Financial advisors are professionals that guide their clients toward making intelligent financial decisions. They offer advice and services related to investments, retirement, estate planning, tax strategies, insurance, and other related topics. They have the experience to effectively assess a client’s financial situation and provide tailored solutions. Although clients can always manage their finances independently, financial advisors offer a neutral perspective that may not otherwise be available. Ultimately, working with a financial advisor can help you achieve your financial goals faster and more efficiently. However, since your choice of a financial advisor may significantly impact your finances, it is essential to be informed and ask the right questions before selecting one. Have a question for a Financial Advisor? Click here. Here are 12 questions to consider when researching and interviewing potential advisors: A fiduciary is a financial professional with a legal obligation to act in their client’s best interests. They must adhere to high standards of ethics when providing financial services and advice. Simply put, they are expected to place their client's interests ahead of their own. Financial advisors registered with the Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA) are fiduciaries and must abide by regulations. However, not all financial advisors are expected to act as fiduciaries. Some advisors only abide by the suitability standard, meaning they can offer products that are merely acceptable instead of the most appropriate one for their client. A financial advisor who is required to act as a fiduciary has increased accountability. Thus, clients can rest assured that their advisor’s recommendations and services are being given for their sake and not just to earn a commission. Financial advisors can provide various services tailored to meet their clients' needs. A good one will take the time to understand your life stage and objectives before recommending any particular strategy or product. The following are examples of services financial advisors can provide: Whichever life stage you are in, check if your prospective financial advisor is offering services that match your goals, needs, and expectations. An investment philosophy is a set of principles and beliefs that guide decisions about investing. It can include the desired rate of return, the level of risk they are willing to take, the types of investments they feel comfortable with, and overall financial goals. A potential financial advisor should be able to explain how they make decisions when selecting investments and why they believe specific strategies will generate the most significant returns for you. It is vital that your investment philosophies are aligned, as you will be counting on the financial advisor to make decisions about your money. Open communication about their beliefs and how they may differ from yours will help ensure a successful partnership. Financial advisors can serve individuals and families, companies, trusts, or other organizations. They can work with clients with various financial goals, such as retirement planning, estate planning, investment management, or tax preparation. Many advisors specialize in specific areas and a certain clientele, such as high-net-worth individuals, business owners, or retirees. They should be able to provide information regarding the types of clients they have served in the past and what solutions they provided for them. This will give you a better understanding of how successful the advisor has been in helping clients achieve their financial objectives. Knowing an advisor’s typical clientele will also help determine if their services suit your needs. A good financial advisor can provide proof of their licenses, credentials, education, and experience. These qualifications help you gauge the competence of your potential financial advisor. Depending on the type of services you need, you can check if your potential financial advisor holds certifications like Chartered Financial Analyst (CFA), Certified Financial Planner (CFP), or Certified Public Accountant (CPA). Then, you must ensure they are appropriately registered by checking SEC’s Investment Adviser Public Disclosure (IAPD)website, FINRA's BrokerCheck tool, or contacting your state's regulators for additional information. Finally, it is also good to check if they are members of professional organizations that require their members to adhere to certain standards when providing their services. An excellent example is the National Association of Personal Financial Advisors (NAPFA). Financial advisors earn in different ways. The following are the most common financial advisor fee structures: It is vital to understand the fee structures associated with a particular advisor before engaging in any services. You can begin by asking if your potential financial advisor is fee-only or fee-based. Fee-only advisors charge hourly, flat, or AUM fees. In contrast, fee-based advisors offer similar fee structures, but they may also earn a commission from selling products or services, which increases their potential conflict of interest. It is also essential to determine if other costs are associated with an advisor’s services, such as custodial fees, tax preparation fees, research fees, or account maintenance fees. Asking