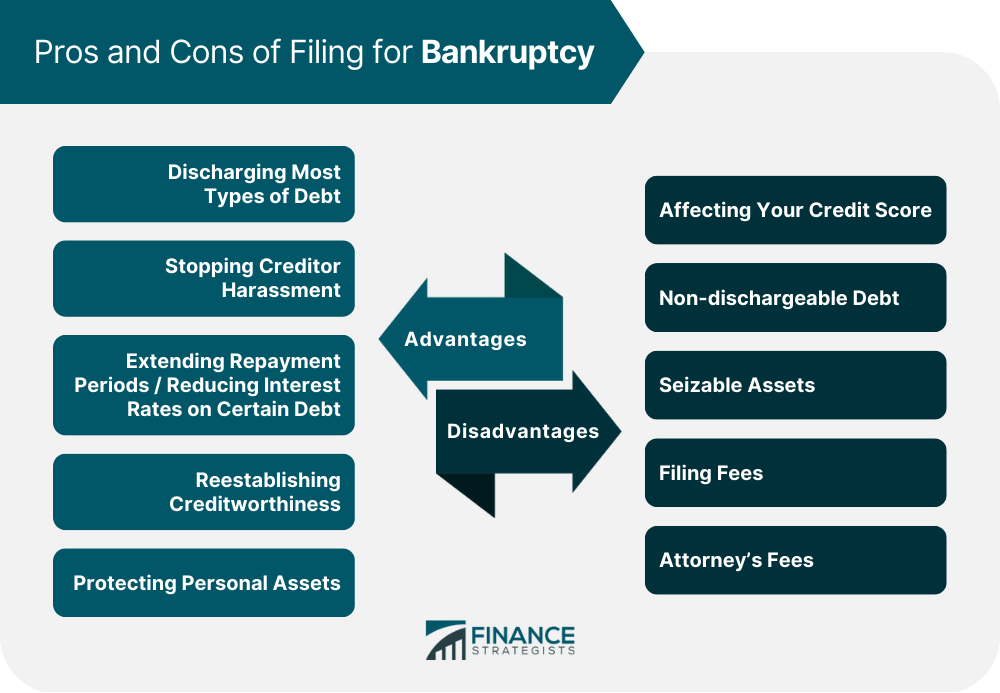

Bankruptcy is a legal process that can help individuals and businesses get relief from unmanageable debt. One of the most important factors in determining whether to file for bankruptcy is your total amount of debt. The amount of debt required to file varies depending on the type of bankruptcy you intend to pursue. Chapter 7 bankruptcy is designed to help individuals and business entities who don’t have enough income or assets to pay off their debts. While there is no minimum or maximum amount of debt necessary to qualify, debtors must first pass the means test. The means test requires debtors to compare their income and expenses to determine whether or not they are eligible for relief under Chapter 7 of the Bankruptcy Code. In some cases, debtors can have additional debts that go beyond the means test threshold and still qualify for Chapter 7 bankruptcy. In contrast with chapter 7 bankruptcies, which require liquidation of assets or property in order to pay off creditors, chapter 13 bankruptcies allow debtors to create a payment plan with creditors instead. This past June, Congress passed the Bankruptcy Threshold Adjustment and Technical Corrections Act that changed how much debt a filer may have to qualify for Chapter 13 bankruptcy. Before this law, there was a distinction between secured and unsecured debts, with different limits on each category. The passage of this act eliminated that disparity and set one total limit of $2.75 million to be eligible for filing under Chapter 13 bankruptcy — provided the amount is below said threshold. While there is no specific debt limit or required income for Chapter 11, the debtor must demonstrate that they have enough income and resources to reorganize their debts and make payments on a repayment plan. The plan must be approved by the court as well as all of the creditors involved. The debtor must also show that their debts are primarily consumer debts in order for them to be eligible for Chapter 11 relief. There are several types of bankruptcy, with the three most commonly filed being: Chapter 7 bankruptcy is often referred to as “liquidation” because it requires the debtor to sell off some of their assets in order to pay back creditors. Creditors are paid from the proceeds of any asset sales before the remaining debts can be discharged by the court. In most cases, Chapter 7 will discharge all unsecured debt but will not eliminate secured debts such as mortgages or car loans. With Chapter 13 bankruptcy, an individual can elect to restructure their finances and propose a repayment plan that lasts three to five years. Under this plan, the debtor must begin making payments within 30 days after filing for bankruptcy and make regular payments during the duration of the repayment plan. Once completed, most remaining unsecured debt is discharged. However, Chapter 13 does not usually offer complete debt elimination like Chapter 7 does. Chapter 11 bankruptcy offers businesses a chance to reorganize their financial affairs and remain operational while still trying to repay creditors when possible. Depending on their financial situation and circumstances, a business can propose a repayment plan that could last up to five years and modify existing contracts with creditors so it can remain in operation while paying off its debts over time. Filing for bankruptcy can be a difficult decision, but it can also provide a fresh financial start. Before