A Fee-Only Financial Advisor is a professional who charges clients solely based on the services they provide. Their fee structures can offer options such as hourly fees, flat fees, or percentage of assets managed. Unlike fee-based financial advisors, they do not receive any commission or other forms of compensation for selling financial products, such as mutual funds or insurance policies. This means that the potential for personal financial gain may not influence their advice and recommendations. Thus, they can offer more objective and unbiased advice to their clients. A Fee-only financial advisor can be identified by studying their Form ADV (Uniform Application for Investment Adviser Registration) on the U.S. Securities and Exchange Commission (SEC)’s public disclosure website. These advisors usually display the following information in their form: One way to tell if a financial advisor is fee-only is to check their compensation structure. A fee-only financial advisor should not receive transaction-based compensation, such as commissions or referral fees. When asked, they should be able to provide a clear explanation of how they are compensated, and it should be based solely on the fee they charge for their services. Another way to identify a fee-only financial advisor is to check if they also work as a broker-dealer or if they are affiliated with any broker-dealer firms. Broker-dealers are financial professionals who buy and sell securities on their client's behalf and may receive commissions or other forms of compensation for these transactions. On the other hand, fee-only financial advisors do not engage in these transactions and are not generally affiliated with broker-dealer firms. In addition, a fee-only financial advisor should not have any sales interests with broker-dealers. This means they should not receive compensation or incentives for recommending or selling financial products from a particular broker-dealer. Hiring a fee-only financial advisor has many advantages, including the following: One advantage of using a fee-only financial advisor is that they have less conflict of interest. Because they do not receive any commissions or other forms of compensation for selling financial products, clients are more likely to be offered products most suited to their needs. Fee-only financial advisors are also more likely to be required to act as fiduciaries, which means they are legally bound to work in the best interests of their clients. This can reassure clients that their financial advisor is looking out for them and is not motivated by personal financial gain. Since they have less conflict of interest and are often required to act as fiduciaries, fee-only financial advisors generally offer more objective advice to their clients. Thus, they can recommend the best options for their clients without being influenced by potential financial gain. While there are advantages to hiring fee-only financial advisors, it is essential to note that there are also several disadvantages, such as: Fee-only financial advisors can be more expensive than fee-based financial advisors because they might need to charge higher fees to make a living. In addition, potential clients might need to spend more when they obtain products, such as insurance from other providers. Thus, fee-only financial advisors may not be suitable for individuals or families on a tight budget or those requiring only a limited amount of financial advice. Fee-only financial advisors may be limited in their services and products. Since they are not affiliated with service providers like insurance companies or broker-dealers, they may not have access to the same products or services that fee-based financial advisors do. This can limit the options available to clients. Thus, fee-only financial advisors may not be suitable for those who require a more comprehensive range of financial services. To find a reliable fee-only financial advisor, you can start by researching online to find candidates in your area. You may utilize trusted online resources such as the National Association of Personal Financial Advisors (NAPFA)website. NAPFA is a professional organization that only allows financial advisors who meet their strict standards for professional conduct and independence to become members. Advisors who are members of NAPFA are required to be fee-only and adhere to a fiduciary duty. Alternatively, you can also ask for personal recommendations from friends, family, or colleagues who have previously worked with a fee-only financial advisor. Whether you search online or ask for recommendations, you must perform due diligence and research your prospective advisor's credentials and qualifications before choosing one. Make sure to ask relevant questions to further check on their background. Fee-only financial advisors charge clients hourly fees, flat fees, or percentage of assets managed. Some are registered and required to act as fiduciaries, meaning they are legally bound to work in their client's best interests. They also do not receive any commission or other forms of compensation for selling financial products, such as mutual funds or insurance policies. Thus, their potential for conflict of interest is low. On the other hand, fee-based financial advisors offer the same fee structures, including hourly fees, flat fees, or percentage of assets managed. However, they may also receive commissions, referral fees, or other forms of compensation for selling financial products. They are also less likely to be registered and required to act as fiduciaries. This means the potential for conflict of interest is high, and personal financial gain could influence their advice or recommendations. Selecting the right financial advisor for your individual needs is an important decision. Thus, it is essential to evaluate whether hiring a fee-only or fee-based advisor will serve you best. Fee-only advisors may provide more objective advice since their potential for conflict of interest is low. Some are also registered as fiduciaries and are legally bound to make decisions that prioritize their client's interests first. However, fee-only financial advisors can be more expensive than fee-based financial advisors because they might need to charge higher fees to make a living. Since they are not affiliated with service providers, they may be limited in the services and products they can offer. In contrast, fee-based financial advisors may offer a wider range of services and products. However, their advice and recommendations may be influenced by the potential for personal financial gain since they can accept compensation for selling financial products. Whichever option you choose, you must perform due diligence. You can do this by researching the credentials and qualifications of your prospective financial advisor. It is also crucial to ask about their compensation structure and check for potential conflicts of interest.What Is a Fee-Only Financial Advisor?

