A journal is a book in which financial transactions are recorded. Because it is where transactions of a business are first recorded, it is otherwise known as the “book of original entry.” Journals can be used to track business records, monitor investments, create budgets, manage daily finances such as receipts and expenses (including profit and loss information), or any other kind of record-keeping that is done regularly. Some companies employ a computerized accounting system while others may still be using manual accounting. Either way, journals are still important in order to keep a record of all sorts of transactions. When a financial transaction happens, the bookkeeper records the transaction into the journal and a journal entry is then made. The entry will detail the date when the transaction was made, the accounts affected by the financial transaction, the corresponding amounts involved for each account affected, and a brief explanation to support the transaction. Regularly maintained journals are also essential for accounting purposes because they provide information about money coming into and going out of your company’s bank account. In double-entry bookkeeping, companies usually keep 7 different types of accounting journals. This is done in order to further organize the kind of transactions into the specific journal type where it fits. This way, it will be easier to analyze the effects of the transactions than if they were recorded in one journal. The seven types of accounting journals are: The purchase journal is where all credit purchases of merchandise or inventory are recorded. Thus, this kind of journal must not contain transactions such as the purchase of assets on credit because this should only be exclusively for merchandise or inventory. Also, merchandise or inventory purchases paid by cash should not be recorded in this journal as it is exclusively for credit purchases. This type of journal houses all returns of inventory that were originally purchased on credit. Take note that inventory returns that were originally purchased in cash cannot be entered into this journal. The cash receipts journal is where all cash receipts, which could be payments from customers for the service or product that you sell, are recorded. Sources of cash could also include, but are not limited to, debtors, income, or loans received. This is where one would record items such as customer payments and bank deposits. The cash disbursements journal is where all payments to creditors using cash are noted down. This includes payments for a variety of expenses such as payroll, suppliers’ bills, interest paid on a loan, or mortgage payment. The cash disbursements journal is also otherwise known as the “cash payments journal.” Note that some companies may have specific journals for each type of expense category they have in order to track costs more effectively. This journal records all sales of goods on credit. Sales to customers who pay in cash should not be recorded here, but instead entered in the Cash Receipts Journal. This journal is where all credit returns of merchandise or inventory are recorded. Also, if the items were originally purchased in cash and returned in credit, they should not be entered here but instead entered in the Purchase Returns Journal. The general journal is where one will record all the journal entries that do not fit into any of the six types mentioned above. An example of a financial transaction that could be recorded here is the purchase of an asset on credit. This is also where we list information about credits and debits so as to form a complete accounting system for recording transactions in double-entry bookkeeping. A simple journal entry in a general journal will look like this: Both journals and ledgers are useful tools in bookkeeping but each of these serves different purposes and uses. As has been already mentioned, a journal is where a financial transaction is first recorded. A ledger, on the other hand, is where the results of the transactions are kept permanently. During preparation, all financial transactions will have to be recorded first in the journal before they are translated into the ledger. Here are some points to remember to differentiate a journal from a ledger: The journal is a very important tool in accounting. Although it may seem quite simple, this record-keeping tool can be a powerful asset for your business. Journals are the books used by companies and businesses in order to maintain records of financial transactions. They are important sources of data that can be analyzed to gain valuable financial insights on business operations, performance, and cash flow status. Just keep in mind these things and always remember to use journals properly so you don’t have to face any problems while doing your books.How Is a Journal Used?