all these ensures you understand what you are paying for and if it is within your budget. Financial advisors need to communicate with their clients regularly. This will allow them to keep their clients informed about any changes in the market or new investment opportunities that may arise. Typically, advisors meet clients face-to-face, but some also offer personalized email or phone updates as needed. Some advisors prefer to meet with clients quarterly, while others are comfortable meeting bi-annually or monthly. Ultimately, it is up to both parties to determine how often communication will be. Be sure to discuss your expected frequency and mode of contact with your financial advisor before signing any documents. Confidentiality and security are paramount. This is because you might provide your financial advisor with sensitive details not only about your finances but also about your professional and personal life, depending on the particular services you require of them. Therefore, it is essential to ask your potential financial advisor what security measures they have to protect your data and if they share any of your personal information with third parties. Your financial advisor should be able to provide a record of anyone outside their firm who has had access to your confidential information. Additionally, they must ensure that their IT infrastructure meets all applicable cybersecurity and data protection regulatory requirements. A financial advisor should be able to provide you with a complete assessment of your current financial situation, including your investments, income, and expenses. They should then offer a plan for how to reach your desired goals. Finally, an advisor should produce regular reports that clearly outline how their services impact your finances. This allows you to track progress and hold them accountable for delivering results. Measuring progress towards your goals can be done by tracking the return on investment (ROI), reviewing the portfolio performance each quarter, and evaluating whether the goals set at the beginning of the engagement are being met. Other metrics include monitoring cash flow, net worth, and liquidity and comparing savings against expected outcomes. It is crucial to have continuity of service even when the primary financial advisor is unavailable. A good financial advisor should provide an alternate representative who can assist in all service areas, including investment management and financial planning. This includes having technology solutions, such as automated payments and online services, that can help minimize disruption if the advisor is unavailable. They should also have a backup system in place so there are no surprises if they cannot communicate with you. Access to multiple people means that no matter what life throws at you, someone is there to care for your interests. Disclosures are public records that provide information about the financial advisor’s compliance with industry regulations. These records may be filed with regulatory agencies or other state and federal authorities, such as the SEC or FINRA. Aside from asking your potential financial advisor this question, you can also check the actual records from government agencies. For instance, you can use the SEC Action Lookup - Individuals (SALI) to confirm their answers. The disclosure documents will provide detailed information regarding previous complaints, investigations, disciplinary actions, or client disputes involving your potential financial advisor. Performing due diligence when researching potential advisors is essential to make an informed decision about whom you are entrusting with your finances. It would be best to stay up-to-date on changes made to their record over time. Some advisors may require that their clients have a certain amount of assets before they accept them as a client. Knowing this information is essential in determining whether or not a particular financial advisor is the best fit for you and your goals. The minimum investment requirement is usually determined by the complexity of an advisor’s services and how much work it takes to manage those investments properly. For instance, some advisors charge AUM fees, while others charge a fee based on how much time they spend managing your portfolio. Therefore, if an advisor has a minimum investment requirement that does not currently meet your own, you will want to consider other options. Be sure to ask whether or not the minimum investment requirement is flexible. Some advisors may be open to waiving this requirement if they find that you are a good fit for their services and have an understanding of your financial goals. Finding the right financial advisor for you can seem daunting. However, by asking the right questions and performing due diligence, you can be confident that you are making the best decision for your future. When selecting a financial advisor, be sure to ask your candidates questions about crucial factors, such as their qualifications, fee structure, investment philosophy, client base, and services provided, to understand how they operate and if they will be a good fit for you. By taking these precautions before signing on with any particular advisor, you can have peace of mind knowing that your financial affairs are being managed by the very best.Why Hire a Financial Advisor?

