Banks are licensed financial institutions that offer services like accepting deposits or issuing loans. They may also provide other financial services, such as investments and foreign exchange. Banks are essential to the economy because they allow businesses and individuals to store their money and make loans. The national government or individual states regulate them. In some cases, they may be covered by regulations at both levels. At the state level, the department of banking or the department of financial institutions regulates how banks work, including how much interest they charge. Banks under their jurisdiction are usually audited and inspected to see if they follow regulations. On the other hand, the Office of the Comptroller of the Currency (OCC) regulates national banks by outlining rules on bank capital levels, asset quality, and liquidity. There are different types of banks, including commercial banks, savings and loan associations, credit unions, and investment banks. Each type of bank has its own unique set of services. Using traditional banks remains unparalleled because of the security and reliability they can offer. They provide a safe place to store your money, and they offer a variety of financial services. They can help you save for goals, make payments, and invest your money. Banks are regulated by the government, which means that they must adhere to strict safety and security guidelines. In addition, they have a variety of protections in place for their customers, including The Federal Deposit Insurance Corporation (FDIC) coverage. This means that your money is safe if the bank goes bankrupt. An FDIC-insured bank account generally provides financial security, convenient access to funds, savings on check-cashing costs, and overall financial peace of mind. The majority of banks can be classified according to the following types: Retail banks are banks that provide banking services to the general public. They offer a broad range of services, including savings and checking accounts, loans, and credit cards. These establishments have physical locations where customers can conduct transactions. Commercial or corporate banks customize their services for business clients, from small companies to multinational corporations. These banks provide credit services, cash management, commercial real estate services, employer services, and trade financing, aside from standard business banking services. Investment banks deliver technical financial services to corporate clients, such as underwriting and merger and acquisition (M&A) assistance. In these transactions, they serve as financial mediators. Central banks differ from other types of bank in that the public do not transact directly with them. A central bank is an independent government-owned institution that regulates a country's monetary policy and money supply. Central banks are accountable for the stability of the currency and the whole economic system. In addition, they regulate the capital and reserve requirements of the country's banks. You may consider the following factors to make the best decision when choosing a bank: First, you must consider the type of bank account you need since some banks offer better terms for specific ones. There are three main types of bank accounts, each with unique features and benefits. Another factor to consider when choosing a bank is its associated fees and interest rates. Banks implement fees for various services, such as monthly maintenance, wire transfers, or overdraft protection. Interest rates are the percentage of interest on the deposited amount that customers earn in exchange for allowing the bank to use their funds. When searching for banks, compare the fees, and interest rates offered. Some banks may charge higher fees but also offer higher interest rates. Others may charge lower fees which may be offset by their lower interest rates. You may want to select the bank that offers the best combination of fees and interest rates for your needs. When choosing a bank, you should also consider the services offered. Most banks offer similar services, such as savings and checking accounts, loans, and credit cards. However, some banks may offer unique services, such as online banking, mobile banking, or in-person financial advice. Another factor to consider when choosing a bank is whether you want a brick-and-mortar bank or an online bank. Brick-and-mortar banks have physical locations where you can deposit money, withdraw funds, and speak to a teller or banker in person. Online banks are purely digital and offer services online or through a mobile app. Brick-and-mortar banks may provide more personal services but could charge higher fees to cover their overhead cost. Online banks may be more convenient but may not provide the same level of customer service. Consider which set-up is more appropriate for your needs when choosing between these banks. You may also consider how accessible a prospective bank’s locations are. Important factors include the proximity of ATMs and branches and the availability of online and mobile banking. If you travel frequently, you may want to choose a bank with branches in multiple states or even countries. If you have a disability, you may want to choose a bank with ATMs that are wheelchair accessible. You may also want to check if your prospective bank is FDIC-insured before opening an account. This will protect you against losing your deposits in the event of a bank failure. Any bank that is FDIC-insured is a safe and reliable choice. Here are some additional tips that can improve your overall banking experience. If you already have an existing bank account, do not assume that your bank offers the best rate. Examine the fees you are paying and see if you can minimize them. Check online for high-yield accounts with a lower minimum balance to avoid maintenance costs. When selecting between accounts, read the finer details about their rates. Some promotional or introductory rates may be attractive but last only a few months. You may also verify if a certain minimum is required to receive the promised interest. When opening a new bank account, do not feel obligated to bank with the same institution where you have a checking or savings account. Review different options and compare services, rates, and fees before deciding. Banks are regulated financial entities that provide services such as accepting deposits and extending loans. They generally provide a secure and convenient location to store your funds while offering the opportunity to earn some interest. Banks can be classified as retail, commercial, investment, and central. Since each type has its own advantages and disadvantages, it is best to determine the most appropriate one for your needs. Factors like available account types, fees, interest rates, and accessibility should be considered when choosing a bank. Even after selecting a bank, you may review your options periodically to ensure you get the most benefits and maximize your banking experience.What Is a Bank?

