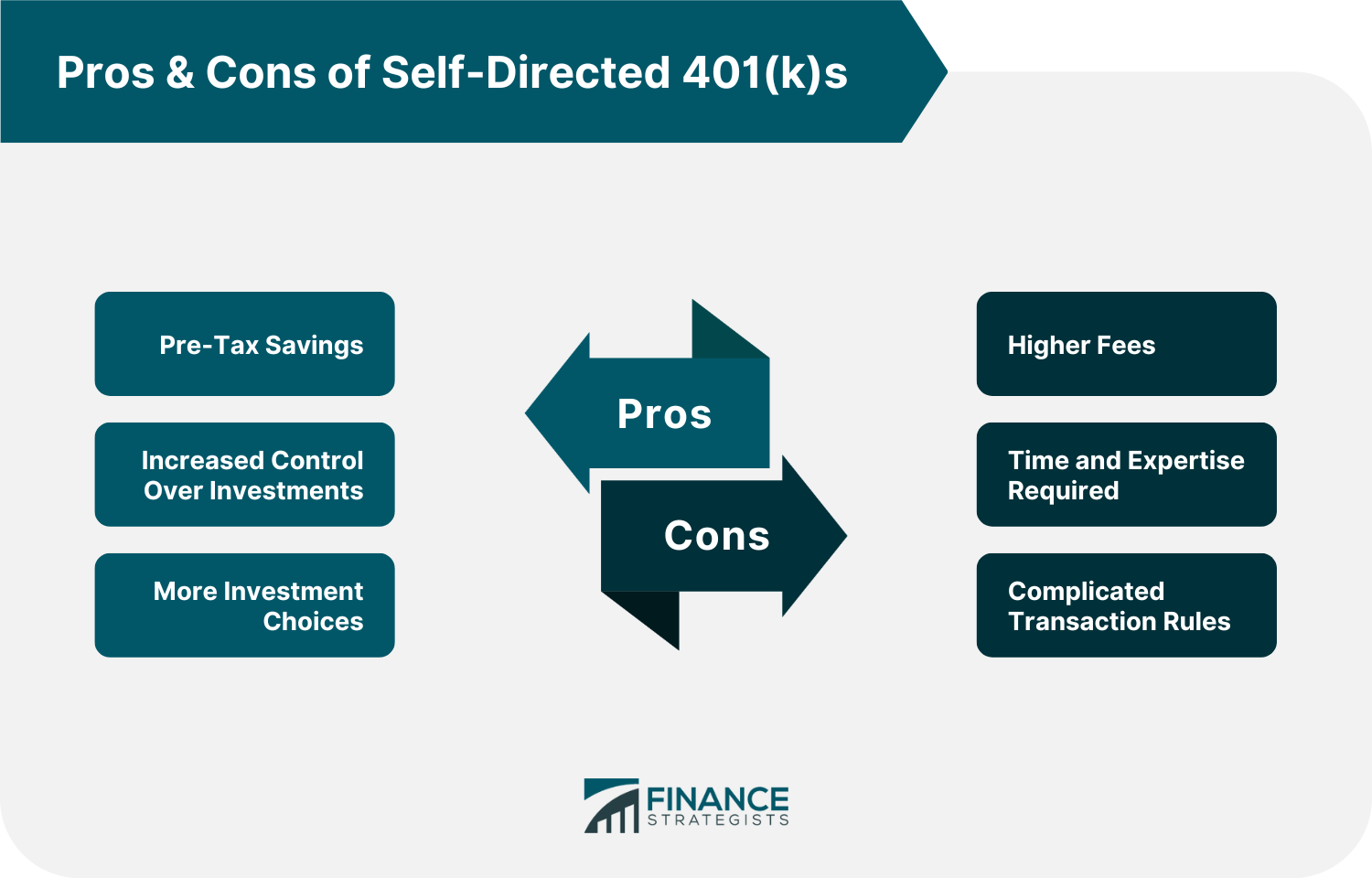

Benefits of Self-Directed 401(k)

Drawbacks of Self-Directed 401(k)

How to Set up a Self-Directed 401(k)

Final Thoughts

Self-Directed 401(k) FAQs

A self-directed 401(k) is an employer-sponsored retirement savings plan that allows employees more freedom in their investment choices. It has many similarities with a standard 401(k) plan, including contribution limits, withdrawal rules, and rollover processes. However, it comes with additional guidelines on prohibited transactions.

Aside from mutual funds, bonds, and stocks, self-directed 401(k)s allow employees to invest in unorthodox assets like real estate, precious metals, foreign currency, tax liens, equipment leasing, and private placements.

A self-directed 401(k) is an employer-sponsored retirement savings plan that allows employees more freedom in their investment choices. In contrast, the solo 401(k) is a retirement plan designed for an individual business owner who does not have any employees.

Self-directed 401(k)s have an employee contribution limit of $22,500 in 2023, which has increased to $23,000 in 2023. Older employees aged 50 and above are entitled to make catch-up contributions of up to $7,500.

Aside from employee contributions made through salary deductions, self-directed 401(k)s may be funded through transfers from other retirement plans except for Roth IRAs. They may also be financed by employer contributions, which are done through their matching or profit-sharing.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.