Question #1: Are You a Fiduciary?

Question #2: What Services Do You Provide?

Question #3: What Is Your Investment Philosophy?

Question #4: Who Are Your Typical Clients?

Question #5: What Are Your Qualifications?

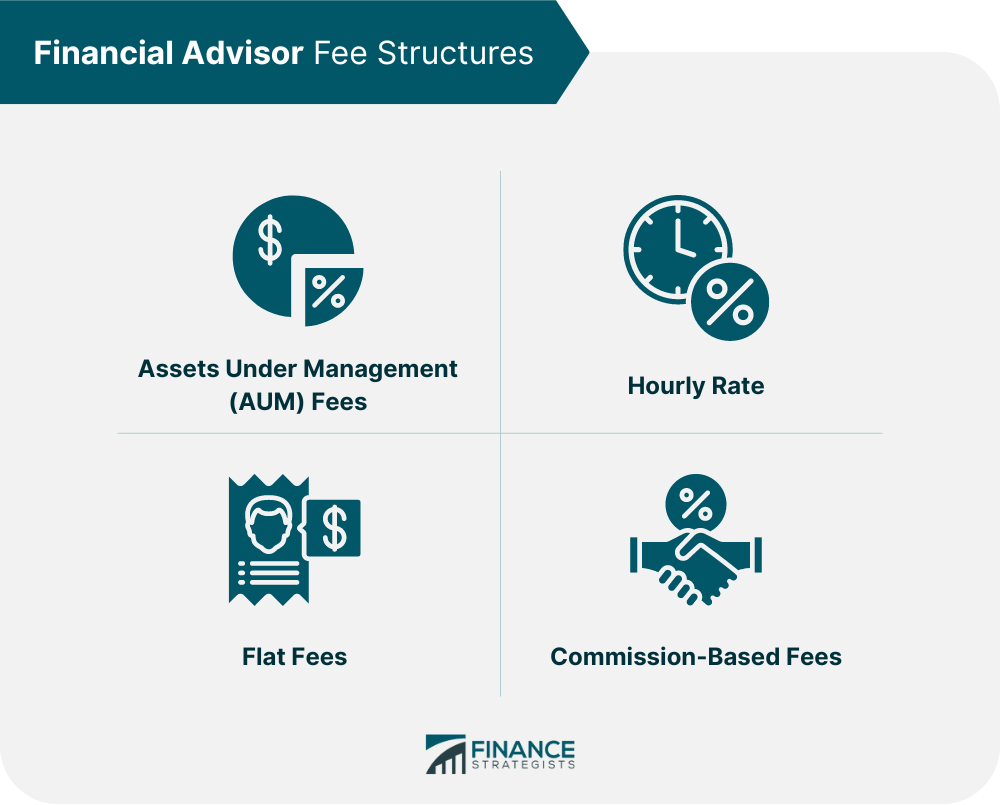

Question #6: What Is Your Fee Structure?

Question #7: How Often Do You Communicate With Your Clients?

Question #8: Who Will Have Access to My Information?

Question #9: How Will We Measure Progress?

Question #10: Who Will Be Available to Work With Me in Your Absence?

Question #11: Do You Have Any Disclosures on Your Record?

Question #12: Do You Have a Minimum Investment Requirement?

Final Thoughts

12 Questions to Ask a Financial Advisor FAQs

A Financial Advisor provides comprehensive and personalized advice on various aspects of personal finance, such as investment planning, retirement planning, estate planning, and taxation.

Financial Advisors typically have extensive experience in the field, covering all areas of financial planning and wealth management, including investments, retirement planning, tax strategy, estate planning, and insurance.

You should meet with your Financial Advisor regularly (at least once a year) to review your progress toward your financial goals and discuss any changes that may be necessary.

Most Financial Advisors will charge a fee for their services, either on an hourly basis or as a percentage of the assets they manage. However, some advisors may offer free services such as basic financial planning advice.

When choosing a Financial Advisor, it is important to make sure they are appropriately qualified and experienced. Look for someone who has earned certifications such as the Certified Financial Planner (CFP) designation or other qualifications such as a Chartered Financial Analyst (CFA) or Chartered Investment Manager (CIM). Additionally, check that the advisor is registered with a professional body such as the Financial Services Commission of Ontario (FSCO).

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.