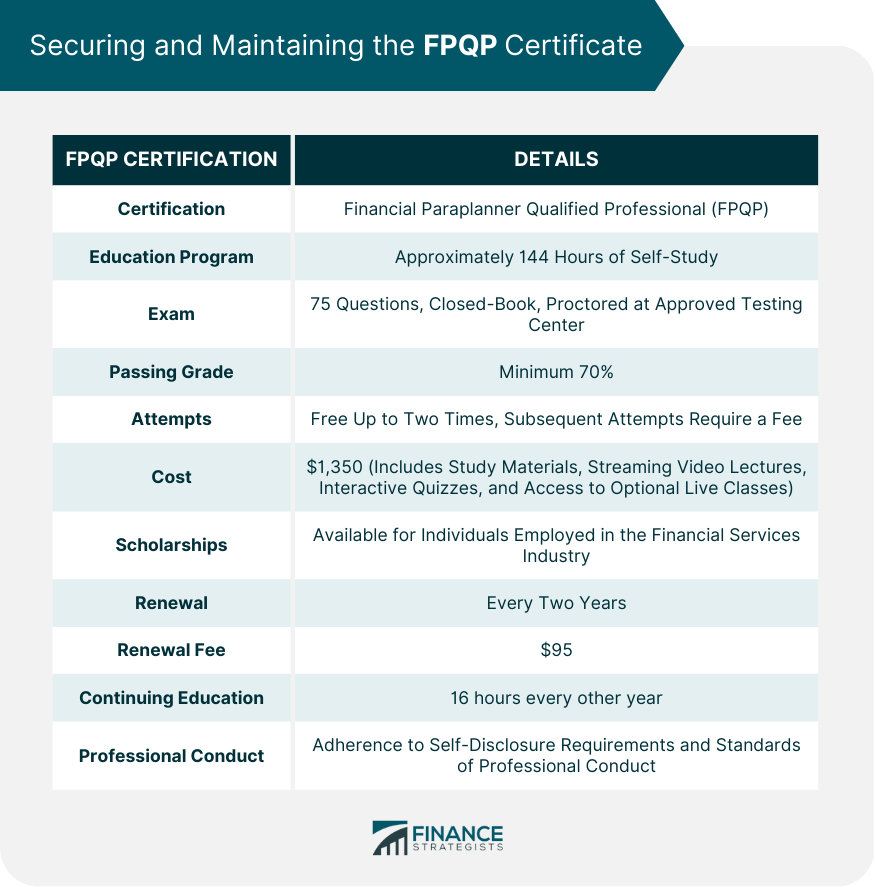

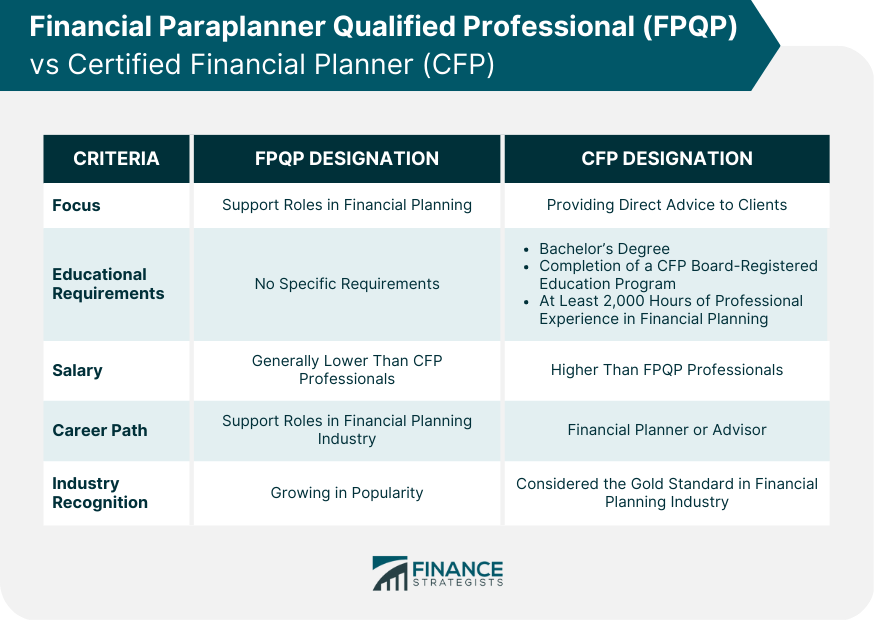

A Financial Paraplanner Qualified Professional is a professional who has achieved certification through the College for Financial Planning (CFFP). The FPQP certification is a formal certification program that teaches individuals the knowledge and skills required to work as a financial paraplanner. The importance of FPQP certification for a career in financial planning cannot be overstated. The certification demonstrates that a professional has achieved a certain level of expertise in financial planning, which helps them better advise their clients. FPQP professionals are different from most paraplanners because the average paraplanner rarely has a formal certification. Have a question for a Financial Paraplanner Qualified Professional? Click here. Financial paraplanners are an integral part of a financial planning team, providing support services to financial planners and advisors. The responsibilities and duties of a financial paraplanner can vary depending on the specific needs of the financial planning team. The following table provides information on the responsibilities and skills required to become an effective FPQP. The College for Financial Planning – a Kaplan Company, offers the FPQP certification program. This program is designed for individuals who want to enter the financial services industry or deepen their knowledge of the foundational aspects of financial planning. The program gives students an opportunity to earn the FPQP designation, which is recognized and offered by the College. To be eligible for the program, there are no prerequisites required. The program is open to individuals who are new to the industry and those with some experience in the financial services profession. The FPQP certification program is offered through two learning modalities: Live Online Classes and OnDemand Classes. Live Online Classes are instructor-led and best suited for individuals who prefer a structured schedule to stay on track with completing the program. OnDemand Classes are self-paced and best suited for individuals who need flexible learning schedules. The program covers various topics, such as financial planning, insurance, investments, retirement, estate planning, taxes, and business ownership. Once enrolled, students must complete the online self-study FPQP course and exam within 120 days of receiving program access. Students can also choose the instructor-led option based on availability. The FPQP certification exam is an online, closed-book final exam. The exam assesses the student’s knowledge of the program material and is in a multiple-choice format with 75 questions. Students must achieve a minimum passing grade of 70% to receive their certification. Upon completion of the FPQP certification program, graduates receive an exemption from course FP511 in the College’s CFP certification education program. Additionally, completion of professional designation programs can help fulfill continuing education (CE) requirements. If a student currently holds a professional designation from the College, completing a new professional designation fulfills CE hours as part of the renewal of their current designation. Obtaining the Financial Paraplanner Qualified Professional certificate involves completing the FPQP education program, designed for approximately 144 hours of self-study. However, the amount of time needed for preparation can vary from person to person. Students must attempt the FPQP final exam within six months of enrolling in the program and pass it within one year of enrollment. The exam comprises 75 questions and is closed-book and proctored at an approved testing center. The minimum passing grade is 70%, and students can take the exam for free up to two times. After the first two attempts, subsequent attempts require a fee. Enrolling in the education program costs $1,350, which includes all study materials, streaming video lectures, interactive quizzes, and access to optional live classes. The College for Financial Planning offers program scholarships for individuals currently employed in the financial services industry. Certificate holders must renew their certification every two years and pay a biennial renewal fee of $95. They must also complete 16 hours of continuing education every other year to maintain their certification. Additionally, the College requires certificate holders to comply with self-disclosure requirements and adhere to standards of professional conduct. The FPQP designation offers several benefits for individuals pursuing a career in the financial services industry. Individuals who earn the FPQP designation have a solid foundation in financial planning and are well-equipped to work as paraplanners or in other support roles in financial planning. The certification program is designed to cover all major facets of personal financial planning, providing students with comprehensive knowledge that can be used to assist financial planners and advisors and for individual financial situations. Based on data from salary.com, the typical salary range for Financial Paraplanners is between $54,626 