A 401(k) plan is a retirement savings plan sponsored by an employer. Employees can contribute a percentage of their pretax income to the account, up to a limit set by the Internal Revenue Service (IRS). The contributions are not taxed until they are withdrawn from the plan. Employers often match a portion of employee contributions. Have questions about 401(k) plans? Click here. There are several different types of 401(k) plans: A traditional 401(k) is the most common type of 401(k) plan. Contributions are made with pre-tax dollars, and earnings grow tax-deferred. When you withdraw money from the account, you will pay taxes on the withdrawals. This type of plan offers a wide range of investment options to employees. Employers in this type of plan make matching contributions. A Roth 401(k) is a newer type of 401(k) which is closely the same as a traditional 401(k) except for a few things. Contributions are made with after-tax dollars, but earnings grow tax-free. When you withdraw money from the account, you will not pay taxes on the withdrawals. A Safe Harbor 401(k) plan is similar to a traditional 401(k), but it offers more protection for the employer. Employers are no longer required to pass the nondiscrimination tests each year to offer them. This type of plan may be offered by public or private employers regardless of size. Employers are mandated to make a contribution to the plan either on a matching or nonelective basis with certain limits set by the IRS annually. A SIMPLE 401(k) stands for Savings Incentive Match Plan for Employees. It is similar to a traditional 401(k), but it sets a much lower limit on contributions and allows employees to save more money. Employers must offer matching contributions of up to 3 percent of an employee's salary or make non-elective contributions equal to 2 percent of each eligible employee's salary. Businesses with less than 100 employees can offer this type of 401(k) plan. Employee contributions are made using pre-tax dollars and any qualified withdrawals made shall be taxed at the ordinary income tax rate of the employee. A Solo 401(k) plan is a variant of a traditional 401(k) used by self-employed individuals and small business owners without any employees other than themselves. Contributions made into the plan are tax-deductible and any qualified withdrawal shall be taxed using the employee's ordinary income tax rate. 401(k) plans are a great way to save for retirement. Employees can contribute a percentage of their pretax income, and employers often match a portion of employee contributions. There are several different types of 401(k) plans available, each with its own set of benefits and restrictions. It is important to understand the differences between these plans so you can choose the one that is best for you.401(k) Plan Definition

