Personal finance is the process of planning and managing your personal financial affairs. It involves all aspects of your financial life, including saving, investing, spending, banking, insurance, mortgages, investments, retirement, tax, and estate planning. Understanding the concept is essential because it helps you make smart decisions with your money. It gives you a roadmap to financial security and freedom. Without a solid understanding of personal finance, you may find yourself making poor choices with your money that can have long-term consequences. For example, you may end up carrying too much debt, or not saving enough for retirement. Ultimately, personal finance helps you prepare for life's unexpected events, such as job loss, illness, or disability. Have questions about Personal Finance? Click here. In the following sections, we will discuss the different aspects of personal finance in detail and provide some tips on how to manage your finances effectively. When it comes to personal finance, there is no one-size-fits-all solution. The best way to manage your finances depends on your individual circumstances. However, we have listed here some general tips that can help you make smart financial decisions: Use your newfound savings to enroll in an automatic monthly deposit plan through your bank or credit union. Having this regularly deposited will help you save down the line, and you will be glad you did it when looking back five, ten, or even twenty years from now. Invest your cash dollar cost averaging into well-established, low-cost mutual funds or equities with a good track record and bargain fees. Dollar-cost averaging is the practice of investing an identical amount of money each week, two weeks, or one month. The goal of dollar cost averaging is to smooth out stock market fluctuations by spreading out the peaks and troughs throughout time. Mutual funds are investment vehicles that raise money from investors and invest it in the stock or bond markets. The rates of return for a given mutual fund may be found by reading the prospectus. Prospectuses are documents that detail the investments held by a mutual fund. They also reveal what rates of returns the fund have generated over time (one year, two years, five years, ten years, and even the life of the fund). Compare those returns to other mutual funds offered by your employer to diversify your assets among the most successful funds or to diversify your assets among mutual funds that best satisfy your needs. If your employer offers a 401(k) or 403(b) with mutual funds, enroll in it as soon as possible. Your employer will match your contribution dollar for dollar up to a certain percentage of gross income. Invest automatically during each bi-weekly pay period. Many employer-sponsored retirement programs match dollar-for-dollar what you save and invest, up to 6% of gross income in many cases. For example, if your gross pay is $2,000 a month, you may put away up to 6% (or $120) each pay period, and your firm will match the amount. The prospectus for the mutual funds managed by the company managing them will generally include a list of options. Examine each mutual fund's prospectus to determine which ones offer the most significant returns and expense ratios. There are three types of mutual funds: growth funds, income funds, and hybrid funds. The best option for you depends on your individual needs and goals. A growth fund usually only invests in stocks. If you want to invest in a growth fund, it is recommended that you do so for a lengthy time frame, such as five years or more. In the long run, growth funds will generate greater returns than income and hybrid funds; however, they are considered riskier and unstable in the short term. An income fund invests in bonds or high-yielding, dividend-paying stocks. Income funds are less risky than growth and hybrid investments. Once a month or every three months (for example, every three months), income funds typically pay out interest and/or dividends; as a result, they are generally more stable than growth and hybrid funds but have less potential for price appreciation. Hybrid funds are mutual funds that have the characteristics of both growth and income funds. These funds are mostly less volatile than growth funds and more volatile than income funds. If you like to do stock research analysis, buy an investment research manual called the Value Line Investment Survey manual. The Value Line Investment Survey manual is published by Value Line, Inc., based out of New York City, and tracks the common stocks of well over two-thousand companies. The Value Line Survey manual contains financial information dating back as many as fifteen years. It features stock charts, financial ratios (such as earnings per share, price-to-earnings ratios, and operating margins), dividend yields and payouts, debt ratios, and analyst opinions about the company. The survey also groups companies by industry (banks, oil companies, internet businesses, etc.), making it easy to find specific types of companies. You can purchase the Value Line Investment Survey manual at valueline.com. A membership may cost anywhere from a few hundred to several hundred dollars annually. Learn about the power of compounding money. Your money may grow substantially depending on the rate of return and time (e.g., years) you have to invest. For example, if you start today with $10,000 and invest it at a 