to $73,656, with an average salary of $63,099 as of January 27, 2024. The actual salary amount may vary depending on factors such as education, certifications, experience, and additional skills. Compared to other financial planning certifications, the FPQP certification offers a more practical application and foundation of financial planning knowledge, ensuring a comprehensive understanding of personal financial planning facets. The FPQP mark can set you apart from other paraplanners because it demonstrates you have the knowledge and expertise to provide advice to clients as part of an effective financial planning team. Additionally, earning the designation is a sound financial decision, as FPQP graduates can generally expect a pay increase after earning the such designation. Moreover, the certification can help with future education plans, as earning the designation provides credit for completing FP511 in the CFFP CFP certification education program, saving both time and money in pursuing multiple credentials. Financial Paraplanner Qualified Professional and Certified Financial Planner (CFP) are both important designations for those interested in pursuing a career in financial planning. However, there are key differences between the two. One major difference is that the FPQP designation is geared more toward support roles in financial planning, while the CFP designation is more focused on providing direct advice to clients. The CFP designation is often seen as the gold standard in financial planning and best suits those who want to work directly with clients to develop comprehensive financial plans. On the other hand, the FPQP designation is ideal for those who want to work in support roles in the financial planning industry, such as paraplanners, client service associates, or other support staff. Another difference between the two designations is the required level of education and experience. The FPQP designation does not have any specific educational or experiential requirements, while the CFP designation requires a bachelor's degree, completion of a CFP Board-registered education program, and at least 2,000 hours of professional experience in financial planning. When it comes to salary, CFP professionals generally earn higher salaries than FPQP professionals. According to the latest available Bureau of Labor Statistics, the median annual wage for personal financial advisors, which includes CFP professionals, is $95,390. However, FPQP professionals can still earn competitive salaries depending on their experience, education, and other factors. In terms of career paths, the CFP designation is best suited for those interested in becoming financial planners or advisors, while the FPQP designation is more geared toward those who want to work in support roles. Both designations can lead to various career paths in the financial planning industry, including roles in banking, insurance, investment management, and more. Ultimately, choosing between the FPQP and CFP designations depends on an individual's career goals and aspirations in the financial planning industry. If you want to work directly with clients to develop comprehensive financial plans, the CFP designation may be the best fit. If you prefer a support role in the industry, the FPQP designation may be the better option. The Financial Paraplanner Qualified Professional certification program offered by the College for Financial Planning is designed to provide individuals with the knowledge and skills required to work as financial paraplanners. The program is open to individuals who are new to the industry and those with some experience in the financial services profession. There are no specific prerequisites or educational requirements to enroll in the program. After completion, individuals will be equipped with the skills and knowledge necessary to perform various duties, including gathering client information, conducting financial analysis and research, developing and implementing financial plans, communicating with clients about financial plans and investments, and preparing reports and financial statements. Earning the FPQP designation offers numerous benefits, such as better job opportunities, a solid foundation in financial planning, and potential salary increases. However, it is important to note that this designation is geared more towards support roles in financial planning, whereas the Certified Financial Planner designation is more focused on providing direct advice to clients. To secure and maintain the certificate, individuals must complete the education program, pass the final exam, and fulfill continuing education requirements. If you are interested in pursuing a career in financial planning or want to enhance your skills and expertise in the field, consider enrolling in the FPQP certification program. The program can help you stand out in the job market, improve your career opportunities, and provide you with comprehensive knowledge of personal financial planning facets. Take the first step towards your professional goals today and explore this certification program.What Is a Financial Paraplanner Qualified Professional (FPQP)?