Types of 401(k) Plans

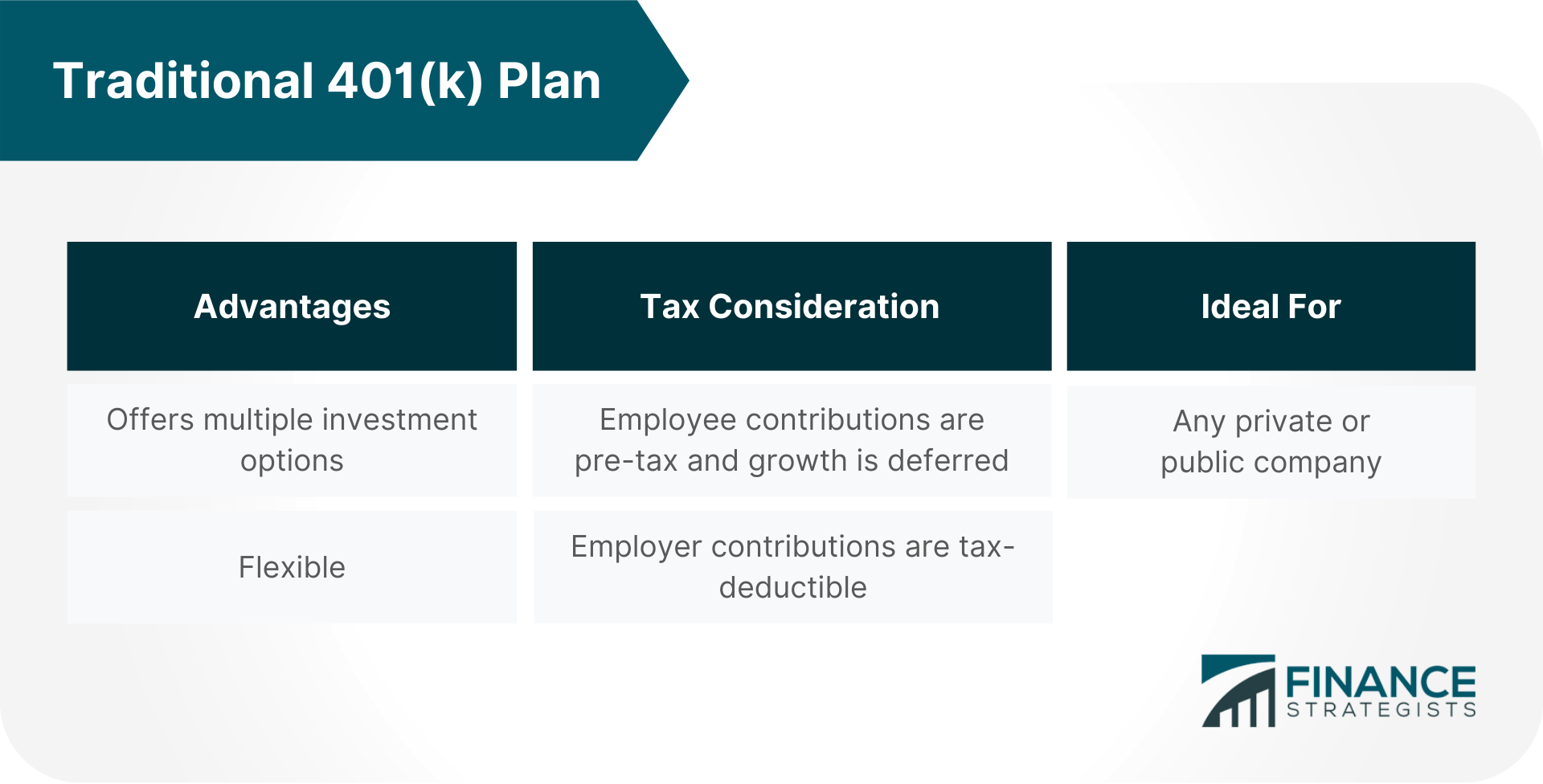

Traditional 401(k)

