A broker-dealer is a person or financial entity trading securities for their own account or on behalf of their clients. The entity could be a corporation, limited partnership, limited liability company, or general partnership. Since most stock brokerages function as agents and principals, the term broker-dealer is used to define them in terms of U.S. securities laws. When executing orders on behalf of its clients, a brokerage works as a broker or agent. When trading for its own account, a brokerage serves as a dealer or principal. In the financial sector, broker-dealers perform several crucial tasks. These include giving clients financial advice, creating liquidity through market-making activities, facilitating trade, disseminating investment research, and helping businesses raise capital. They are subject to oversight from regulatory agencies such as the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA). Broker-dealers vary in business size, from small and independent to large subsidiaries of giant commercial and investment banks. The two main types of broker-dealers are wirehouse and independent broker-dealers. A wirehouse is a term used to describe a full-service broker-dealer, ranging from small brokerages to leading global institutions. They often have their own line of products they offer their clients and profit from. Wirehouses like Morgan Stanley and Wells Fargo, discount brokerages like Charles Schwab and TD Ameritrade, and independent companies like LPL Financial and Raymond James are a few of the most well-known broker-dealers. A wirehouse broker is an employed representative of wirehouses whose activities are governed by their employer. Independent broker-dealers are small businesses that offer a more comprehensive range of investment options from outside sources. These include stocks, bonds, hedge funds, tax credits, non-qualified plans, and initial public offerings (IPOs). Independent broker-dealers also offer services such as financial planning and portfolio management. Compared to larger broker-dealers, these firms are often more lightly regulated due to their size. They have total control of their business and manage every aspect of the business operations, from setting up services and goals for growth trajectory to office location and work culture. Broker-dealers are intermediary when buying and selling securities and distributing other investment products. In this dual capacity, they can render their services efficiently and effectively. Brokers facilitate client transactions by sourcing and obtaining stocks from various sources, including their own supply, other broker-dealers, and outside vendors. Brokers can offer consumers looking for investments in multiple marketplaces the best service possible by being able to obtain securities on demand. They provide more than just investment advice but can also help with financial planning, research, and margin lending. Additionally, some smaller brokers might assume the fiduciary position and provide more customized advice. When making investment selections, the broker must consider the client's best interests. When broker-dealers are the primary players in an exchange, they act as dealers. As a result, they buy or sell stocks from their accounts while working on behalf of their brokerage company. Dealers purchase and sell shares on the market using their own funds and guarantee that transactions are carried out effectively, quickly, and affordably. Dealers must also correctly monitor their own trades to ensure compliance with all applicable laws and regulations. Although they might recommend products for which they will receive a commission, investors must still approve such deals. Broker-dealer fees refer to the charges that a broker-dealer, or financial intermediary, levies on its clients for facilitating securities transactions and providing investment advice. Brokerage fees are commissions for carrying out trades, negotiations, and consultations. The charges can be fixed per transaction, a percentage of total sales, or a combination of the two. Full-service brokerages offer an array of services, including tax consultation, portfolio assessment and creation, research advice, retirement planning assistance, and more. They also provide vital estate planning tools to help clients reach their financial goals faster. Working with a full-service broker typically costs 1% to 2% of the total sales or investment. With an online brokerage, investors have the advantage of fast and convenient trading. While customer service may be limited, stocks can be traded without incurring commission fees. These flat rates typically have a maximum of $30 per transaction. Unlike full-service brokers, discount brokerages have more limited product choices and no investment advice. As a form of compensation for fewer options, they provide significantly lower costs than the standard fee charged by most full-service brokers. Their transaction charges are typically flat, ranging from under $5 to above $30 per trade. Additionally, account upkeep fees usually stay close to 0.5% yearly based on how many assets their brokerage currently holds. Broker-dealers generate revenue the same way as any other business. They purchase securities like stocks and bonds, then resell them to different investors at a higher price than what they paid. The profit from these transactions is called the dealer spread. Be guided with the following steps to undertake in becoming a broker-dealer. These credentials will allow the individual or company to deal with financial transactions. In general, these differ depending on the sort of products involved. In addition, the broker-dealer must pass certain examinations, such as the Securities Industry Essentials (SIE) exam, before selling any security directly to the client or customer. Provide an application form, often known as the Form BD or the Uniform Application for Broker-Dealer Registration, for each state where the broker intends to market its products. This form is submitted to the SEC, self-regulatory organizations (SROs), and FINRA's Central Registration Depository (CRD) to identify the broker's personal information, contact information, and any conflicts of interest. The next stage is to join FINRA or any other self-regulatory organization. You must become a Securities Investor Protection Corporation (SIPC) member. SIPC assists investors in receiving compensation if the investment company goes bankrupt or becomes solvent. Follow any pending formalities in the state where the broker intends to practice and complete any required certificates. The SEC provides a comprehensive set of criteria for all formalities, which may differ from state to state, and the broker-dealer must adhere to them. Broker-dealers and RIAs are the two primary categories of financial managers. The following are the fundamental distinctions between the two investment experts: Independent broker-dealers perform the same duties as full-service brokerage firms without being subject to the restrictions and requirements of a major Wall Street corporation. However, RIAs are independent financial advisors acting in a fiduciary capacity that works with broker-dealers to sell various goods and services. Broker-dealers must register with SEC and join FINRA and SIPC. Further, they must comply with state mandates and meet eligibility requirements. RIAs are required to register with the SEC or State Securities Regulator depending on the value of assets under management. Brokerage fees are the primary source of income for broker-dealers. Some charges are a set amount per transaction, a portion of overall revenues, or a combination of both. RIAs charge clients a percentage of their assets under their management, while others bill a flat or hourly rate for the advice they provide. Thus, broker-dealers are more flexible, and their investments are bound by the lower suitability standard. Working with RIAs also offer many benefits especially because they are required to operate according to fiduciary standard. A broker-dealer is a financial intermediary, either an individual or a financial entity, acting as a broker and a dealer in trading securities. The two main types of broker-dealers are wirehouses and independent broker-dealers. Broker-dealers facilitate client transactions by sourcing and acquiring stocks and charging brokerage fees and commissions for trades, negotiations, and consultations. To become a broker-dealer, an individual or financial entity must register with SEC and join any SRO and SIPC. Further, they must comply with state mandates and meet eligibility requirements. Broker-dealers differ from Registered Investment Advisors regarding functions, qualifications and requirements, and fees. A financial advisor can provide expert advice and help clients understand how their investments and markets operate.What Is a Broker-Dealer?

