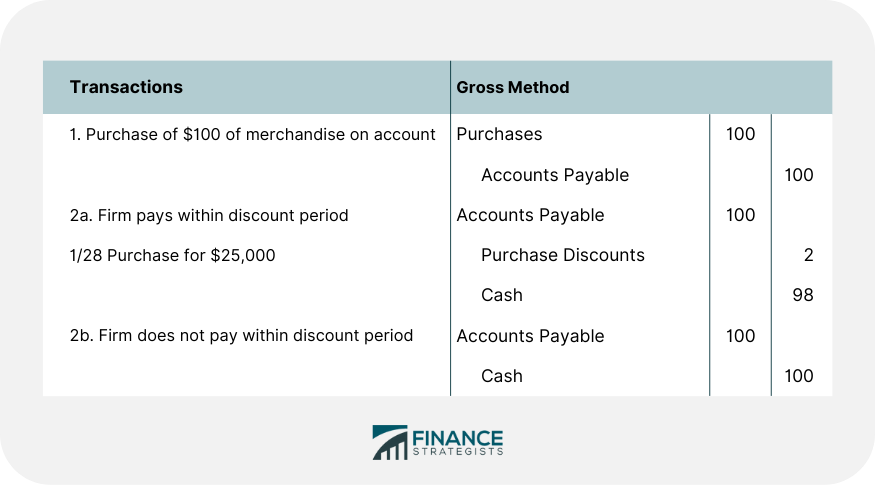

Gross method of recording purchase discounts is the method in which the purchase and the payable are recorded at the gross amount, before any discount. The gross method of recording purchase discounts records the purchase and the payable at the gross amount before any discount. If the firm takes the discount, an account titled Purchase Discounts will be credited for the amount of the discount. This account is eventually closed into Cost of Goods Sold at the time and adjusting entry is made to compute the cost of goods sold. The result is to reduce cost of goods sold by the amount of the discount taken. $100 purchase – Stated terms 2 / 10, n / 30 If the business fails to take the discount, the entry to record the payment will be straight forward. Accounts payable is debited, and Cash is credited for $100, the full invoice price. Like the gross method of recording sales discounts, the gross method of recording purchase discounts is very common. However, it also suffers from the same criticism made against recording sales at the gross amount when discounts are offered.What Is the Gross Method of Recording Purchase Discounts?

Explanation

Journal Entries to Record Purchase Discounts Under Gross Method

* This illustration assumes the uses of the periodic inventory system.

If a perpetual inventory system is used, the debit is to the Merchandise Inventory Account in all places where Purchases Account is debited. All other aspects of the entry are the same.

Gross Method of Recording Purchase Discounts FAQs

The Gross Method of Recording Purchase Discounts is an accounting principle that records discounts on purchases as a reduction in the cost of goods sold instead of reducing the purchase price by the discount amount.

Purchase discounts are recorded separately from regular purchased costs and then deducted from gross purchases. This is done to ensure that only actual payments made during a period are included in expenses for that period.

The Gross Method helps to provide accurate financial information by making sure payment amounts reflect reality, rather than showing inflated sales figures or artificially lowered expenses.

The Gross Method should be used whenever discounts are offered on purchases, such as when paying an invoice early or ordering in bulk quantities.

The Gross Method results in a lower cost of goods sold figure, which can impact several places on your financial statements including net income and inventory valuation. It also helps to ensure that expenses accurately reflect payments made during a period.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.