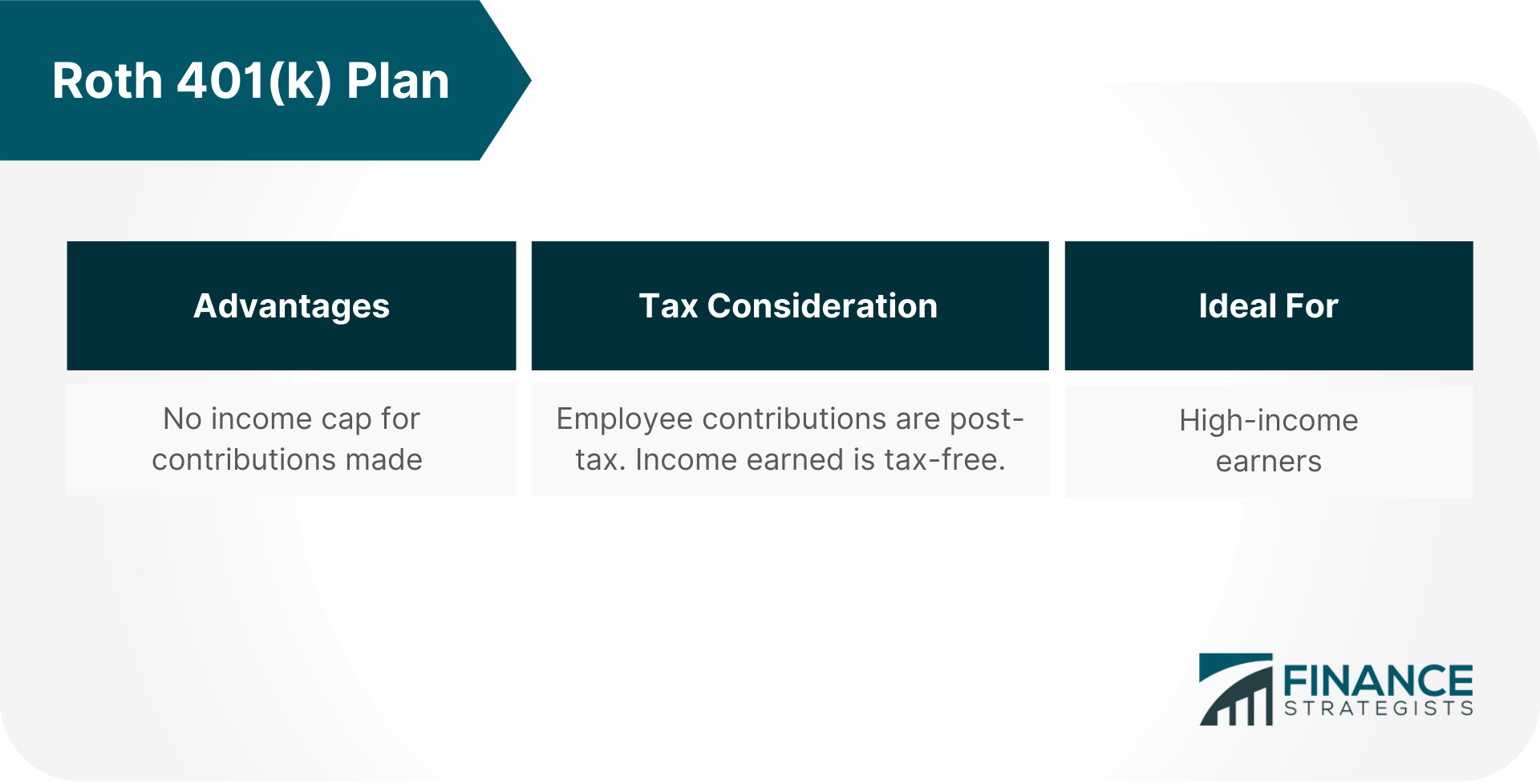

Roth 401(k)

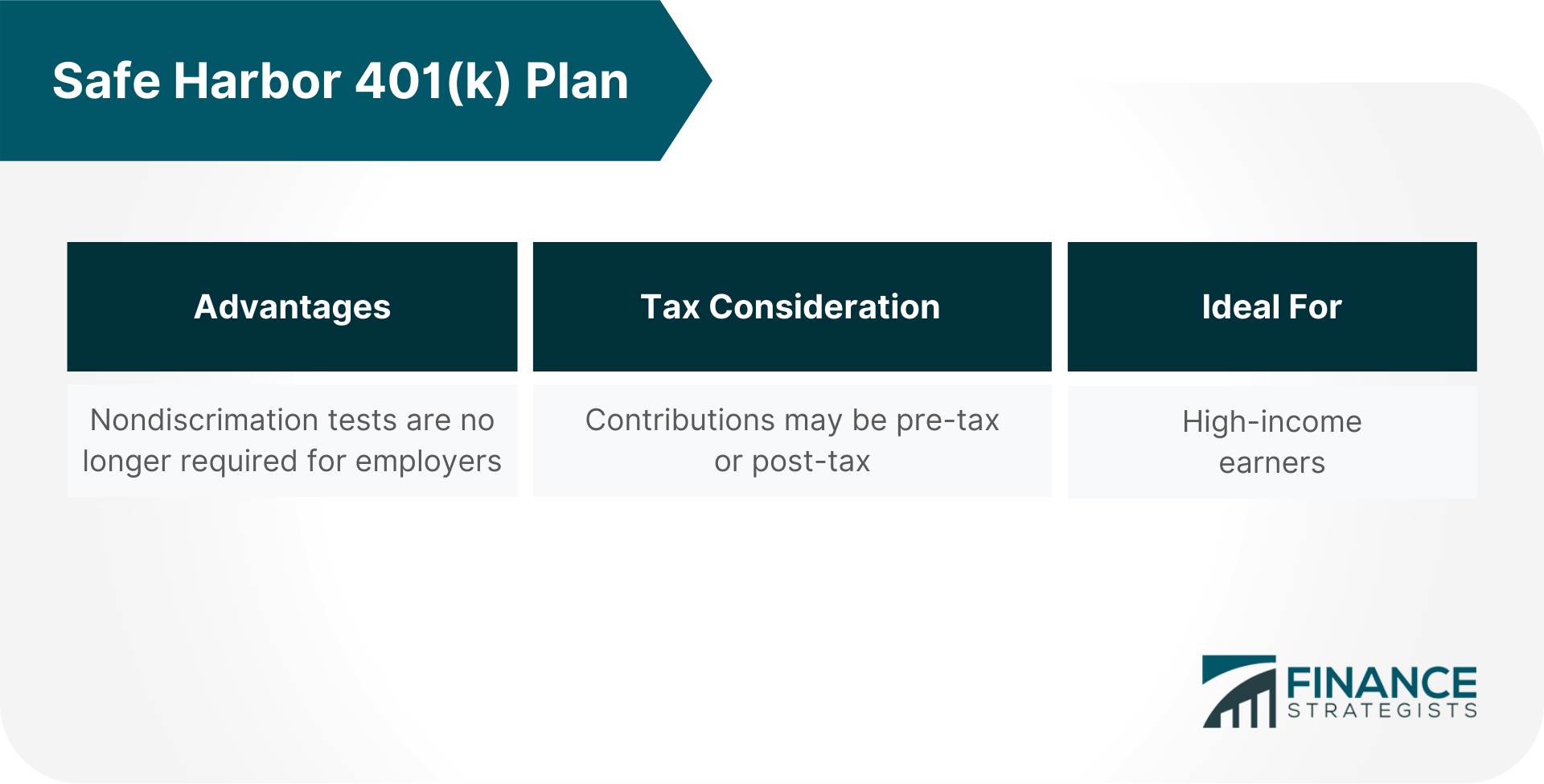

Safe Harbor 401(k)