How to Identify a Fee-Only Financial Advisor

Non-Transaction-Based Pay Structure

Not Connected to Broker-Dealers

No Sales-Based Interests With Brokers

Advantages of Hiring a Fee-Only Financial Advisor

Has Less Conflict of Interest

May Be Required to Act as a Fiduciary

Can Offer Objective Advice

Disadvantages of Hiring a Fee-Only Financial Advisor

Can Be More Expensive

May Provide Limited Products and Services

How to Find a Fee-Only Advisor

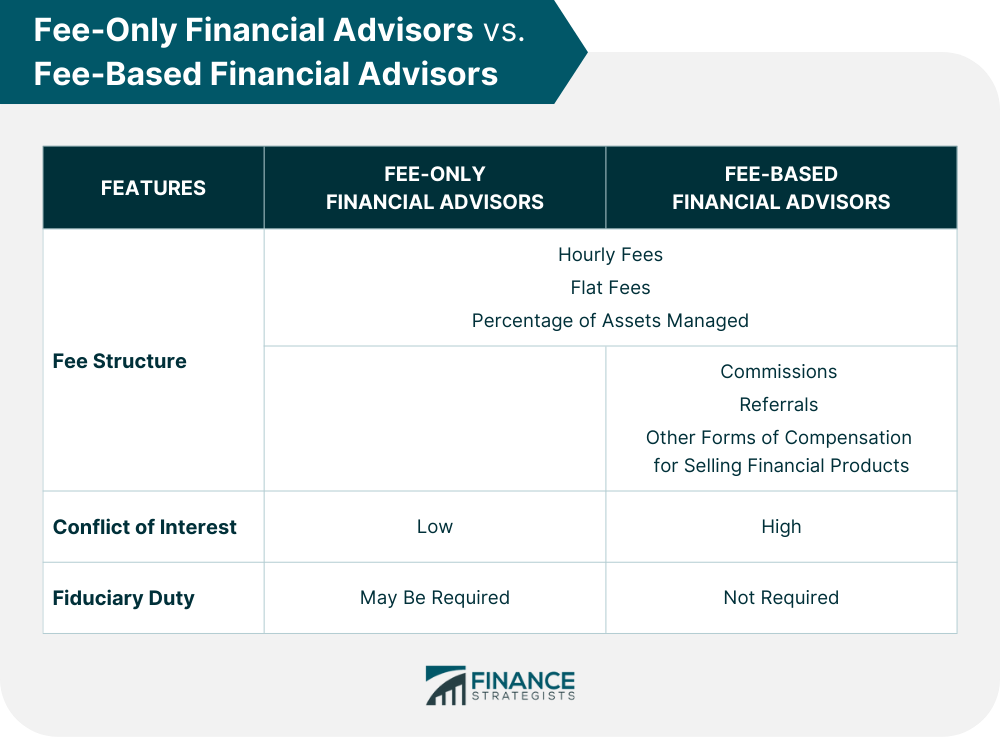

Fee-Only Financial Advisors vs Fee-Based Financial Advisors

The Bottom Line

How to Find a Fee-Only Financial Advisor FAQs

To determine whether a financial advisor is fee-only, study their Form ADV on the SEC’s public disclosure website. Check if they offer a non-transaction-based pay structure and verify that they are connected with or receiving sales-based interest from broker-dealers.

The advantages of using a fee-only financial advisor include more objective advice, lesser conflicts of interest, and a higher possibility of being registered as a fiduciary who is required to act in the best interests of their clients.

Fee-only financial advisors charge clients hourly fees, flat fees, or percentage of assets managed. They do not receive any commission or other compensation for selling financial products. Meanwhile, fee-based financial advisors offer similar pay structures, but they also receive commissions or other forms of payment for selling financial products.

Fee-only financial advisors typically charge a percentage of the assets they manage on behalf of the client, an hourly rate, or a flat fee. The exact cost will depend on the advisor's experience and the services they provide. Thus, before selecting a financial advisor, asking about the fee structure and any additional charges upfront is essential.

To find a fee-only financial advisor, you can research online for possible advisors in your area or ask for recommendations from trusted individuals who have previously worked with one. Whichever selection method you choose, you must perform due diligence and research the advisor's credentials and qualifications before choosing one.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.