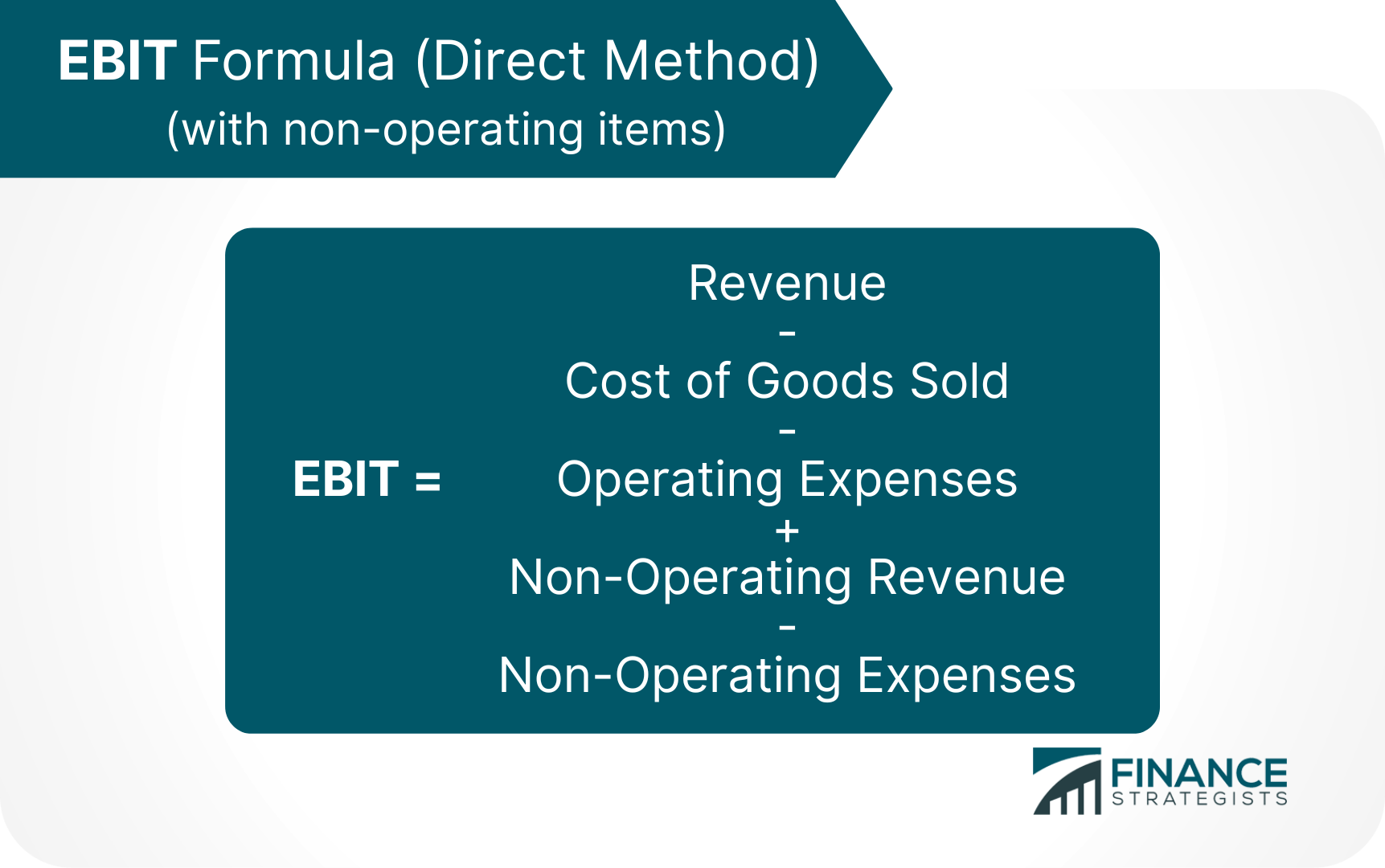

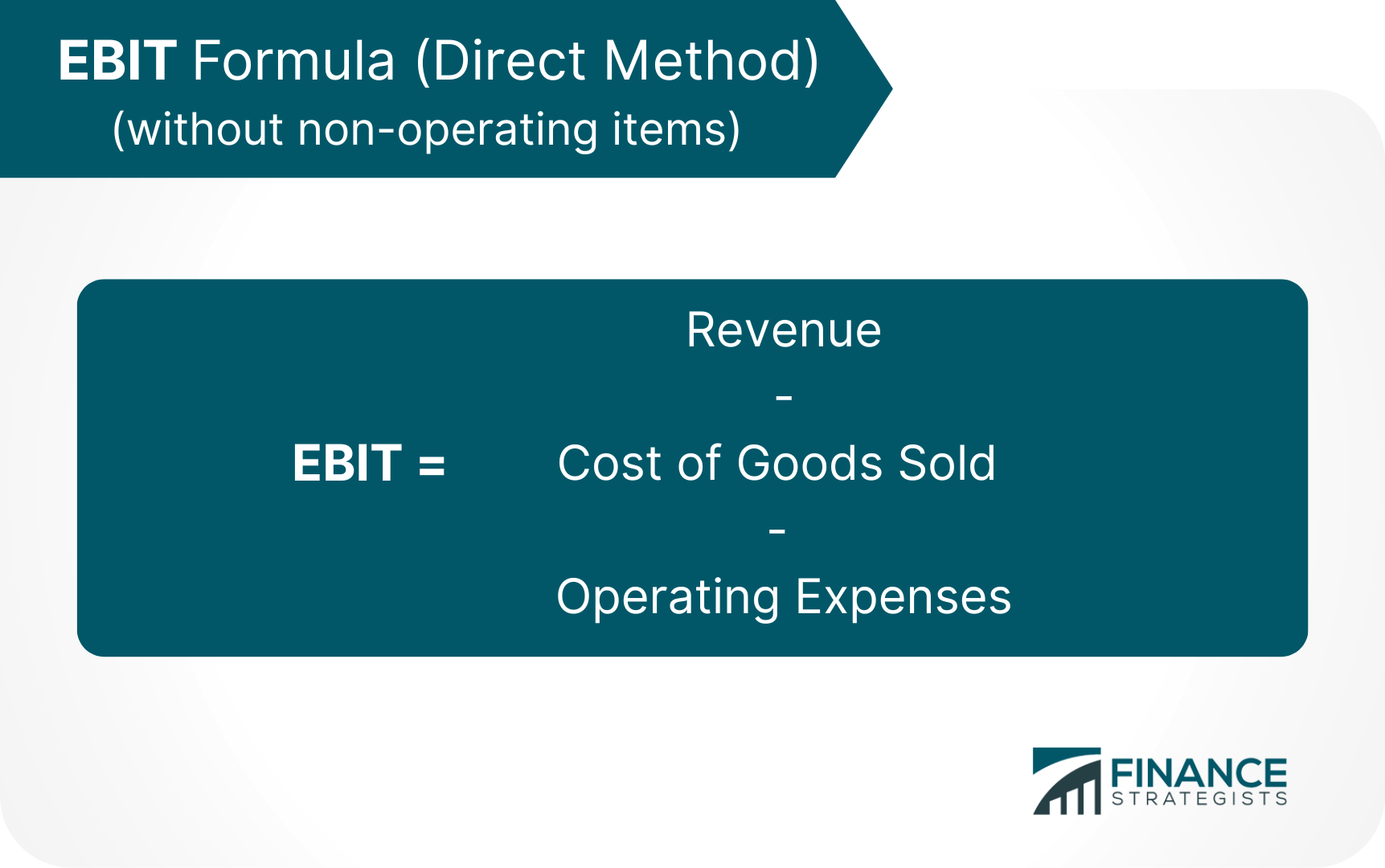

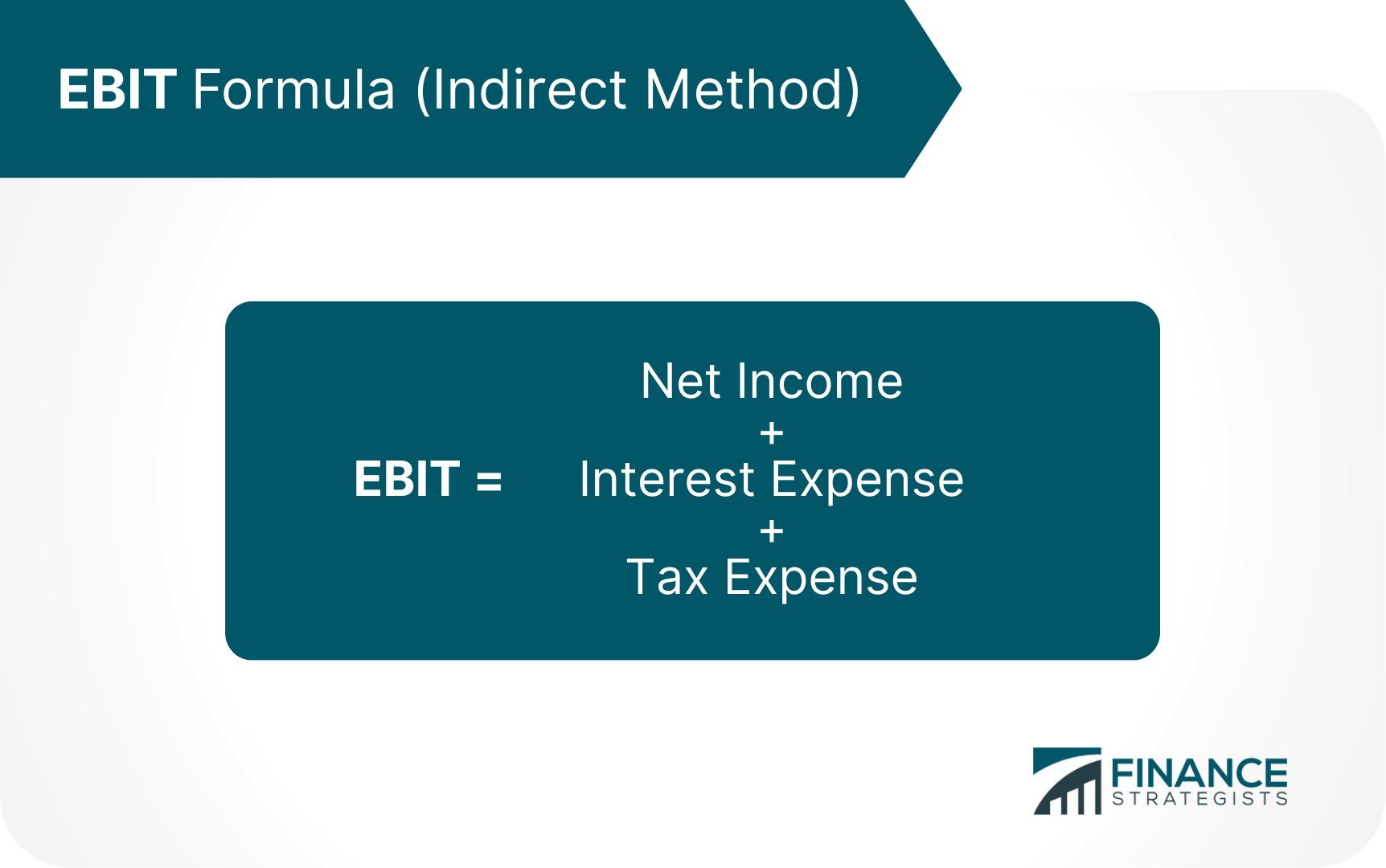

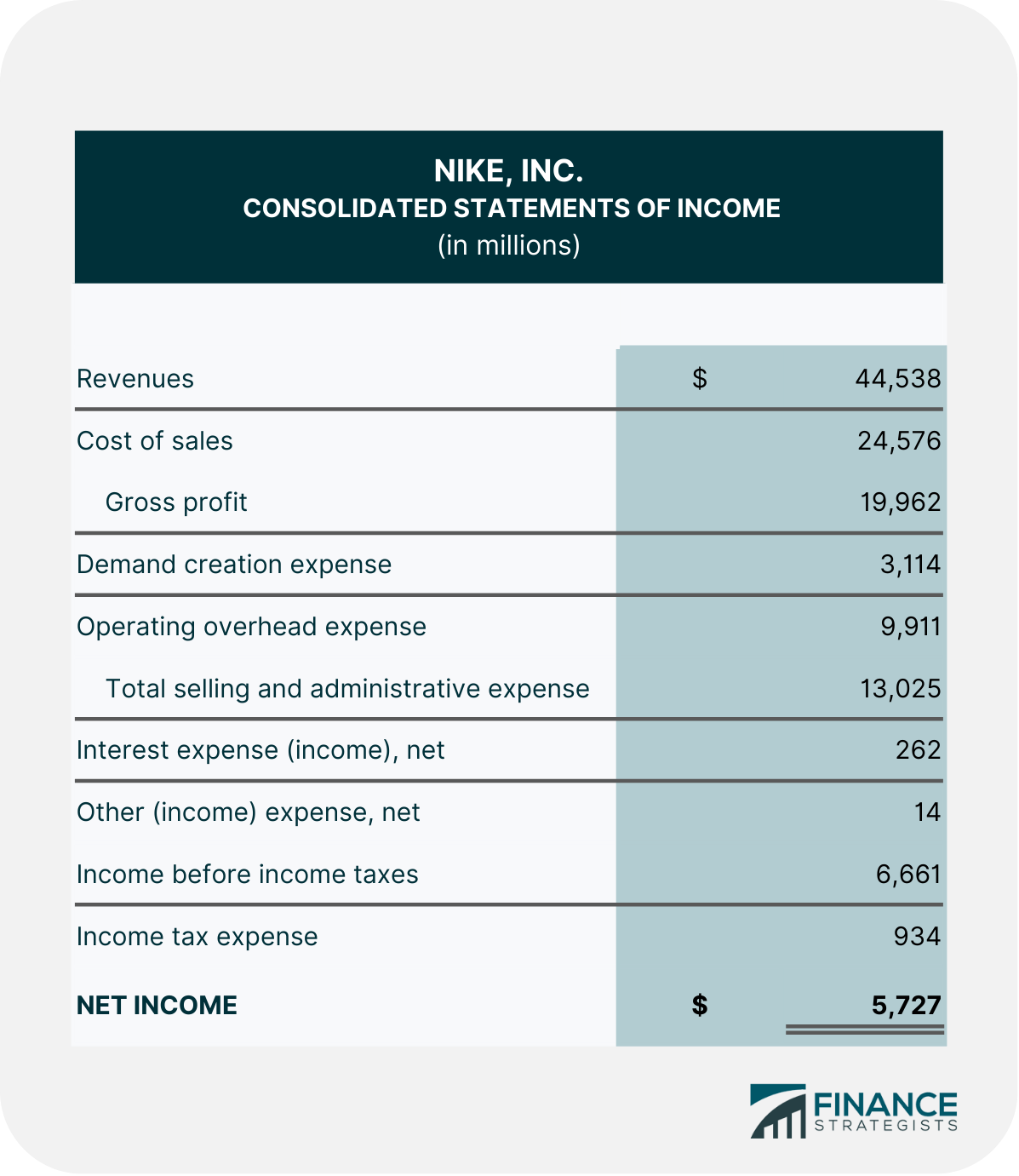

Earnings Before Interest and Taxes (EBIT) is one of the various profitability metrics for businesses. It can be calculated by deducting the cost of goods sold (COGS), operating expenses, and non-operating expenses from sales revenue and then adding any non-operating revenue. Although considered as non-operating items, interest and tax expenses are excluded from the calculation of EBIT for the purpose of gauging a company's profitability without the impact of its capital structure and tax expenses. Often, EBIT is referred to as operating profit or operating income. This is true when there are no non-operating items to be accounted for. For this reason, most resources on the matter do not make that distinction although it is important to understand that they are two different measures of profitability. EBIT is a helpful metric in monitoring the ability of the company to earn enough to deliver profits to the business, pay down debt, and fund its daily operations. The components of EBIT are as follows: Revenue is the total amount of money that a company brings in from its sales and other activities over a given period of time. It is often calculated by multiplying the