Investment banking and wealth management are distinct but related financial services. They both advise and guide clients to help them grow their wealth. Investment banking is specialized work focused on raising capital or handling finance-related transactions for institutional clients like governments and corporations. Investment bankers do not work with individual investors. On the other hand, wealth management helps clients manage finances to achieve long-term goals. Wealth managers work with individuals or families to provide comprehensive advice on budgeting, asset allocation, retirement and estate planning, and tax planning.

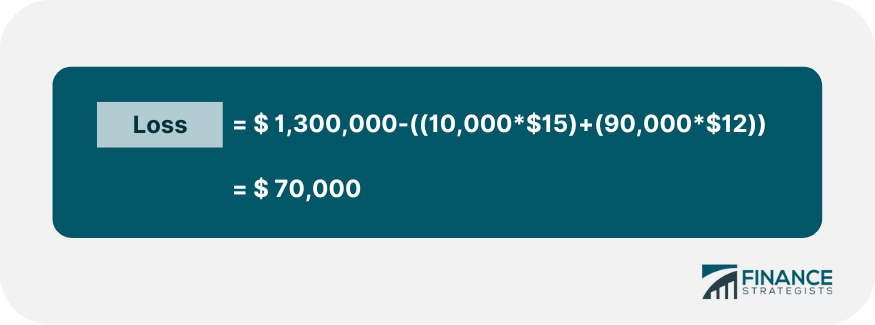

Investment banking is a financial service that creates capital for corporations, governments, and institutional investors. Investment bankers advise on investments, mergers and acquisitions (M&A), and corporate reorganizations. They underwrite new debt and equity securities for their clients, offer asset management, and help companies expand through an initial public offering (IPO). Investment bankers advise corporations on various strategies related to equity financing, derivative products, and mutual fund investing activities. They may also help governments create and manage sovereign wealth funds or give strategic advice on privatization matters. Investment banks typically receive fees, incomes, and commissions. Fees are usually charged for M&A advice, underwriting, or providing access to capital markets. Commissions and incomes are often earned when trading stocks, bonds, or derivatives on behalf of a client. Full-service investment banks provide a wide range of services, including underwriting, mergers and acquisitions, sales and trading, and equity research. Underwriting refers to providing capital to companies or governments in return for ownership of shares or bonds. When a corporation wants to go public, they need an investment bank that can offer advice on pricing and structure. For governments, raising capital typically involves selling debt to private enterprises. Investment banks act as advisors and intermediaries and help manage the sale of debt through bonds. This involves advising companies on mergers & acquisitions and divestitures. Investment banks handle negotiations between the two entities, provide analysis to determine if potential deals make sense, and structure transactions that maximize value. They provide advice on tax implications and perform due diligence. They also work with legal and accounting firms to ensure the processes are correctly carried out. This involves helping clients buy and sell securities such as stocks, bonds, options, futures, commodities, and foreign exchange in the secondary market. Investment banks monitor specific stock movements and advise when to enter or exit the market. They may execute trades directly or through brokers on their client's behalf. Investment banks may also act as principal traders in their own accounts. Investment banks analyze potential investments and advise their clients on whether they should buy, sell, or hold particular stocks. They may also provide fundamental and technical analysis, market research, industry analyses, financial forecasts, macroeconomic trends, sector outlooks, and individual company reports. Suppose Company Y makes running shoes and other athletic gear and wants to go public. Investment Banking Firm A offered company Y to manage its IPO at $12 per share. Not to be outdone, Investment Banking Firm B offered $13 each. Naturally, Company Y agreed to Firm B's terms and got paid $1.3 million for the initial 100,000 shares. After completing the paperwork, Firm B sells the shares at $15 each. Unfortunately, it could only sell 10% of the shares at that price. As a result, Firm B is forced to lower the price to $12 just to sell the remaining 90,000 shares. For the IPO deal for Company Y, it made a total of $1.23 million. Firm B overvalued the company and lost $70,000 in the process. Due to intense competition, investment banking firms can sometimes overvalue a company to land an IPO deal. As in this example, the firm incurred losses that could adversely affect its bottom line instead of earning profits. Wealth management is managing clients' financial assets to reach their goals. This includes customizing investment portfolios and providing comprehensive advice on taxes, retirement, estate, legacy planning, and philanthropic works. Unlike investment banking which offers services to corporations and governments, wealth management deals with individuals and families, typically higher net-worth investors, due to the comprehensive nature of services and minimum investment requirements. Wealth management costs depend on the type and complexity of services provided. Generally, fees are based on a percentage of assets under management (AUM). Other charges include annual retainer fees and performance-based fees. Wealth management is typically divided into two aspects and performed by relationship managers and investment professionals. They are responsible for understanding their client’s financial goals, creating personalized plans that help meet these goals, and offering advice on various topics such as taxes, estate planning, retirement planning, or philanthropic planning. They work alongside relationship managers to understand each client's specific circumstances to customize an investment portfolio. They can also help with insurance, estate, and tax planning strategies. Overall, they ensure that a client's finances meet their changing goals. These may include investment management, retirement planning, estate planning, tax planning, philanthropic planning, education planning, business planning, debt management, insurance services, and asset preservation. Investment management helps individuals manage their investments in stocks, bonds, mutual funds, and other financial instruments. It provides advice on where to invest for the best returns. It also monitors your current investments and suggests changes when necessary. Retirement planning gauges how much you will need in retirement and creates strategies to meet those goals. It often involves calculating how much money you will need to maintain your current lifestyle and investing in assets that generate income when you retire. Estate planning is arranging the management and disposal of your estate after death or incapacity. It involves understanding your current financial situation, goals, and legal concepts like wills, trusts, and taxes. It ensures that assets are distributed according to your wishes. Tax planning is anticipating and managing an individual's tax obligations. It involves working with a tax accountant to reduce taxes owed by taking advantage of available deductions and credits and timing income and expenses for maximum tax benefit. This involves structuring a charitable giving strategy to maximize the tax advantages and long-term impact of the giving. Philanthropic planning can also involve advising clients interested in creating their foundations or other charitable entities. Education planning includes saving money, maximizing aid and scholarships, and leveraging tax incentives. Education planning also involves proper investment diversification to manage risk and ensure that you have enough funds for your child's education. This process helps businesses define objectives and develop strategies to achieve them. It includes analyzing internal resources, developing short- and long-term goals, researching the competition, conducting market analysis, creating financial plans, and monitoring progress. This involves creating a plan to help individuals better manage their debt through budgeting, consolidating loans, restructuring payments, and renegotiating terms with creditors. It may also include credit counseling to help individuals remove and stay out of debt. This involves working with an insurance broker to select and purchase appropriate policies to meet an individual's needs. Insurance services include auto, home, life, health, disability, liability, and long-term care. They help keep finances safe in case of untoward incidents. This focuses on preserving your capital while still allowing you to enjoy some growth. It typically involves investing in low-risk, fixed-income securities such as bonds, Treasury bills, and certificates of deposit. Strategies also include diversifying across asset classes to limit risk. A family has recently inherited a large sum of money and would like to grow their wealth over time without taking on too much risk. A relationship manager meets with the family and establishes their goals, including retirement planning and estate planning. The manager then works with investment professionals to create a customized portfolio that meets the family’s objectives while considering current market conditions. They invest in long-term certificates of deposit, fixed annuities, and life insurance. The portfolio also includes mutual funds and treasury bills. It is closely monitored over time to ensure it remains in line with the family's needs, and periodic reviews are conducted to address any concerns or life changes. The key difference between investment banking and wealth management is their respective focus. Investment banking focuses on raising capital for corporations, governments, and institutional investors, while wealth management focuses on an individual’s financial assets. Investment banking involves M&A, IPOs, trading, and market making. Wealth management includes estate, tax, philanthropy, education, business planning, debt management, insurance services, and asset preservation. Wealth management is best if you seek advice on managing investments or creating a long-term financial plan for yourself or your family. Investment banking may be the right option if you want to raise capital for a business venture or need help with complex transactions. Regardless of your choice, working with a qualified financial advisor who can provide sound guidance is essential. Be sure to ask a financial advisor the right questions, research the services and fees, and do your due diligence to make a well-informed decision.Investment Banking vs Wealth Management: Overview