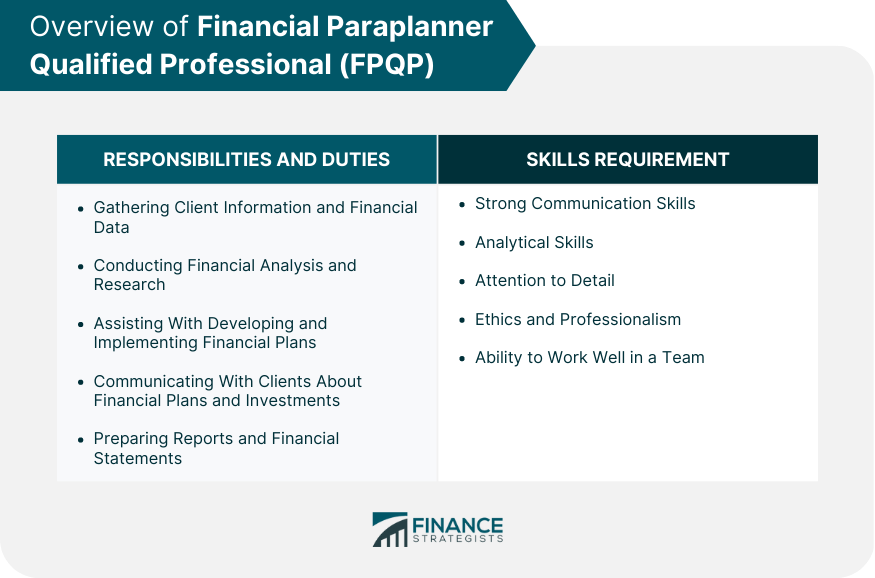

Responsibilities and Skills Requirement of a Financial Paraplanner Qualified Professional (FPQP)

FPQP Certification Program

Securing and Maintaining the FPQP Certificate

Benefits of the FPQP Designation

Career Opportunities for FPQP Professionals

Salary Expectations for FPQP

Skills Advantage of FPQP Certification

FPQP vs Certified Financial Planner (CFP)

Final Thoughts

Financial Paraplanner Qualified Professional (FPQP) FAQs

The FPQP certification is a formal certification program offered by the College for Financial Planning (CFFP) that teaches individuals the knowledge and skills required to work as a financial paraplanner.

The responsibilities of an FPQP include gathering client information and financial data, conducting financial analysis and research, assisting with developing and implementing financial plans, communicating with clients about financial plans and investments, and preparing reports and financial statements.

To become an FPQP, there are no specific prerequisites or education requirements. However, individuals who wish to become an FPQP should possess certain skills and qualifications, including strong communication skills, analytical skills, attention to detail, ethics and professionalism, and the ability to work well in a team.

The FPQP certification program is offered through two learning modalities: Live Online Classes and OnDemand Classes. Live Online Classes are instructor-led and best suited for individuals who prefer a structured schedule, while OnDemand Classes are self-paced and best suited for individuals who need flexible learning schedules.

FPQP certificate holders must renew their certification every two years and pay a biennial renewal fee of $95. They must also complete 16 hours of continuing education every other year to maintain their certification. Additionally, the College requires FPQP certificate holders to comply with self-disclosure requirements and adhere to standards of professional conduct.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.