Types of Broker-Dealers

Wirehouse

Independent Broker-Dealer

Roles of a Broker-Dealer

As a Broker

As a Dealer

Broker-Dealer Fees

Brokerage Fees

Full-Service Brokerage Fee

Online Brokerage Fees

Discount Brokerage Fees

Bid-Ask Spread

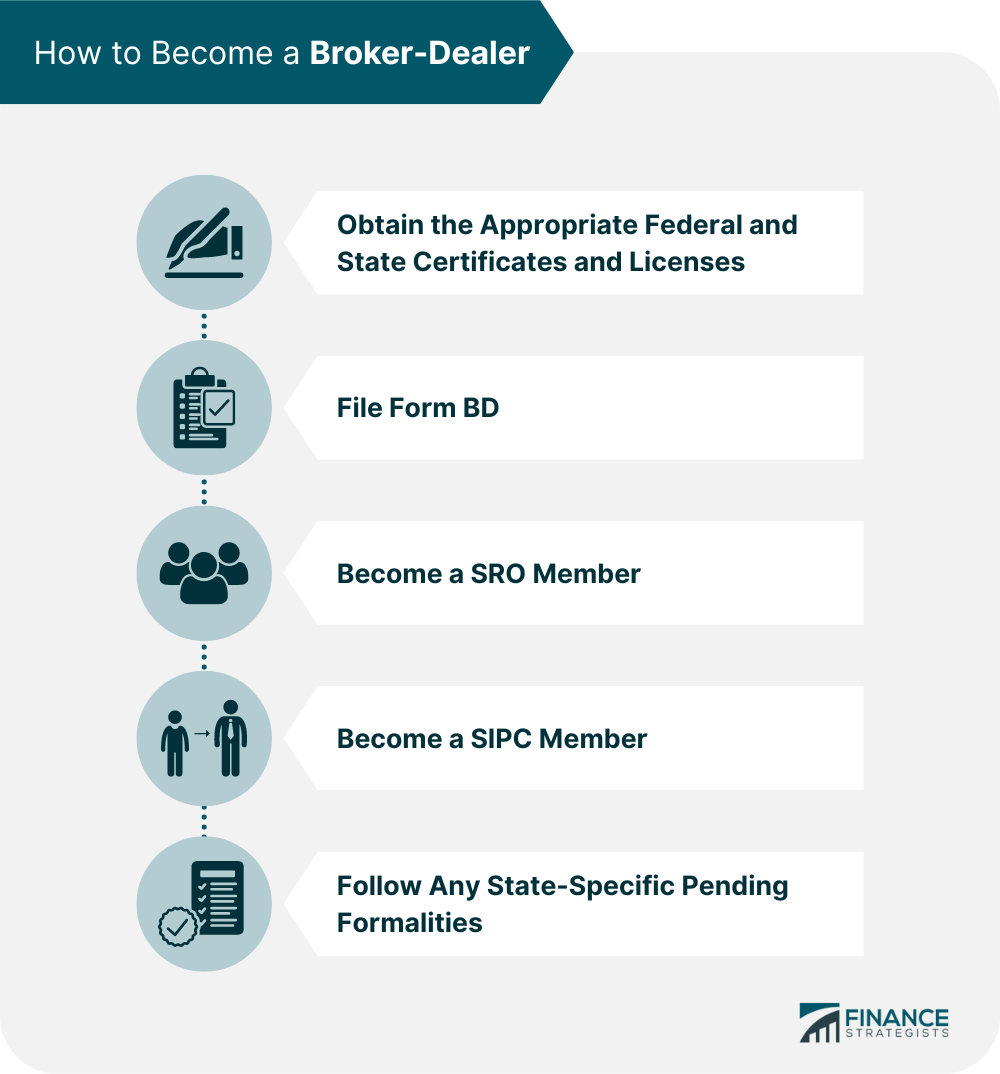

How to Become a Broker-Dealer

Obtain the Appropriate Federal and State Certificates and Licenses

File Form BD

Become a SRO Member

Become a SIPC Member

Follow Any State-Specific Pending Formalities

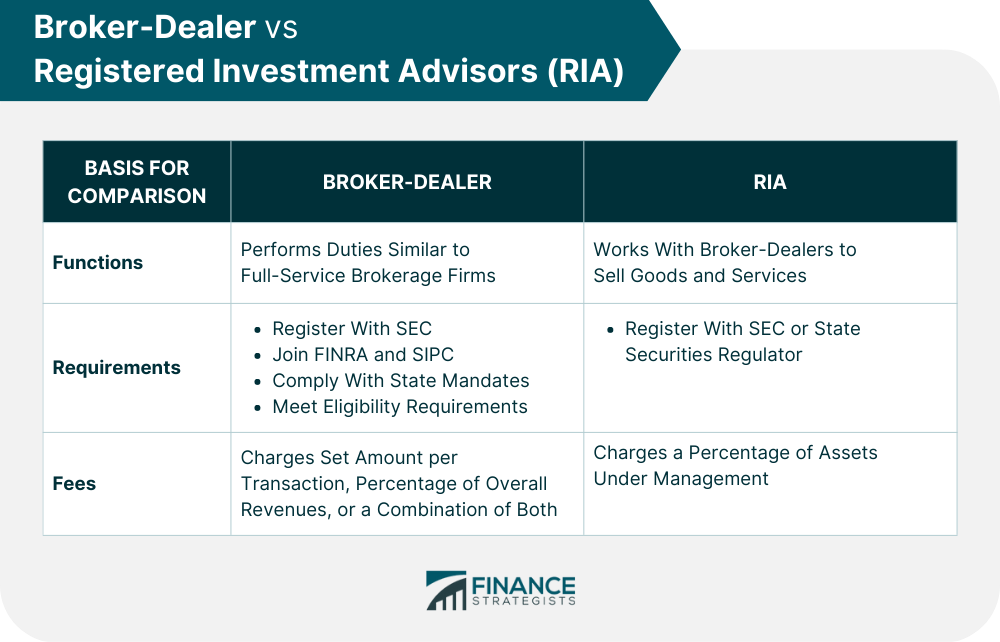

Broker-Dealers vs Registered Investment Advisors (RIAs)

Functions

Qualifications and Requirements

Fees

Final Thoughts

Broker-Dealer FAQs

A broker-dealer can be firms, banks, or individuals who generally purchase securities and then eventually sell them at a higher price to another investor. They also participate in the sales of securities.

Some of the most famous broker-dealers are wirehouses like Morgan Stanley and Wells Fargo, discount brokerages like Charles Schwab and TD Ameritrade, and independent firms like LPL Financial and Raymond James.

Brokerage fees are the main source of income for broker-dealers. They mainly sell the securities at a price more significant than the purchase price. The difference between the two prices is called the dealer's spread, which is the broker-dealer's profit on every transaction.

A broker executes on behalf of clients; he can be a full-service or discount broker who is only engaged in buying and selling securities. A dealer buys and sells securities on its own, but some dealers identified as primary dealers facilitate trades on behalf of the U.S. Federal Reserve in implementing monetary policy. On the other hand, broker-dealers do both roles.

Securing a broker-dealer is highly recommended for those unfamiliar with the trading industry. He will manage financial transactions between buyers and sellers and provide services such as stock splits and facilitate stock trading.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.