making any decisions, it’s important to understand the pros and cons of doing so. Filing for bankruptcy has many potential benefits which include: Discharging most types of debt, including medical bills, credit card debts, and personal loans; Stopping creditor harassment; Extending repayment periods or reducing interest rates on certain types of debt (e.g., student loans); Reestablishing your creditworthiness quicker than if you were to pay off all your debts on your own; and Protecting assets such as your home or car from creditors in some cases. However, filing for bankruptcy also comes with some drawbacks, including: Affecting your credit score and making it more difficult to qualify for new loans or lines of credit; Certain types of debt may not be dischargeable (e.g., student loans); Some states allow creditors to seize certain assets regardless if you’re in bankruptcy (e.g., 401(k) accounts); Filing fees may need to be paid upfront; and Attorney's fees may need to be paid if you choose to use legal representation during the proceedings. It’s important to do research before filing for bankruptcy so you can make an informed decision that is best for your situation. The amount of debt you need to file for bankruptcy depends on a number of factors, such as the type of bankruptcy and your individual circumstances. In general, if an individual's total unsecured debts exceed what they can reasonably pay off within five years, then they may become eligible for Chapter 7 bankruptcy. Maximum income thresholds also need to be met in order to qualify for either Chapter 7 or 13 bankruptcy. Finally, applicants must receive credit counseling from an approved nonprofit organization before filing a petition with the court.Determining the Amount of Debt Required to File for Bankruptcy

Qualifying Debts for Chapter 7 Bankruptcy

Qualifying Debts for Chapter 13 Bankruptcy

Qualifying Debts for Chapter 11 Bankruptcy

Types of Bankruptcy

Chapter 7 Bankruptcy (Liquidation)

Chapter 13 Bankruptcy (Reorganization)

Chapter 11 Bankruptcy (Reorganization for Businesses)

Pros and Cons of Filing for Bankruptcy

Pros

Cons

Conclusion

How Much Debt Do You Need to File for Bankruptcy? FAQs

The amount of debt you need to file for bankruptcy depends on the type of bankruptcy you are considering filing. If you are considering filing for Chapter 13 bankruptcy, the amount of debt owed must not exceed a certain limit set by federal law.

Most unsecured debts – like credit card and medical bills – can usually be discharged in bankruptcy. Secured debts – such as mortgages and car loans – may not be eligible for discharge depending on the circumstances.

Generally speaking, certain types of student loan and tax debt cannot be discharged through bankruptcy. Other types of non-dischargeable debt include domestic support obligations (e.g., alimony payments or child support) or criminal fines, fees, and restitution.

Filing for bankruptcy can cost hundreds or even thousands of dollars in court costs, attorney's fees, and other related expenses. That said, there are programs designed to help lower-income individuals who cannot afford these costs have access to legal assistance.

Yes. Once your case is filed with the court, an automatic stay goes into effect that prevents creditors from continuing their collection activities against you – including phone calls and letters requesting payment.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.