sales price by the number of units sold. Revenue is also called sales or the top line in the income statement, where the COGS is subtracted to determine gross profit. COGS include all direct costs associated with producing the goods or services that were sold. It involves direct labor costs, material costs, and manufacturing overhead. COGS reveals how much a business had invested in its inventory that it sold throughout a certain period. It excludes those indirect expenses, such as sales force costs and distribution costs. Operating expenses can include items such as rent, utilities, employee salaries, and other day-to-day expenses that are required to keep the business running. Thus, operating expenses are the expenses that a company must make to conduct its operational activities. Non-operating items are further classified into non-operating revenue and non-operating expenses. These include proceeds from sale of extraordinary items, lawsuit expenses, and certain accounting adjustments. These items are added/subtracted from operating profit before EBIT is reached. While interest and taxes are also non-operating items, they are excluded from the calculation of EBIT. EBIT can be calculated by two methods: The first method of calculation is more commonly used. The formula for EBIT can be expressed as: In instances where there are no non-operating items to account for, the formula can simply be: The resulting figure will be equal to operating profit. This method shows directly what is taken out of earnings. This gives more of a preliminary operations point of view. The formula for EBIT using the indirect method can be expressed as: The indirect method begins with the net income of the company and adds back the interest and tax expenses. This method is straightforward since these items are always displayed on the income statement. The indirect method gives an end-period profitability point of view. Direct and indirect methods arrive at the same EBIT figure and allow business owners and investors to understand the profitability ratio from two different points of view. For instance, ABC Company has the following revenues and expenses: Using the direct method, we calculate EBIT as follows: EBIT = Revenue - COGS - Operating Expenses + Proceeds from Sale of Asset - Lawsuit Expenses = $500,000 - $250,000 - $50,000 + $3,000 - $2,000 = $201,000 Using the indirect method, calculating EBIT will be: EBIT = Net Income + Income Tax + Interest Expense = $151,000 + $25,000 + $25,000 = $201,000 Using either equation or method, the EBIT for ABC Company is $201,000. Another example is the income statement of Nike, Inc. from the year ending May 31, 2021 (all figures in millions