What Is Investment Banking?

Investment Banking Services

Underwriting

Mergers & Acquisitions

Sales and Trading

Equity Research

Example of Investment Banking

What Is Wealth Management?

Relationship Managers

Investment Professionals

Wealth Management Services

Investment Management

Retirement Planning

Estate Planning

Tax Planning

Philanthropic Planning

Education Planning

Business Planning

Debt Management

Insurance Services

Asset Preservation

Example of Wealth Management

Investment Banking vs Wealth Management

The Bottom Line

Investment Banking vs Wealth Management FAQs

Investment banking focuses on financial services related to mergers, acquisitions, public offerings, and corporate restructuring. It works with governments, corporations, and institutional investors. Wealth management is a holistic approach to managing a client’s financial needs and objectives. It typically works with high-net-worth individuals.

Investment banks provide corporate finance and capital market activities, which involve helping companies raise funds in the stock and bond markets. They also provide financial advisory services, such as mergers and acquisitions (M&A) advice, restructuring advice, and portfolio management.

Investment banks primarily work with governments, corporations, and institutional investors. These clients typically have large financial assets and need help managing them efficiently.

Wealth management focuses on the individual’s financial needs and objectives. It typically involves detailed advice for high-net-worth individuals, such as tax planning, estate planning, retirement planning, risk management, and investments. Wealth managers also provide services such as portfolio management and asset allocation.

Wealth management typically works with high-net-worth individuals, such as business owners and executives, because of the comprehensive nature of its services. It provides financial advice tailored to their individual needs and objectives.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.