Financial stability is a huge issue for many people. In recent years, the economy has been through some difficult times and as a result, families have struggled to keep their heads above water financially. Even those that were lucky enough to keep their jobs may have found that their salaries didn't go as far as they once did or that they no longer had the financial resources available to them in order to enjoy life's luxuries such as vacations and other outside activities. It can be very stressful when you don't know how much money will come into your household each month so being able to save up something for a rainy day or an unexpected expense can help ease this stress immensely. This article will discuss ways of achieving financial stability by saving money on various expenses. Financial stability is defined as the ability to maintain a steady income while avoiding debt. It may also involve both management of recurring household expenses and ensuring that there is adequate insurance against financial disruptions. Financial stability allows people to make reasonable plans for future expenses, save money for retirement or major purchases, invest in other things (such as education), and meet emergency expenses without incurring debt. It also helped by getting rid of existing debt, especially extreme debt, such as credit card debt or high-interest student loans. Financial stability can be achieved with asset management, wise spending habits, and adequate insurance coverage. Financial stability stems from having a working knowledge of the resources that are available to achieve financial security. There are many steps that you will have to take towards financial stability. Financial stability begins with a monthly budget. To increase your awareness, create a household budget and determine how much money is coming in and how much money is going out each month. Once you have determined where your money is going, you can then start to make changes that will allow for financial stability. For example, if there are several expenses that could be reduced, but are not absolutely necessary to have, you should cut them out of your monthly expenses. You can also set up an automatic transfer from checking to savings account for a certain amount every month. One thing that financial stability will require is having enough money set aside in case of an emergency. It is recommended that people set aside at least 3-6 months' worth of living expenses in case of an unexpected job loss or major expense. Create a buffer zone by saving up extra money each month, even if it is just $20, which you can use to cover emergencies before tapping the rest of your savings. Another way financial stability is achieved is by paying off debt and staying out of credit card debt. Keep your total monthly debt payments which include their mortgage, car loan, student loans, and credit cards to less than ten percent of your take-home pay Financial stability requires a certain amount of lifelong learning. Invest in yourself by taking classes, going to seminars, or reading books that will teach them new skills and help them grow as a person. The more knowledge you have the better your chances are of making good decisions about your financial matters. Start looking for new ways to make money and increase your total income. You need an action plan in order to achieve financial stability. It is a good idea that you set goals and stick with them, so try making a list of your financial goals and the steps you need to take to achieve them. Financial stability is not just about having money; it's also about how you use your money. Save up enough money to live comfortably during retirement, which is typically an average of 80% of your pre-retirement income. If you do not save enough for retirement, it can lead to financial problems later on in life such as having to work longer than planned or living a more frugal lifestyle than you would have liked to. Start saving for your retirement as early as possible because the benefits of compounded money are huge! The last step is having insurance coverage, which means having enough life, health, homeowners, car, and disability insurance to allow you to live comfortably. It is recommended to get enough life insurance coverage so that your dependents can continue living their lives even if you are not here anymore. Also, estate planning is also important if in case something were to happen. Financial Stability is accomplished by making a budget and sticking to it, saving up an emergency fund, staying out of debt and paying off debt, learning new skills that will allow for more income, setting goals, and then getting rewards as you meet those goals. Financial stability also requires having insurance coverage which means having enough life, health, homeowners, car, and disability insurance to allow you to live comfortably. It is recommended to get enough life insurance coverage so that your dependents can continue living their lives even if you are not here anymore. What Is Financial Stability?

