Debt Service Coverage Ratio (DSCR) is a ratio to measure a company's ability to service its short- and long-term debt. It is a measure of how many times a company's operating income can cover its debt obligations. The ratio is one of the factors used by financial institutions to make credit-related decisions for an entity, and analysts use DSCR to make investment-related decisions. The formula to calculate DSCR is EBITDA divided by total debt (including total interest to be paid and the principal loaned), where EBITDA of a company is the Earnings before Interest, Depreciation, Taxes and Amortization. Instead of EBITDA, some investors instead use the formula: For example, if a company has an operating income of $50,000 and total debt of $25,000 ($10,000 in short-term debt and $15,000 in long-term debt), then it has a DSCR of 2. A DSCR of 1 or above means that the company has surplus operating income that can be used to service its debts. Conversely, a ratio below 1 is not a good sign because it means that the company is unable to service its current debt commitments. For example, if a company has a DSCR of 0.5, then it is able to cover only 50% of its total debt commitments. Companies often employ different strategies to increase their DSCR score. For example, they might reduce their amount of debt requested, or may reduce their expenses in order to increase their operating income and therefore their DSCR. Financial institutions use DSCR scores to make credit lending decisions. Entities or individuals with good DSCR scores are generally eligible for loans and receive favorable terms compared to those with bad DSCR scores. Conditions in the broader economy, such as interest rates, can affect a lender's willingness to extend credit. For example, lenders relaxed their minimum DSCR score requirements in the years leading up to the financial crisis of 2008. As a result, borrowers with low debt ratio scores had easier access to funds. It is important to note that Debt Service Coverage Ratios provide less information when viewed in isolation. The debt service ratio of a company should always be measured relative to that of its peers in an industry.DSCR Defined

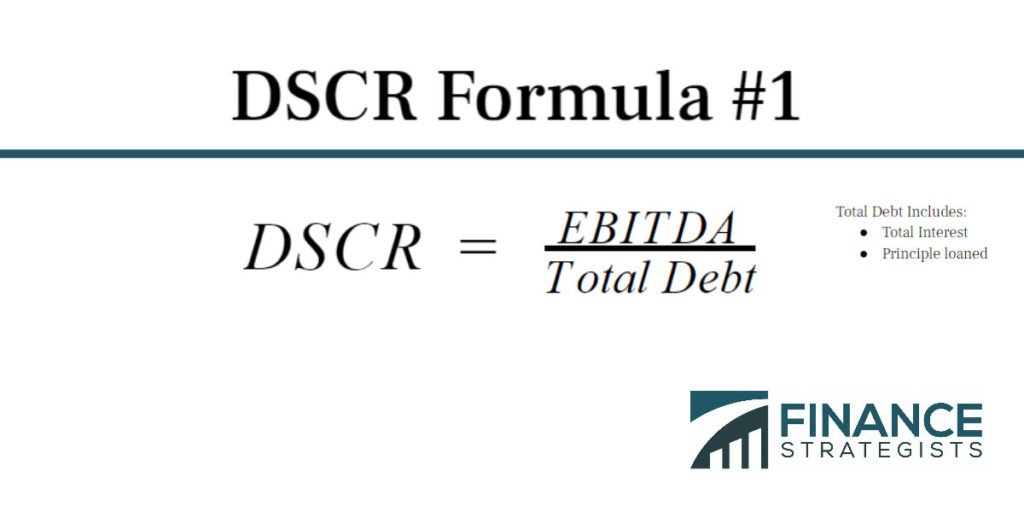

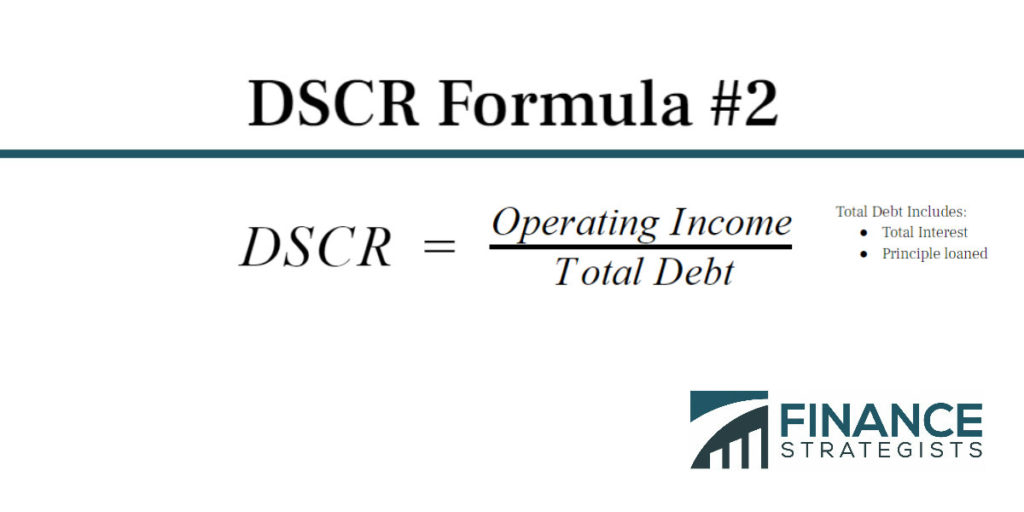

DSCR Can Be Calculated Two Ways

Formula Meaning

DSCR Company Perspective

DSCR Importance

Benefits of Having a Good DSCR Score

Debt Service Coverage Ratio (DSCR) FAQs

Debt Service Coverage Ratio (DSCR) is a ratio to measure a company’s ability to service its short and long-term debt.

The ratio is one of the factors used by financial institutions to make credit-related decisions for an entity. Analysts use DSCR to make investment-related decisions.

The formula to calculate DSCR is EBITDA divided by total debt (including total interest to be paid and the principal loaned), where EBITDA of a company is the Earnings before Interest, Depreciation, Taxes and Amortization.

A DSCR of 1 or above means that the company has surplus operating income that can be used to service its debts. A ratio below 1 means that the company is unable to service its current debt commitments.

Entities or individuals with good DSCR scores are generally eligible for loans and receive favorable terms compared to those with bad DSCR scores.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.