Types of Journals

Purchase Journal

Purchase Returns Journal

Cash Receipts Journal

Cash Disbursements Journal

Sales Journal

Sales Returns Journal

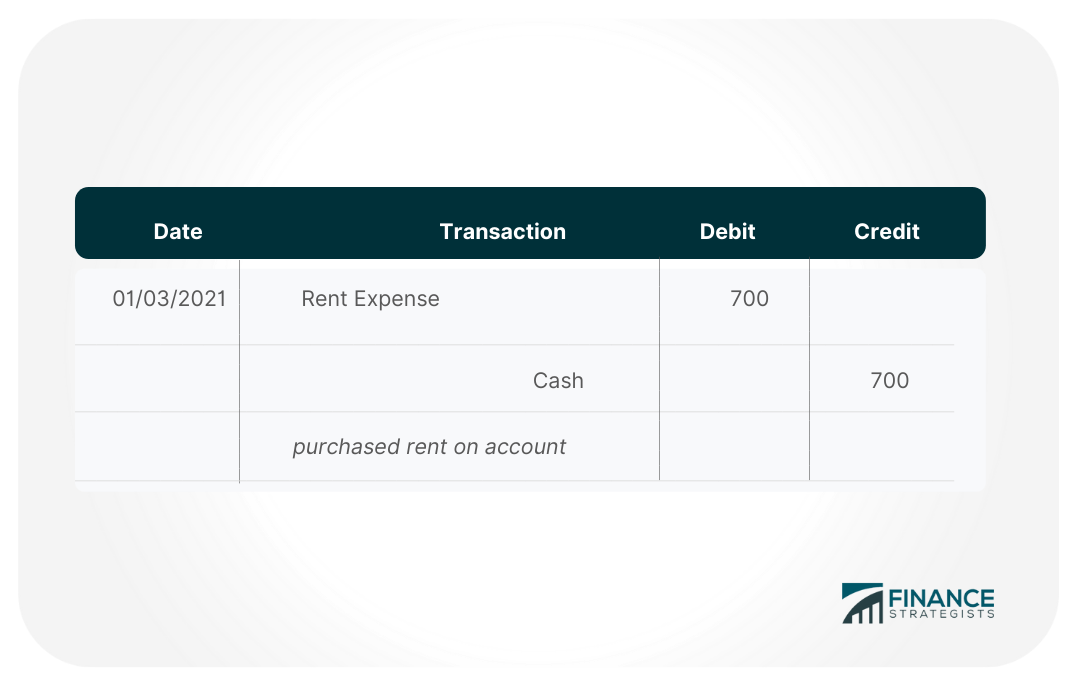

General Journal

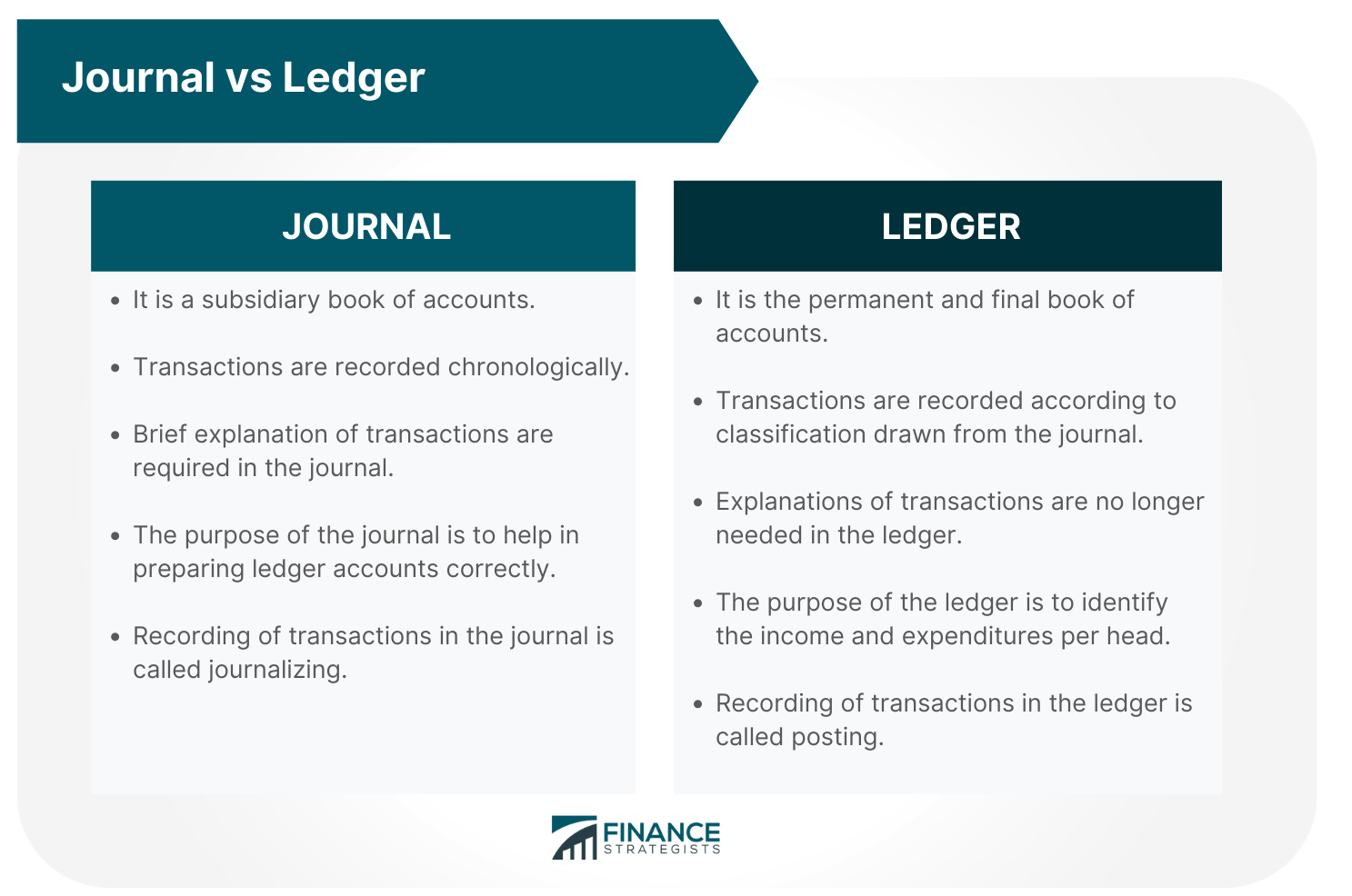

Journal vs Ledger

Final Thoughts

Journal FAQs

There are seven different types of journals: purchase, purchase returns, cash receipts, cash disbursements, sales, sales returns, and general.

The general journal is where all information not included in an individual transaction will be recorded. This includes things like payments for rent or interest on loans.

You can choose whether you want to use a journal or not. It all depends on what you and your company find most convenient and useful for your accounting dealings. You may also opt to work with both, depending on how detailed your financial records need to be.

When a financial transaction happens, the bookkeeper records the transaction in the journal and a journal entry is then made. The entry will detail the date when the transaction was made, the accounts affected by the financial transaction, the corresponding amounts involved for each account affected, and a brief explanation to support the transaction.

The journal is important because it is the first point of recording anything to do with your business. It will help you keep track of all these transactions and know what kind of financial position your business is in. You can also use journals to monitor certain things like cash flow, inventory quantities, and accounts receivable or payable status.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.