of USD): To calculate EBIT using the direct method, we subtract the cost of sales or COGS, total selling and administrative expense, and other expenses from revenues. EBIT = $44,538 - $24,576 - $13,025 - $14 = $6,923 To calculate EBIT using the indirect method, we add income tax expense, and interest expense to the net income. EBIT = $5,727 + $934 + $262 = $6,923 From both examples we had above, we can see non-operating items (proceeds from sale of asset, lawsuit expenses, and other expenses) that need to be accounted for. These non-operating items inflated the EBIT figure, but not the operating profit figure. For this reason, it is not always safe to assume that operating profit is the same as EBIT. There are a number of advantages to knowing EBIT. Here are a few of them: EBIT is a good indicator of how well a company is doing compared to its competitors. If two companies are in a similar industry and one company has a higher EBIT, this means that the company is more profitable. When the company has a lower margin, an analysis of EBIT will reveal whether the lower margin is exclusive to the company only or is due to a slow down of the overall industry. Business metrics, such as ratio analysis, depend on including EBIT in the calculation. Creditors also closely monitor EBIT figures to give them an idea of pre-tax cash generation for paying back loans or debts. EBIT is a good indicator of how well a company is run. A high EBIT margin indicates that the company has good operating efficiency. There are also some disadvantages to using EBIT: EBIT will exaggerate the earnings potential of a company while it also owes a large amount of debt or loan. It will display a high cash flow based on EBIT alone, but in reality, that cash might be used to pay interest expenses. Having a large number of fixed assets may give a company a lower present-day valuation compared to another company because of the depreciated value of fixed assets. EBIT and operating profit are both essential metrics in the analysis of the financial performance of a company. However, EBIT and operating profit could be different. Here is a comparison table between EBIT and operating profit. Both EBIT and earnings before interest, taxes, depreciation, and amortization (EBITDA) are ways of measuring the profits of a company. While closely similar, they also differ in some critical ways and fundamentally measure two different forms of income. Here is a comparison table between EBIT and EBITDA. Earnings Before Interest and Taxes (EBIT) is a metric used to measure a company's profitability. It is calculated by adding interest and tax expenses back to net income. The direct method begins with deducting the cost of goods sold and operating expenses from the revenue. The resulting figure is then added to the non-operating revenue and deducts any non-operating expenses except for interest and taxes. The indirect method uses the net income of the company and adds back the interest and tax expenses. There are also a number of advantages and disadvantages to using EBIT as a profitability metric. Some advantages include that it is a good indicator of how well a company is doing compared to its competitors and that it is a good indicator of operating efficiency. Some disadvantages include that it excludes interest expenses and includes depreciation. Excluding interest expenses will overvalue the earnings potential of a company while it also still owes a large amount of loan or debt. Including depreciation also gives the company a lower present-day valuation compared to its competing company. EBIT is a good profitability metric to use when analyzing a company. However, it is important to keep in mind its limitations. When used correctly, EBIT can give you a good idea of how profitable a company is. EBIT is just one metric that can provide insights into a company's profitability. Thus, it is important to use a variety of metrics when analyzing the financial performance of a company.What Is Earnings Before Interest and Taxes (EBIT)?