Importance of Using a Bank

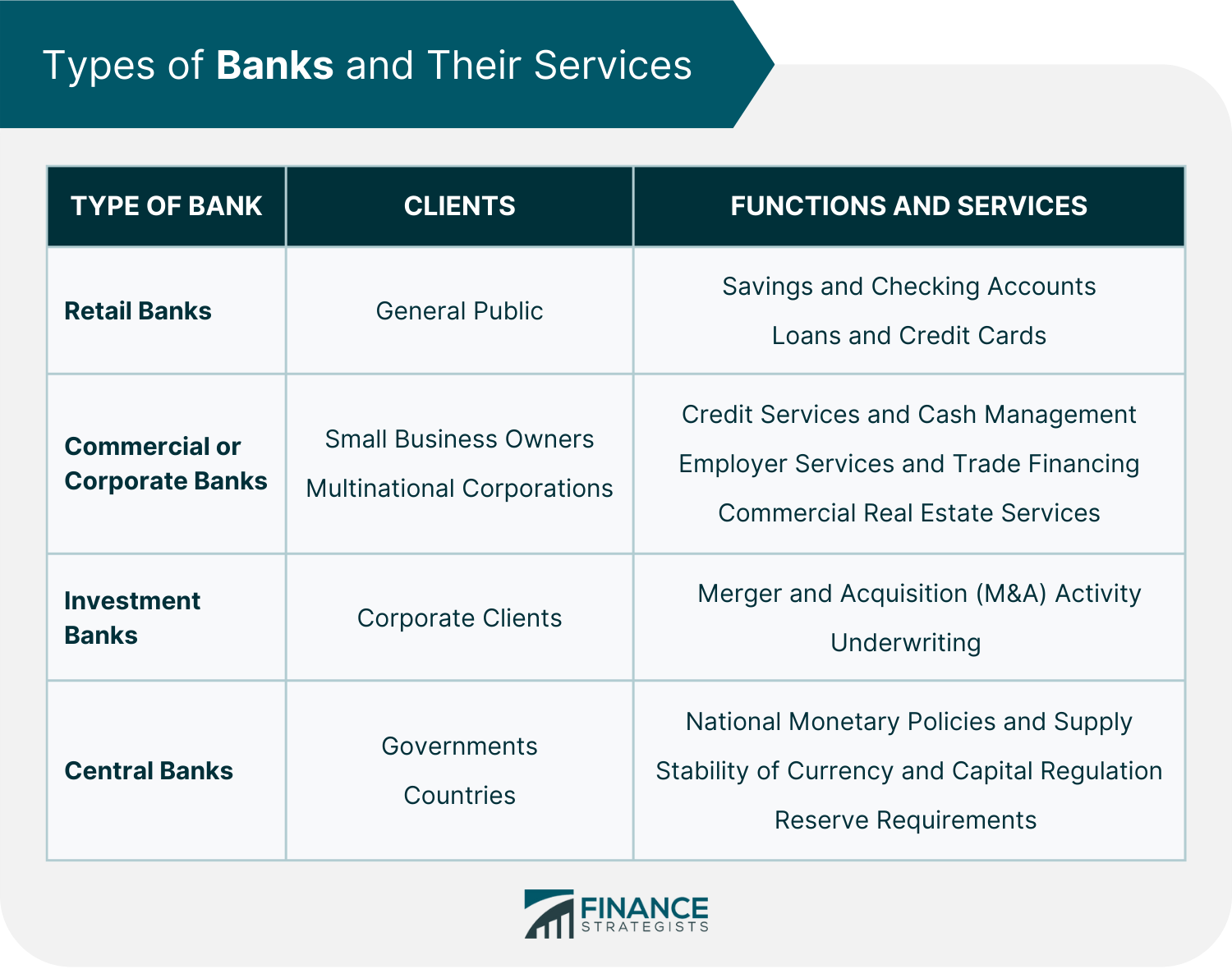

Types of Banks

Retail Banks

Commercial or Corporate Banks

Investment Banks

Central Banks

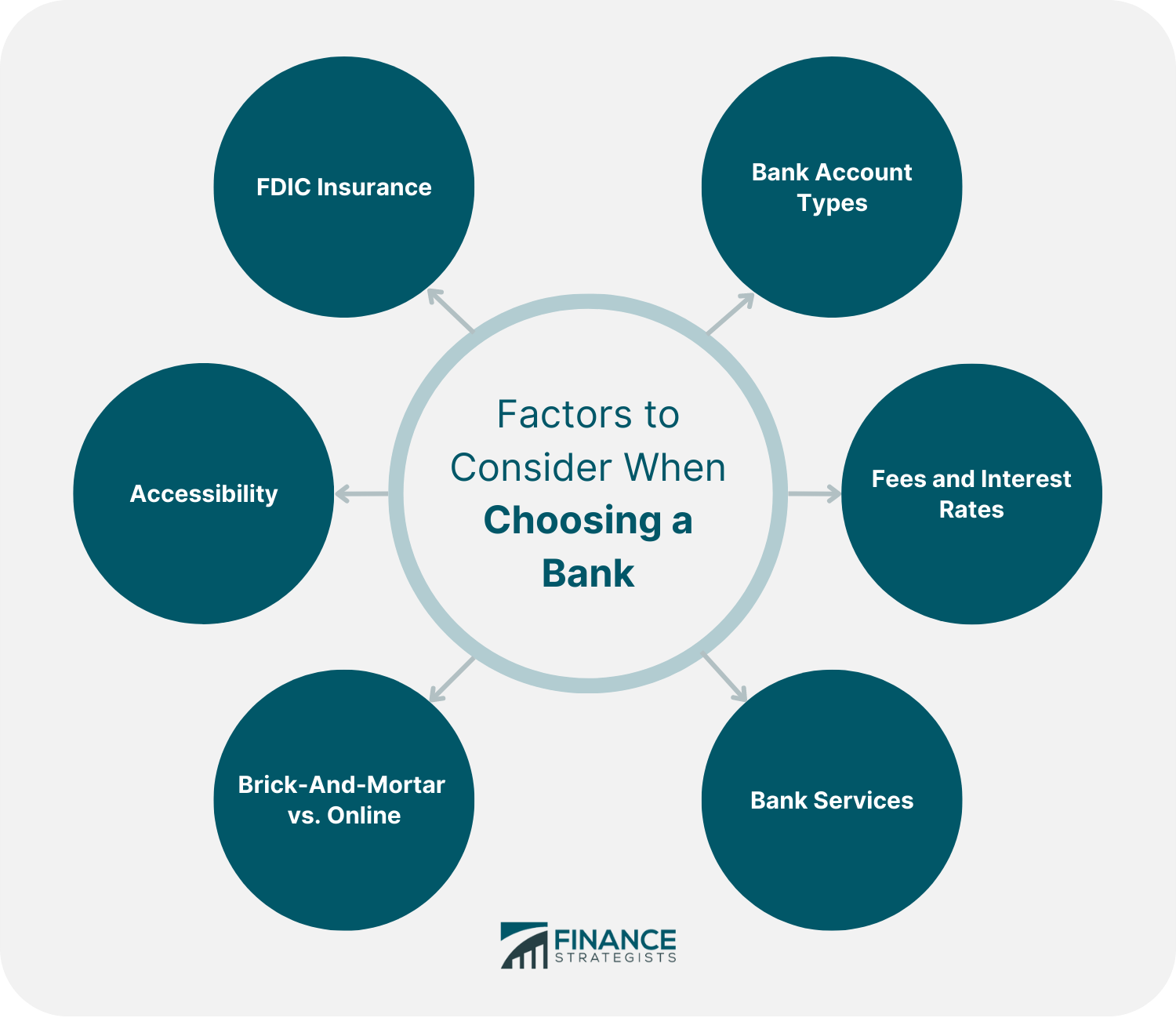

Factors to Consider When Choosing a Bank

Bank Account Types

These accounts are typically used for long-term financial goals, such as preparing an emergency fund or saving for a trip.Fees and Interest Rates

Bank Services

Brick-and-Mortar vs Online

Accessibility

FDIC Insurance

Banking Tips

Appraise Your Bank

Be Careful of High Interest Rates

Consider Multiple Banks

The Bottom Line

Banking FAQs

A bank is a regulated financial institution that accepts deposits and extends loans. Depending on the type of bank, they may also offer other services, such as selling securities.

When picking a bank, you should consider the types of accounts and services they offer. You may also review their accessibility, safety, fees, and interest rates.

The different types of banks include retail, commercial, investment, and central banks.

The fees may vary depending on the account type you hold with the bank. However, common banking fees include overdraft fees, ATM fees, monthly service fees, and maintaining balance fees.

Yes, some online banks are FDIC-insured, just like brick-and-mortar banks. This means that your deposits are protected up to $250,000 in case of a bank failure. Be sure to check if your prospective online bank is one of those who fall in this category.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.