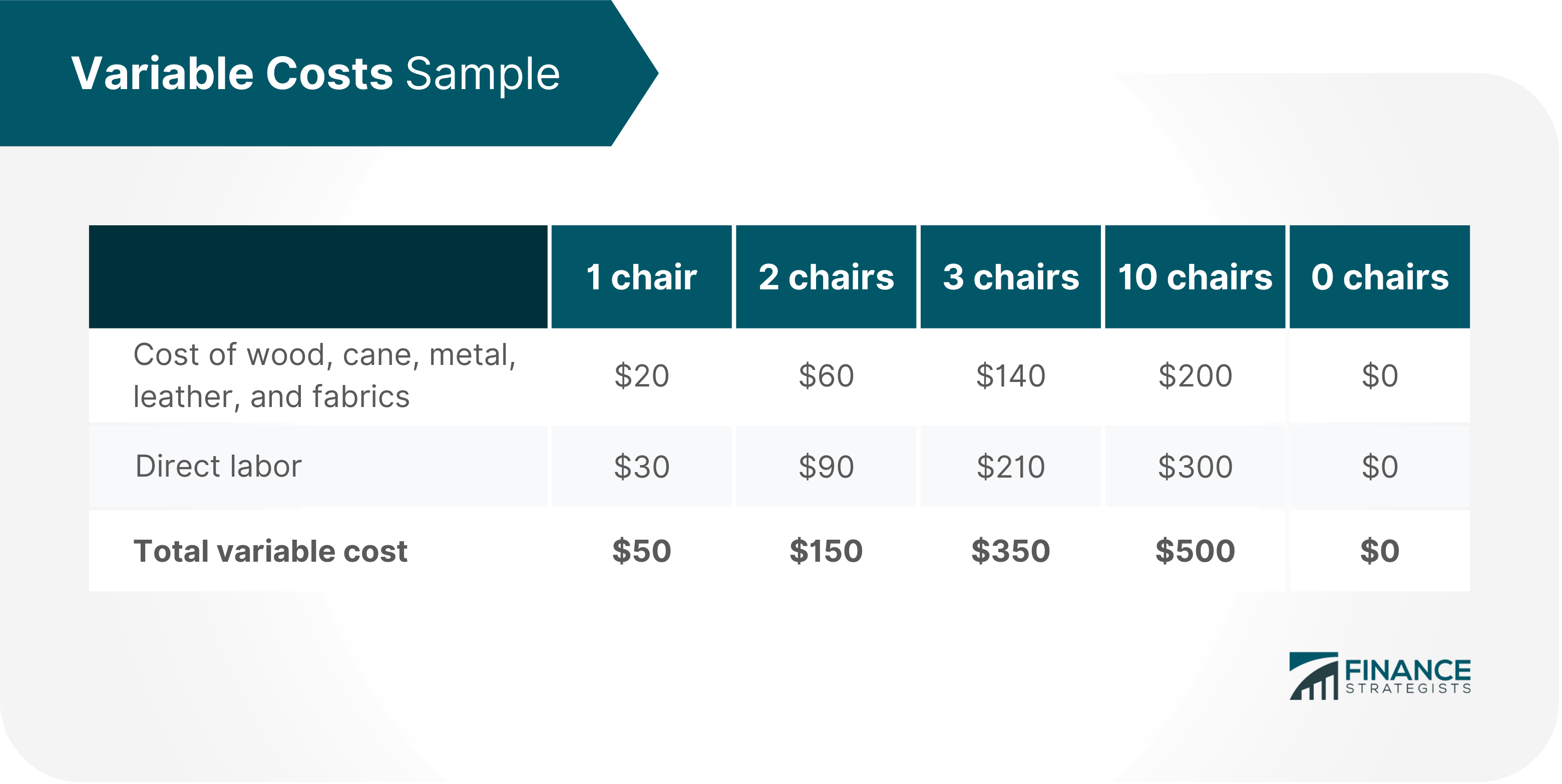

Cost allocation is a process in which businesses and individuals identify the costs incurred by activity and distribute them to appropriate accounts. This allows for better decision-making when determining how much should be spent on different business areas. There are types of costs to consider during the process of cost allocation. They include: Below shows how the variable costs change as the number of chairs made varies. As the production output of chairs increases, the bakery’s variable costs also increase. When the furniture shop does not make any chair, its variable costs drop to zero. Cost allocation is an important part of any business. The following points reflect why you should always be sure to allocate all your expenses: For example, comparing the cost of producing one product versus another can help decide which should be produced more often based on its profitability compared with other goods or services offered by a company. Taking these factors into account when allocating cost allows businesses and individuals to understand better how much money they need coming in (revenue) compared with how much they must spend (costs). This makes setting prices easier since there is an understanding of what each unit sold brings in revenue-wise. The following is an overview of how to allocate costs and some tips on what you should take into consideration when doing so. The first step is to identify all of your costs. This includes both direct and indirect expenses, as well as fixed or variable costs. Indirect costs should be allocated between departments, projects, and products based on a fair allocation plan that reflects their use in those areas. For example, suppose your company produces two products, products A and B. In that case, you will need to construct a cost-allocation plan that reflects the allocation of overhead expenses between these areas. Fixed costs are allocated among departments or projects based on how they benefit each area. For example, if Product A produces a specific product that is used for Product B, it would be appropriate to allocate the fixed costs associated with producing Product A between these two products. Variable costs are allocated among departments or projects based on how much of each cost driver they use. For example, if your company produces two products, A and B (and each product has its own direct labor cost), you would first need to determine how many units of Product A are produced for every unit of Product B sold. You can then use this information to allocate the variable costs associated with producing each product based on their respective rates. If your company uses multiple products, services, or departments that incur indirect costs, cost allocation is important in determining which method will work best for reporting profits accurately. For example, suppose you’re using a full absorption costing (FAC) system and another department within your company is using a direct labor cost system. In that case, you may need to use more than one allocation method. Cost allocation is important for both decision-making and reporting purposes. Using cost allocation, you can determine which areas of your company are over or under-spending and how changes to specific processes will affect the overall profitability of a product or department.Types of Costs

For example, a business spends $100,000 on rent every month.

Even if the company can only produce and sell 50 units of a product in one month (when they normally make and sell 100), this cost remains at $100,000 for that given time period.

For example, it costs a furniture shop $50 to make a chair—$20 for raw materials such as wood, cane, metal, leather, and fabrics, and $30 for the direct labor involved in making one chair.

For example, if a company pays for equipment rental to produce their product, this cost is considered direct because it links back to how many units have been produced.Why Is Cost Allocation Important?

Common Mistakes People Make When Allocating Costs

Process of Cost Allocation