Components of Earnings Before Interest and Tax

Revenue

Cost of Goods Sold

Operating ExpensesNon-Operating Items

Formula and Calculation for EBIT

Direct Method

Indirect Method

EBIT Examples

Advantages of EBIT

Helps Investors Or Analysts Compare Companies In Similar Industry

Other Metrics Depend On It

Indicates Operating Efficiency

Disadvantages of EBIT

Exclude Interest Expenses

Includes Depreciation

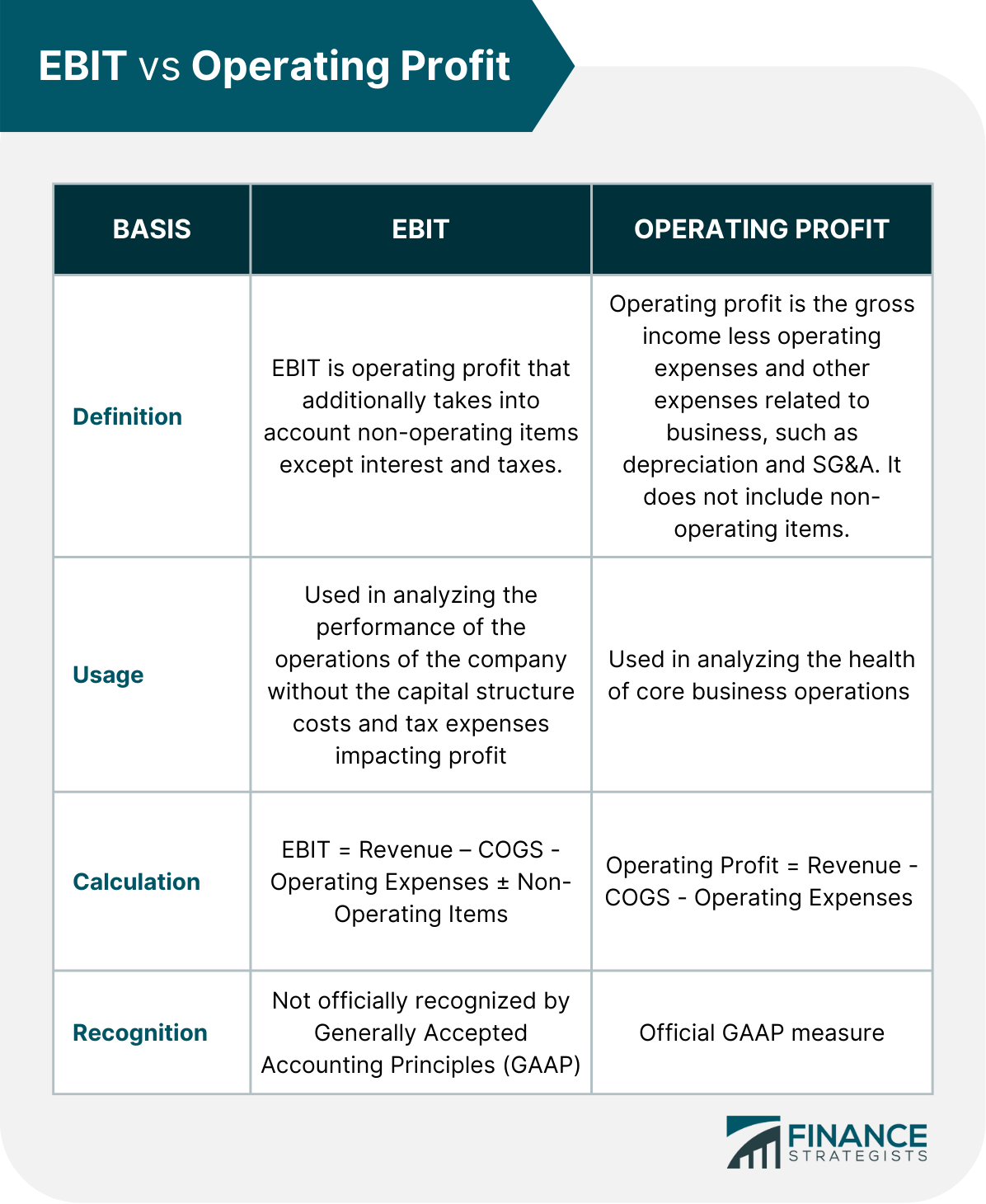

EBIT vs. Operating Profit

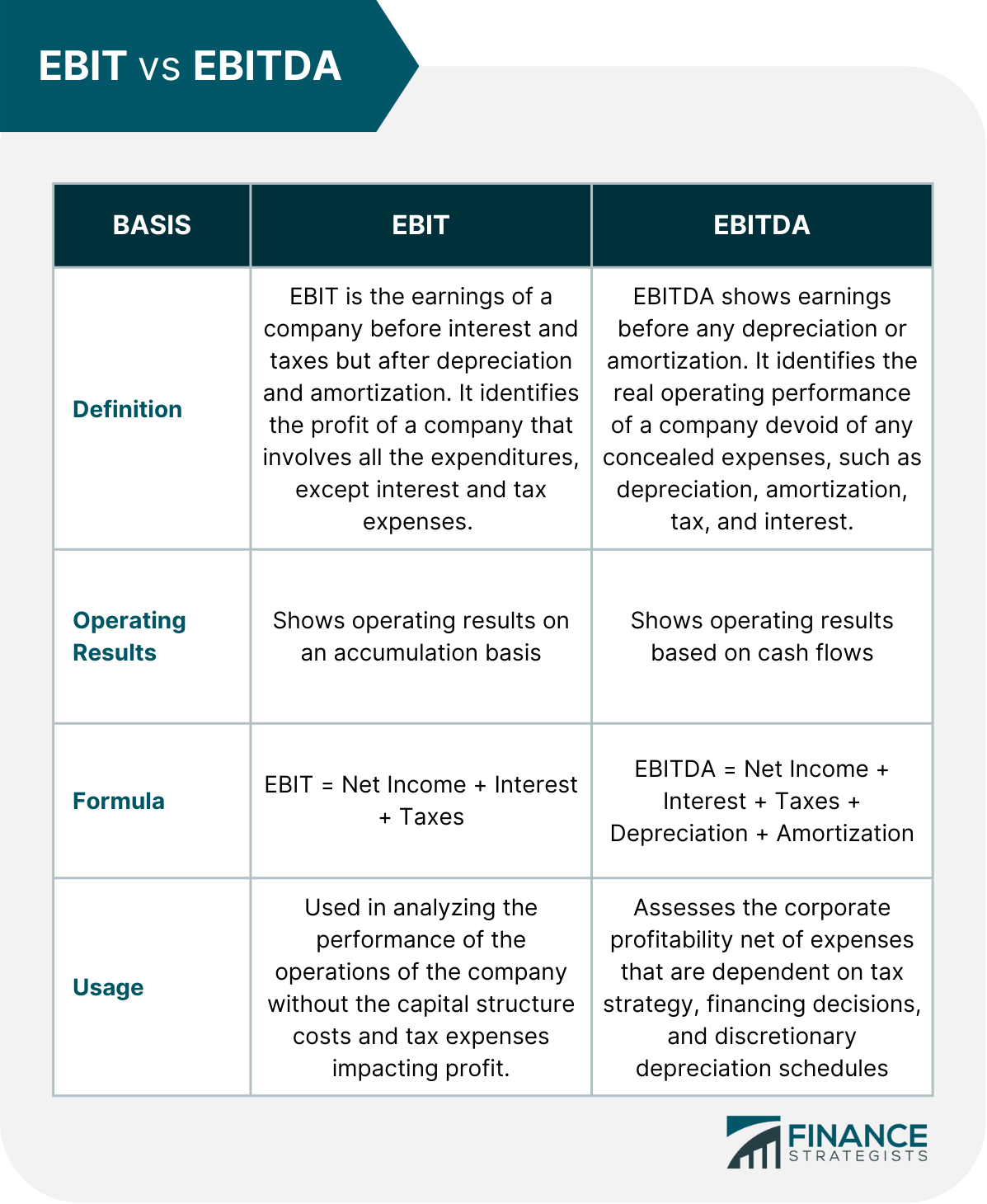

EBIT vs. EBITDA

The Bottom Line

Earnings Before Interest and Taxes (EBIT) FAQs

EBIT is used in analyzing the performance of the operations of the company without the capital structure costs and tax expenses impacting profit.

When your EBIT increases, it also increases your bottom line or net profit. It also shows the lenders that you have a high ability to pay your debts. Using EBIT, investors can tell that your company can generate enough earnings to be profitable and fund its daily operations.

Direct Method: EBIT = Revenue - Cost of Goods Sold - Operating Expenses ± Non-Operating Items Indirect Method: EBIT = Net Income + Interest + Tax

Analysts and investors use EBIT to assess a company's operating profitability. It is used to compare companies within the same industry because it eliminates the impact of a company's capital structure and tax rate. It also reveals whether the company generates enough profits and is able to fund ongoing operations.

The core difference between EBIT and operating profit is that EBIT takes into account non-operating items (except interest and taxes), such as proceeds from sale of assets and litigation expenses, while operating profit does not.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.