5% yearly return, in twenty years, you will have around $25,000.00 *These examples assume no additional funds or investment, and no taxes are included. What if you were to add $500.00 a month or $1,000.00 monthly on top of the original $10,000? If you start with $10,000 and invest an additional $500 every month for 20 years, your total will be around $89,000. If you add $1,000 to the scenario above, some possible outcomes are as follows. Please keep in mind that these scenarios do not take into consideration any extra money or capital, and taxes are also not included. Making money without putting in active work may sound like a myth, but compounding can make it your reality. Many states require automobile insurance coverage. To protect yourself and others, you must have a plan. Below are the types of coverages available on a typical automobile policy plan: Depending on your living situation, you should have either renters or homeowners policy in addition to auto insurance. Some of the coverages under a homeowners insurance policy are as follows: Dwelling coverage for a condo includes the part of the building you are responsible for, sometimes called building items or additions and alterations. This can consist of materials used for construction like lumber and drywall or interior finishes like electrical outlets or plumbing fixtures. The limit on this coverage reflects the amount you would receive to replace these items if a covered event destroyed your unit. Your personal properties are everything you own, including your furniture and other household items. If you can't live in your home because of a covered loss, this insurance will help pay for the increased living expenses you need to live comfortably. The insurance company will pay for as long as it takes to repair or replace the damage or until you find a new home if you have to relocate permanently. Personal Liability will protect you if somebody files a lawsuit against you or anyone else covered under the policy for any accidental bodily injury or property damage. Your coverage limit should be high enough to protect your personal assets, including your home. For example: if somebody sues you after they slip and fall on your property, this coverage will help pay for legal fees and damages. Medical expenses for people other than you or your family are covered under this protection plan. This includes costs for those injured either on your premises or as a result of your actions away from home. Please refer to your policy documents for more information. Floods, surface water, waves, tidal water, overflowing bodies of water, and spray from any of these are all considered floods. Your policy will start to pay for losses that are not from earthquakes if the amount of your loss exceeds this limit. For complete details, please refer to your policy documents. For your policy to begin paying, the amount of damage caused by wind and hail must exceed this figure. For example, if your home has a $1,000 deductible and hail causes $3,000 worth of damage, your policy would pay $2,000, and you would be responsible for the first $1,000. If your deductible is a percentage, it is calculated based on your dwelling limit and varies as this limit fluctuates. If you have numerous assets, buying an umbrella insurance policy would be beneficial. This is also known as additional liability insurance. A disability is an illness or injury, physical or mental, that prevents you from carrying out your usual and regular employment. Elective surgery, pregnancy, delivery, and related medical situations are all examples of disabilities. Work-related disabilities are usually covered under worker's compensation laws. Still, disability insurance benefits can also be paid for work-related illnesses or injuries in specific situations that are outlined by law. In a life insurance policy, the insurer agrees to pay a designated beneficiary a sum of money in exchange for premiums paid by the policyholder. The death of the insured person triggers this payment. Personal Finance is the financial planning that an individual or a family unit undertakes to earn, save and spend money wisely. There are a number of key concepts in personal finance that can help you make sound financial decisions. These include setting financial goals, budgeting, investing, saving, retirement planning, and insurance planning. Always remember these things when diving into personal finance, first, make sure you have an emergency fund to cover unexpected expenses. Second, invest money wisely to grow your wealth over time. Third, make sure you have adequate insurance coverage to protect yourself and your family in case of an accident or illness. Lastly, be mindful of your spending habits and try to live within your means. Personal finance is not about making money – it’s about managing the money you have to get the most out of it. There is no one-size-fits-all solution in managing your money, what works for one person may not work for another. The best way to approach personal finance is to take a holistic and individualized approach. Consider your unique circumstances, goals and risk tolerance when making financial decisions. If you are not sure where to start, seek out the advice of a financial planner or advisor. A professional can help you create a personalized financial plan that will put you on the path to financial success.A Quick Guide to Take Good Care of Your Money

