Death taxes are a type of tax imposed on an individual's estate upon their death by the federal government and some state governments. It can be further subdivided into estate taxes and inheritance taxes. With estate taxes, dues are paid by the estate itself before any distribution is made to the beneficiaries. In contrast, with inheritance taxes, beneficiaries pay dues after they have received distributions from the estate. Both estate and inheritance taxes are usually calculated based on how much the decedent’s estate was worth upon death. After someone dies, death taxes in the form of inheritance tax and estate tax are collected. First, the federal government collects estate taxes. On top of that, twelve states and one district impose an additional estate tax. These are the states of Connecticut, Hawaii, Illinois, Maine, Maryland, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont, and Washington. Also included in this list is the District of Columbia. The federal government does not collect inheritance tax. However, the states of Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania do. Aside from paying estate tax to the federal government, residents in these states also have to pay inheritance tax. All of these states who collect inheritance taxes have exemptions for surviving spouses. On the other hand, Nebraska and Pennsylvania still collect taxes from estates left to surviving offspring or grandchildren. Due to the Tax Cuts and Jobs Act of 2017 only a few people must pay the federal estate tax. For 2024, only estates valued above $13.61 million are subject to this tax. Aside from this threshold, individuals also need to take note of the annual and lifetime gift tax limits. To circumvent estate taxes, individuals can give their assets as gifts during their lifetime. However, if the value of these gifts goes over the annual limit, they are subjected to the gift tax and deducted from a person's lifetime limit. For 2024, individuals may give up to $18,000 annually per recipient tax-free. Any gifts above this amount count towards a person's lifetime gift tax limit, which is the same as the threshold for death taxes. The unified tax credit consolidates the two distinct exemptions for gift and estate taxes. The unified tax credit combines the amount given in gifts during an individual's lifetime with the taxable part of a decedent's estate. Federal estate taxes are applied if the amount exceeds the death tax threshold. Below is the unified rate schedule, which shows the taxable amount, the applicable tax rate, and what the estate pays per bracket. To illustrate, let us take the case of an individual who leaves an estate valued at $14.05 million. In his lifetime, this individual has never given anything above the annual gift tax limit. Thus, the total lifetime exemption of $13.61 million can be deducted from the estate ($14.05 million – $13.61 million). This will result in a taxable amount of $131,440. According to the Unified Rate Schedule, the taxable amount will be charged a rate of 30% and the base tax of $23,800. The resulting death tax duty (30% x $131,440) + $23,800 would amount to $63,232. The following are some advantages of death taxes: Federal estate taxes only apply when the value of an estate exceeds a certain threshold. This high threshold means that only a small number of estates are subject to the tax. The federal estate tax is predicted to generate over $200 billion in the next decade. This revenue can finance essential government expenses, such as infrastructure projects or social programs. Death taxes also have some disadvantages. Here are some of the following: Due to the estate tax, individuals may be required to pay taxes twice. First, income taxes are collected when money is earned, or an asset is acquired. Then, estate and inheritance taxes may need to be paid after death. Numerous affluent Americans escape paying estate taxes, even if they exceed the threshold for total assets. This can be done by reducing the amount of taxable estate through giving to charities, gifting to spouses, and taking advantage of the annual gift tax exemption. Death taxes can be avoided through proper estate planning. Here are some steps that estate owners can take: An irrevocable trust is a type of trust that cannot be changed or modified after it has been created. Assets placed in an irrevocable trust are no longer considered taxable estate. This alternative can help reduce the amount of death taxes that are owed. Another method of avoiding estate taxes is to make charitable donations. Donations to charity are exempt from the estate tax. They can be subtracted from the estate's worth, helping to lower the amount of taxes due. Giving assets to relatives and friends is another method of avoiding estate taxes. As long as the gifts do not exceed the yearly and lifetime gift tax exemption, estate taxes will not apply. Death taxes are a type of tax imposed on an individual's estate upon their death. It can be further subdivided into estate taxes and inheritance taxes. The federal government collects taxes on all estates. Meanwhile, some states collect additional estate or inheritance taxes. With estate taxes, dues are paid by the estate itself before any distribution is made to the beneficiaries. In contrast, with inheritance taxes, beneficiaries pay dues after they have received distributions from the estate. For 2024, only estates worth more than $13.61 million are subjected to death taxes. Death taxes have certain advantages, like ensuring that the wealthy pay their fair share and providing revenue for the government. However, there are also disadvantages to death taxes, such as the possibility of double taxation and the existing loopholes that help individuals circumvent estate taxes. These strategies include giving assets away before death and making charitable donations. Estate planning is essential for anyone with a large estate. By taking the time to plan ahead, it is possible to avoid or reduce the amount of taxes that are owed.What Are Death Taxes?

How Do Death Taxes Work?