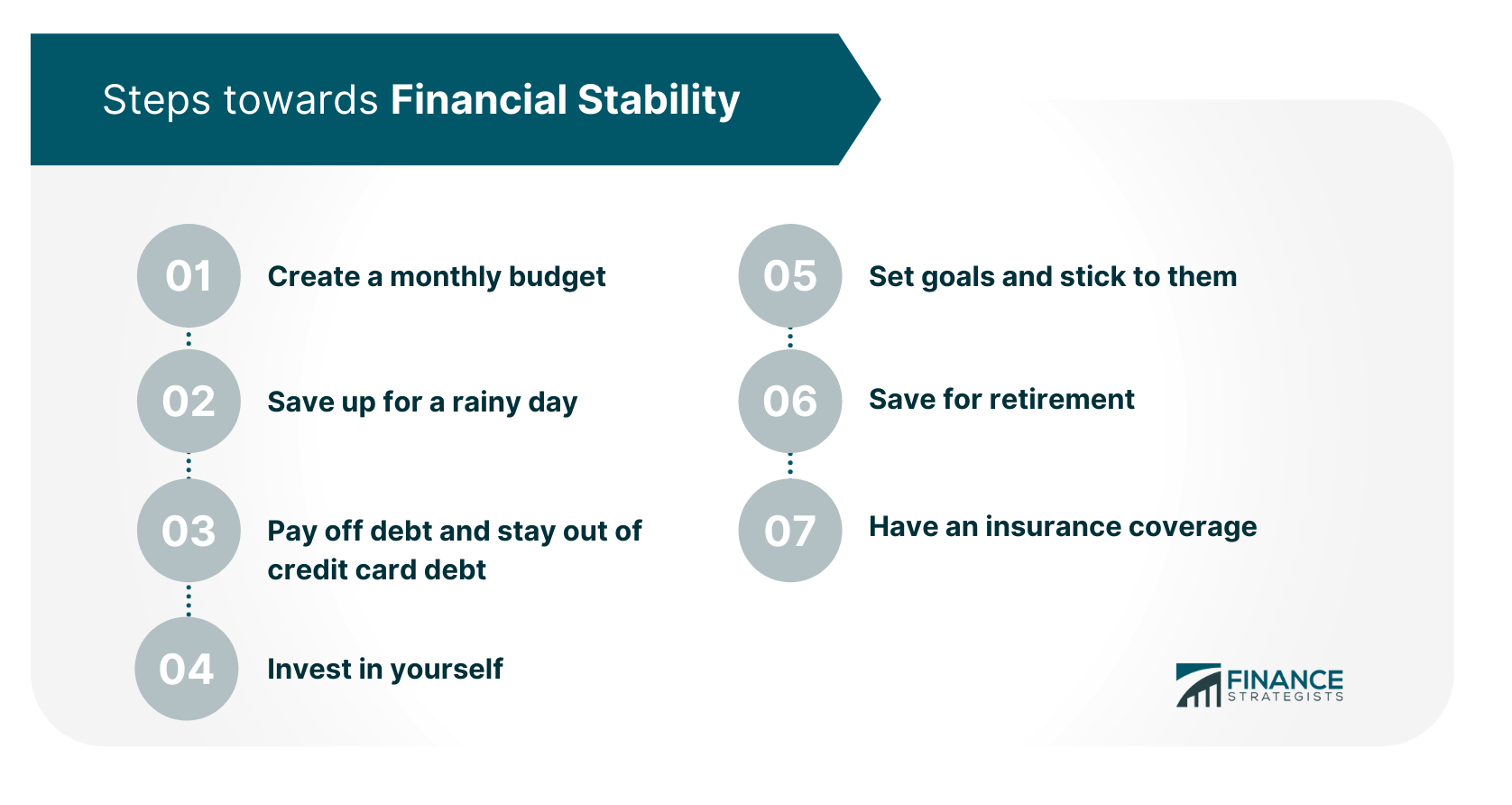

Steps Towards Financial Stability

Step 1: Create a monthly budget.

Step 2: Save up for a rainy day.

Step 3: Pay off debt and stay out of credit card debt.

Step 4: Invest in yourself.

Step 5: Set goals and stick to them.

Step 6: Save for retirement.

Step 7: Have an insurance coverage.

The Bottom Line

Financial Stability FAQs

Financial stability is when your income and expenses are in balance. Financial stability allows you to live a comfortable life without worrying about money so much. Financial stability also means having enough saved up for an emergency fund, paying off debt, and investing in yourself through learning new skills or taking classes.

An emergency fund is money that you put aside for emergencies. Financial stability requires having an emergency fund because it allows you to pay cash for small unexpected expenses like car repairs or medical bills.

Financial stability is important because it allows you to live a comfortable life without worrying about money.

Financial stability requires creating a monthly budget, saving up an emergency fund, staying out of debt, paying off your debt, having insurance, and investing in yourself. Financial stability also requires learning new skills and achieving goals.

Investing in yourself means learning new skills, going to seminars or taking classes, or reading books that will help you grow as a person.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.