Tips for Personal Finance

The amount of money you make minus the amount of money you spend equals your profit.Investing

401(k) and 403(b) Plans

Different Types of Mutual Funds

Conducting Research on Stocks

The Money-Compounding Powers

The Powers of Compounding Money Part Two

Insurance

Insurance for Automobiles

Homeowners and Renter's Insurance Policy

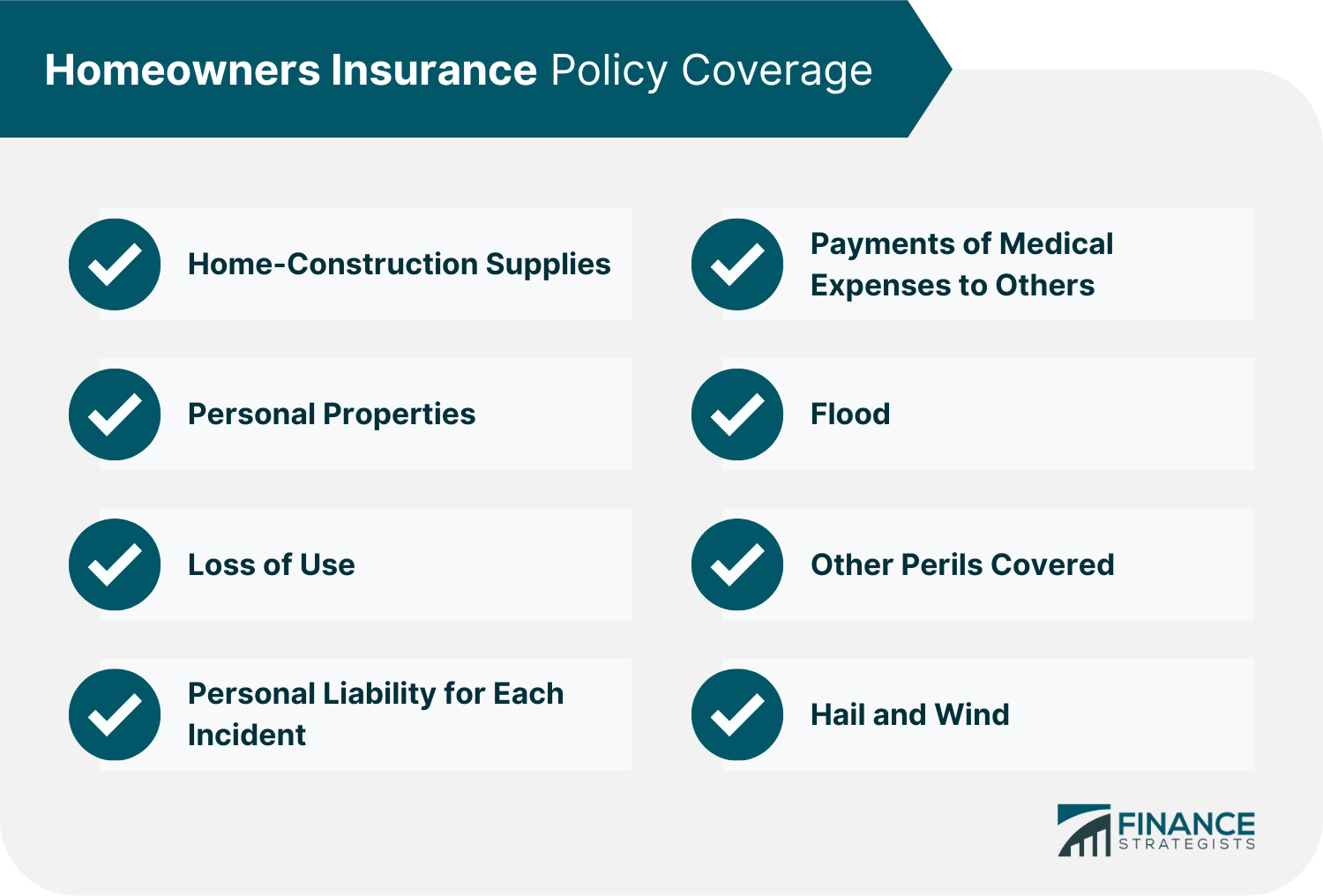

Home—Construction Supplies

Personal Properties

Loss of Use

Personal Liability for Each Incident

Payments of Medical Expenses to Others

Flood

Other Perils Covered

Hail and Wind

These Are the Exceptions

Umbrella Insurance

Disability Insurance

Life Insurance

The Bottom Line

Personal Finance FAQs

Personal finance is the financial planning that an individual or a family unit undertakes to earn, save and spend money wisely. It involves all aspects of financial decision-making, from budgeting and investing to saving for retirement and insurance planning. Personal finance is about making your money work for you – in other words, getting the most out of your money.

Personal finance is important because it gives you the tools to make informed financial decisions. It can help you budget your money, save for retirement, pay for unexpected expenses and more.

Some key concepts in personal finance include setting financial goals, budgeting, investing, saving, retirement planning, and insurance planning.

Insurance is a contract in which an insurer agrees to pay a designated beneficiary a sum of money in exchange for premiums paid by the policyholder. The death of the insured person triggers this payment.

Compounding refers to the process of earning interest on both the original investment and any previous interest earned. This allows your money to grow at an accelerated rate over time.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.