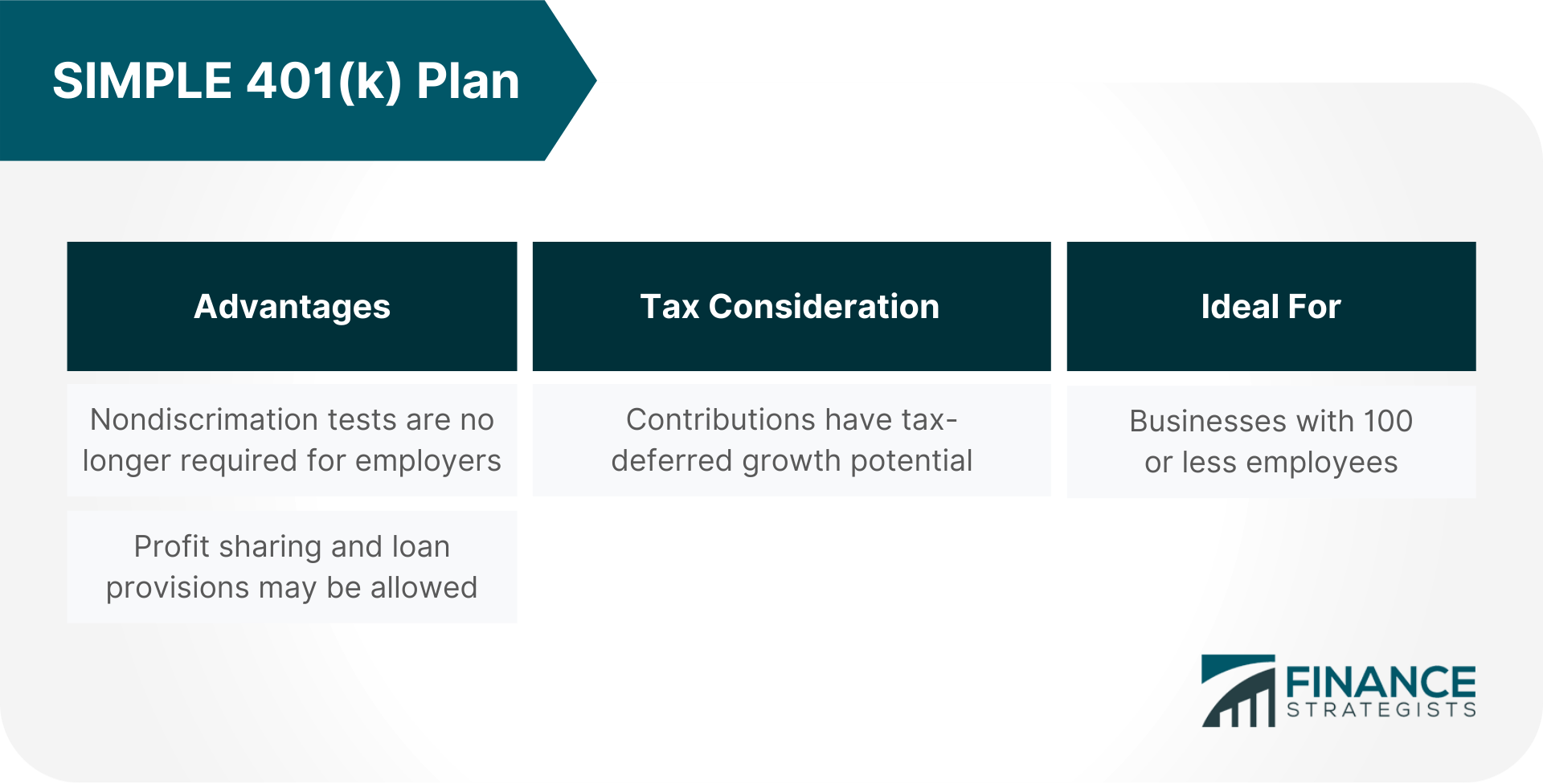

SIMPLE 401(k)

