An Intentionally Defective Grantor Trust (IDGT) is a trust in which the grantor creates specific provisions to ensure that upon their death, any assets remaining in the trust will be taxed at one or more levels prior to being distributed to beneficiaries. IDGTs are an excellent estate planning tool for individuals who want to pass on significant wealth tax-free but plan on spending down most of their assets during their lifetime. Have questions about Intentionally Defective Grantor Trusts? Click here. An IDGT can be a very effective way to reduce or avoid estate taxes, as well as gift taxes. The grantor can make direct contributions to the trust without having to worry about gift tax consequences, and any assets remaining in the trust after the grantor's death will be taxed at a lower rate than if they were distributed to beneficiaries outright. p an IDGT? The creation of an IDGT is a fairly complex process, and it is advisable to work with an experienced estate planning attorney to make sure everything is done correctly. Generally, the following steps are taken: There are several benefits to creating an IDGT, including: Assets remaining in the trust after the grantor's death will be taxed at a lower rate than if they were distributed to beneficiaries outright. The estate tax exemption amount is currently $5.45 million per individual, so an IDGT can be a very effective way to reduce or avoid estate taxes altogether. The grantor can make direct contributions to the trust without having to worry about gift tax consequences. The trustee has discretion over distributions from the trust, so they can be tailored to the needs of each beneficiary. There are a few potential drawbacks to setting up an IDGT, including: The creation of an IDGT is a complex process, and it is advisable to work with an experienced estate planning attorney to make sure everything is done correctly. There may be additional administrative costs associated with setting up and maintaining an IDGT. The grantor should take steps to ensure that the trust is administered properly and that no assets are stolen or misused. An IDGT can be a very effective estate planning tool for individuals who are willing to leave substantial wealth to charity after their death. However, the IDGT is not beneficial in all situations, and it may not make sense for individuals with smaller estates or those who expect to spend most of their money before they pass away. An IDGT is a complex estate planning tool that can be very beneficial in some situations, but it may not make sense for many individuals. Before setting up an IDGT, the grantor should work with an experienced estate planning attorney to ensure that everything is done correctly and legally. Why Would Someone Create One?

What are the Benefits of an IDGT?

Drawbacks to Creating One

Who Should Consider Setting Up an IDGT?

The Bottom Line

Intentionally Defective Grantor Trust (IDGT) FAQs

The creation of an Intentionally Defective Grantor Trust is a complex process, and it is advisable to work with an experienced estate planning attorney to ensure that everything is done correctly. Generally, the grantor must give the trustee discretionary power over distributions from the trust, disclaim ownership of any assets that are contributed to the IDGT and transfer them into a separate entity, such as a limited liability company or corporation. The assets are then transferred back into the trust.

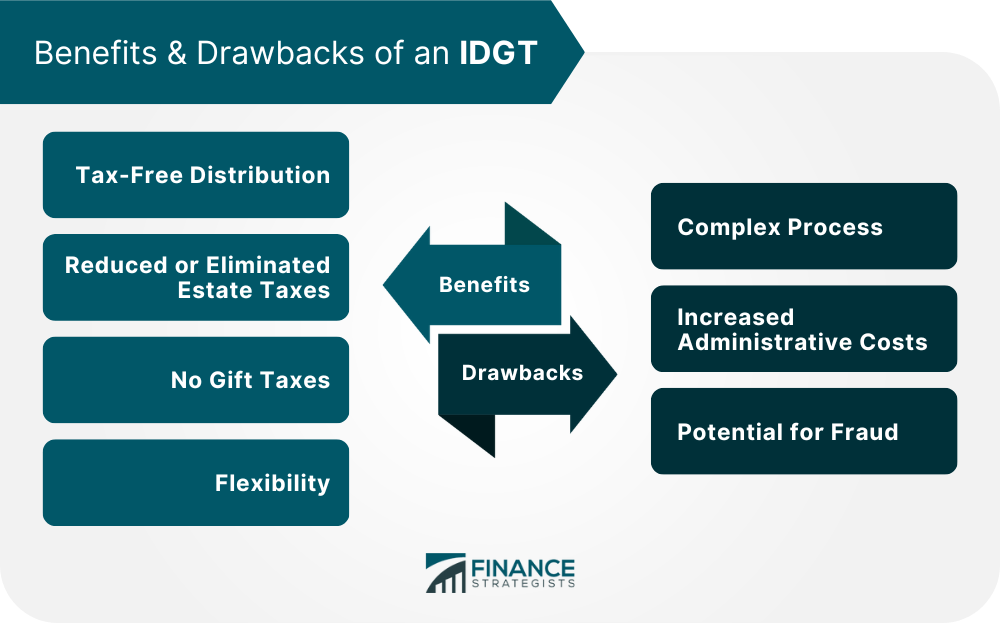

There are several benefits to creating an Intentionally Defective Grantor Trust, including reduced or eliminated estate taxes, tax-free distributions and no gift taxes. Additionally, the trustee has discretion over distributions from the trust, so they can be tailored to the needs of each beneficiary.

An Intentionally Defective Grantor Trust can be a very effective estate planning tool for individuals who are willing to leave substantial wealth to charity after their death. However, the IDGT is not beneficial in all situations, and it may not make sense for individuals with smaller estates or those who expect to spend most of their money before they pass away. Before setting up an IDGT, the grantor should work with an experienced estate planning attorney to ensure that everything is done correctly and legally.

Yes, there are a few potential drawbacks to creating Intentionally Defective Grantor Trusts, including the complex process of setting them up and maintaining them, as well as additional administrative costs. Additionally, there is a potential for fraud, so the grantor should take steps to ensure that the trust is administered properly and that no assets are misused or stolen.

Intentionally Defective Grantor Trusts are legal in the United States, but it is important to check with your estate planning attorney to ensure that everything is done correctly and legally. Additionally, there may be state-specific laws or regulations that need to be taken into consideration when setting up an Intentionally Defective Grantor Trust.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.