Death Tax Limit 2024

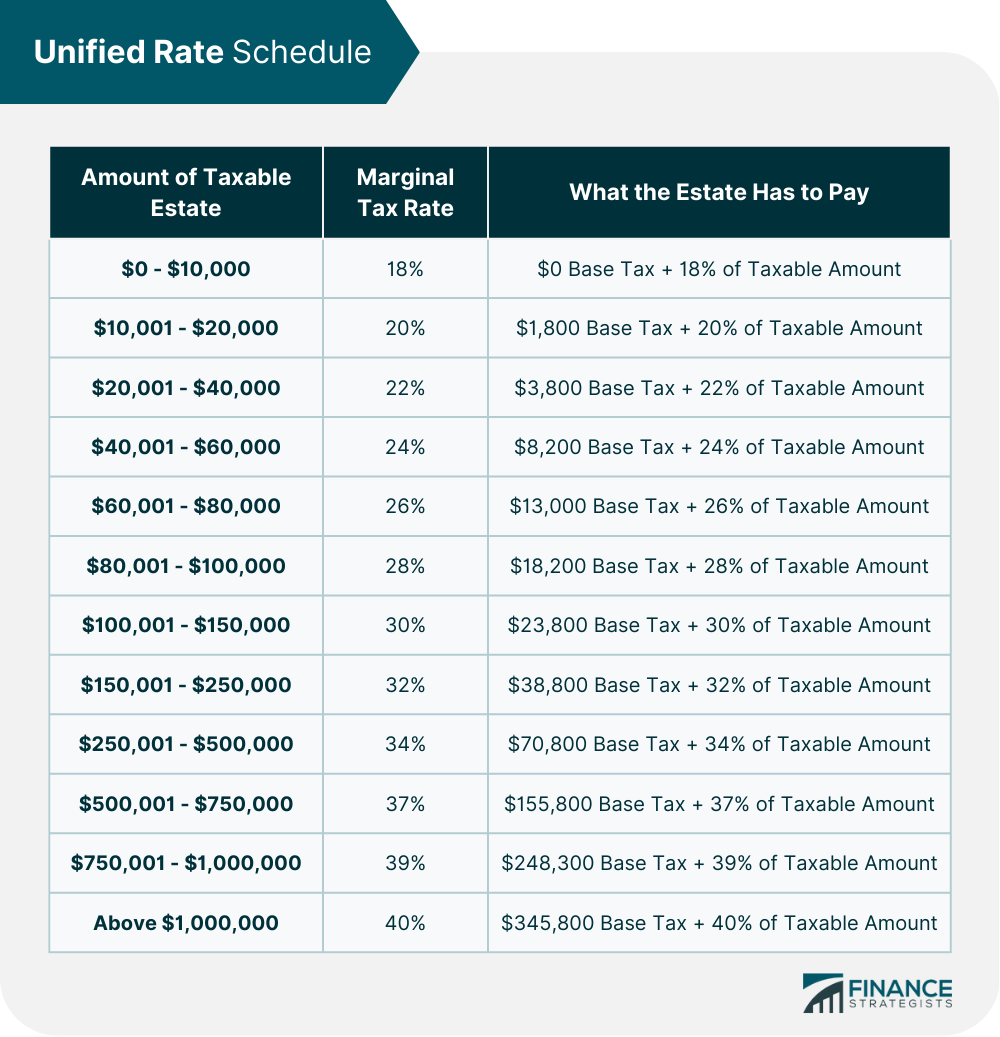

Unified Tax Credit

Death Tax Calculation Example

Advantages of Death Taxes

High Threshold

High Tax Revenue

Disadvantages of Death Taxes

Double Taxation

Loopholes

Avoiding Death Taxes

Creating an Irrevocable Trust

Charitable Donations

Giving Assets to Family and Friends

Final Thoughts

Death Taxes FAQs

The federal government collects estate taxes. Meanwhile, some states collect additional estate or inheritance taxes. With estate taxes, dues are paid by the estate itself before any distribution is made to the beneficiaries. In contrast, with inheritance taxes, beneficiaries pay dues after they have received distributions from the estate.

The states of Connecticut, Hawaii, Illinois, Maine, Maryland, Massachusetts, Minnesota, New York, Oregon, Rhode Island, Vermont, and Washington collect additional estate taxes. Also included in this list is the District of Columbia. Meanwhile, the states of Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania collect inheritance taxes.

For the year 2024, the death tax threshold is $13.61 million. Estates worth more than this amount will not be exempted from death taxes.

There are a few ways to avoid death taxes, including giving assets away before death and making charitable donations. Death taxes can also be avoided by taking advantage of the annual and lifetime gift tax exemptions.

With estate taxes, dues are paid by the estate itself before any distribution is made to the beneficiaries. In contrast, with inheritance taxes, beneficiaries pay dues after they have received distributions from the estate.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.