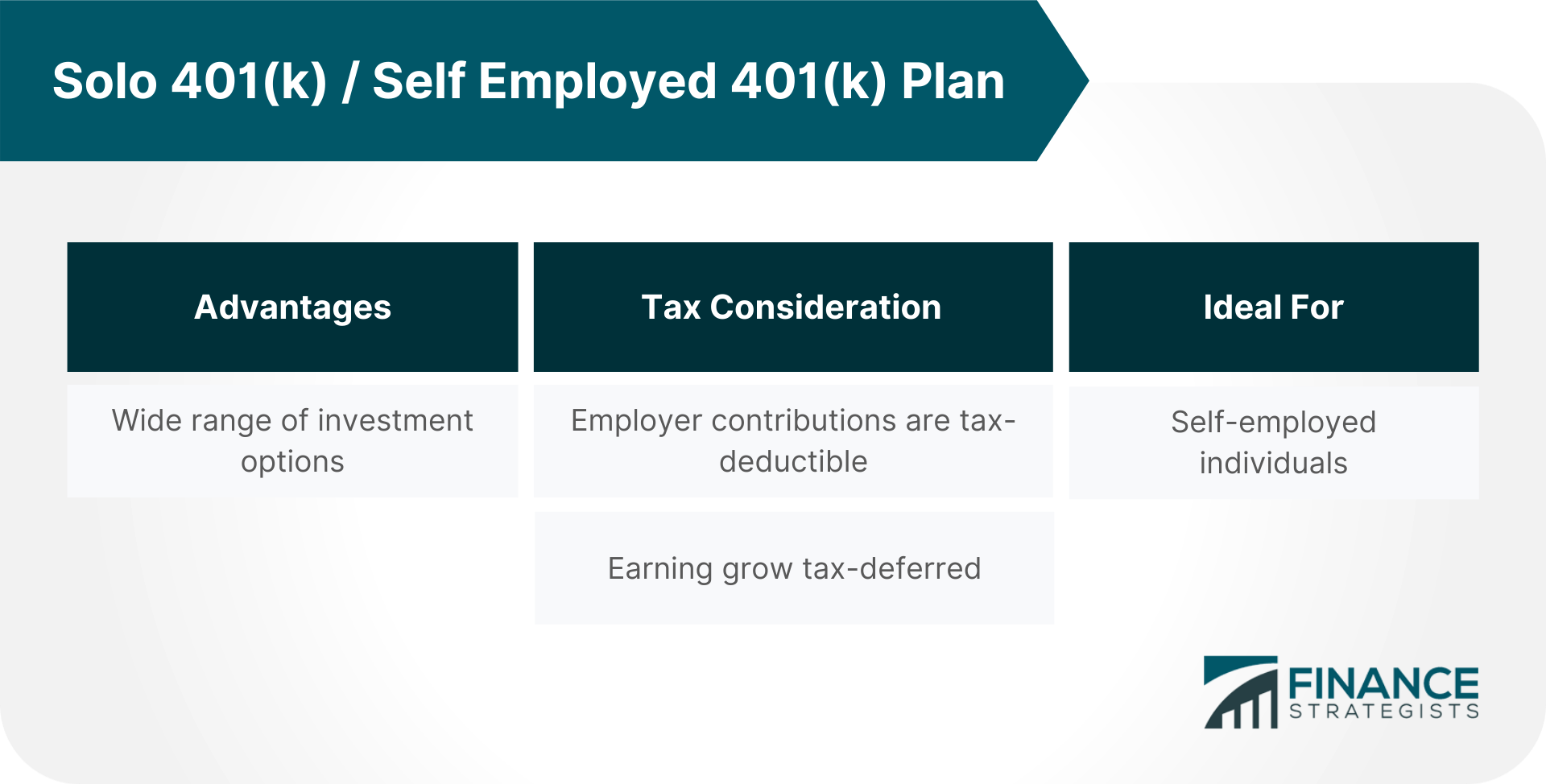

Solo 401(k)/Self Employed 401(k)

Final Thoughts

Types of 401(k) Plans FAQs

Yes. This can be done through a rollover, which is the process of transferring money from one retirement account to another.

It depends on your goals and financial situation and the availability of the plans as offered by your employer.

You have two options: roll over or cash out.

No. Depending on the plan, employees may have the option of making Roth 401k contributions from after-tax dollars.

Nondiscrimination tests are used by employers to make sure everyone is benefiting equally from the company's 401k plan. Employers must pass these tests every year to avoid penalties with employee elective deferrals and employer contributions.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.