Step One: Identify Your Costs

Step Two: Allocate Indirect Costs Between Departments or Products

Step Three: Allocate Fixed Costs Among Departments or Projects

Step Four: Allocate Variable Costs Among Departments or Projects

Step Five: Use Cost-Volume-Profit Analysis to Determine the Best Allocation Method

Step Six: Use Cost Allocation for Decision Making & Reporting

Common Cost Allocation Methods

1. Step-up/down method. This is a simple way to allocate indirect expenses, but it can result in higher costs for products and departments that use a large number of resources.

2. High/low method. This is appropriate if you have multiple cost drivers and each one has different fixed or variable rates associated with them.

It’s also helpful if your company uses more than one allocation base.3. Direct materials cost method. This is useful when the allocation base and variable rate are the same for all products.

4. Direct labor cost method. This can be used if your company produces only one product or has multiple indirect expenses that vary with direct labor costs.

However, this approach may result in some inaccuracies since it’s difficult to determine which areas of production each labor cost is associated with.5. Full Absorption Costing (FAC). This approach uses the actual costs of indirect expenses, as well as a predetermined FAC rate that can be calculated based on your company’s historical data and industry standards for determining this type of expense.

It also includes direct material and direct labor in its calculation, so you’ll have more accurate reporting of costs.6. Variable costing. This approach is appropriate when you have many variable cost allocations and your company uses a high amount of direct labor in production.

Still, it may result in inaccurate financial reports since fixed expenses aren’t allocated to products or departments based on their use.

Cost Allocation FAQs

Cost allocation is the process of assigning expenses to one or more cost objects. A cost object can be a product, project, department, business unit, or another grouping within an organization with costs associated with it.

There are many ways to allocate expenses, including the high/low method and step-up/down. There’s also a simple way called the direct materials cost method that uses an allocation base of the same value as the variable rate. Using FAC or Variable costing can provide more accurate reporting on your company’s financials.

Cost allocation allows you to determine where costs can be reduced and provides accurate reporting on company financials based on its relative performance. Allocating indirect expenses is also important for decision-making purposes. With this information, you can determine which areas of your business need improvement and how changes in production will affect overall profitability. Cost allocation can also show you which departments or products are spending too much money on indirect expenses, and which ones aren’t using enough of them. This enables you to make more informed staffing decisions in the future based on how your company’s needs change over time. Finally, cost allocation allows companies to compare their performance against similar businesses.

One of the most common mistakes is to allocate indirect expenses based on current production volume. Other issues include not performing cost allocation at all or using arbitrary rates rather than industry standards. When deciding how to allocate these types of expenses, companies should consider their company’s size and what it will cost to produce a certain amount of output.

Cost allocation can be done manually or through software. It’s important to keep detailed records of all your company’s expenses so you have accurate financial reports for decision-making purposes. If you don’t have cost records, the process of allocation can be time-consuming and difficult to determine. You may not know which department or product each expense is associated with, so your reports will lack accuracy.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.