A robo-advisor is an automated online investment service that provides personalized portfolio management advice at a fraction of the price of traditional financial advisors. It uses a financial algorithm to assist individuals in making better investing decisions. Similarly, it provides them with tailored financial advice based on their goals, risk tolerance, and other personal factors. Compared to traditional advisors, robo-advisors are more cost-effective in providing personalized advice with little to minimal need for any interaction with a human financial advisor. Robo-advisors must register with the U.S. Securities and Exchange Commission (SEC) and are subject to the same securities laws and regulations as traditional broker-dealers. During the financial crisis of 2008, robo-advisors were first introduced to the market. Jon Stein launched Betterment and opened the door for robo-advisors to enter the market. Financial managers initially used them for their existing clients. Still, it was made available to the general public due to the high demand for a cost-effective alternative to asset management. Robo-advisors have since become a popular alternative to traditional financial advisors. They quickly gained traction in the market by providing low-cost portfolio management options. Since then, more and more robo-advisors have joined in filling out a large portion of the available services that offer investing advice with little to no human interaction. New clients who sign up for robo-advisor services begin by providing basic details about their financial objectives through an online questionnaire. Questions may include items on their risk tolerance, financial timeline and goals, income, liabilities, savings, and current investments. With the information gathered, the robo-advisor will generate the investor's profile and use an algorithm to predict the best portfolio allocation the investor should make. The robo-advisor will regularly monitor and rebalance the portfolio of investments based on market volatility and changes in the investor's objectives and risk tolerance. Through artificial intelligence technology, the robo-advisor analyzes data from the individual's financial transactions to understand the pattern of their financial behavior. Aside from that, it also analyzes investment, bank, and credit card transactions, allowing robo-advisors to develop a personalized portfolio that caters to their investment goals. Robo-advisors are subject to the same securities rules and regulations as traditional broker-dealers. They must register with the U.S. SEC. Most robo-advisors are members of the Financial Industry Regulatory Authority (FINRA), where investors can use the site's BrokerCheck to research the robo-advisor's credibility. Government protocols and standards must be regularly followed and observed to protect investors from fraud and provide higher accountability for robo-advisors. The popularity of robo-advisors is due to their many benefits: Fees are considerably lower because a computer-driven algorithm offers services. Clients can focus their money on their actual investments rather than paying fees to their portfolio manager every time they make a transaction. There is no need to meet in person as most transactions are completed online. Clients can manage their portfolios from anywhere. Additionally, the service is accessible to anyone because only a minimal account balance is required to start investing. Robo-advisors provide a wide range of services that handle all aspects of your financial planning. Services, including retirement planning, tax-strategy plans, and portfolio rebalancing can fall under this category. The robo can manage your portfolio on a single platform, ensure you are on track to meet your investing goals, and reduce liabilities. Robo-advisors can quickly and accurately analyze data to develop a portfolio tailored to the investor's goals. Automated technology saves time and does not require much from investors, resulting in faster portfolio management, risk calculation, and decision-making. The unequal standard of robo-advisors is one of their main drawbacks aside from the others mentioned below. While some robo-advisors on the market today construct portfolios using cutting-edge AI and machine learning, the majority still employ outdated techniques. Most robo-advisors have a portfolio of pre-selected stocks. They may only provide access to some of the investments a client needs. Also, the investment options they offer are strictly dependent on the algorithm used by the robo-advisor based on the investor's profile. Robo-advisors do not provide financial advice or allow their clients to ask questions or receive guidance. Investors who want someone to talk with when making investment decisions may find this an issue. Multiple accounts might be necessary to access different investment options. Some investments may not be available with the robo-advisor's platform, so clients need to open another account. Investors who want to combine all their investments may find this inconvenient. The cost of utilizing a robo-advisor is often less than 1% of assets under management (AUM). It will depend on the robo-advisor company and the types of fee structures they offer. An average cost of 0.5% per annum is common for many robo-advisors. Clients who invest $5,000 will have to pay $25 as an annual fee. A sliding scale of fees applies to some companies with a mix of robo-management and human advisors. An individual's portfolio determines the service costs charged on a sliding scale. The higher the portfolio, the more you will pay. The lower the portfolio, the lesser you will pay. Larger accounts usually have lower fees. Additional fees might be charged if clients request human advice. There are also fees for opening and maintaining the investment account itself. Betterment is the leading company with services such as tax-loss harvesting and goal-based investing with related cost as follows: Features of this robo-advisor include automated rebalancing, wide exchange-traded funds (ETFs), and a personalized portfolio. Related costs are as follows: Offering hundreds of ETFs to allow portfolio customization, they provide access to fractional shares, automatic portfolio rebalancing, and tax-loss harvesting. Related costs are as follows: With the many options available, it is essential to know the critical differences between the different alternatives: As a digital and automated platform that provides investment advice, robo-advisors are suitable for simple investment goals at a low fee. They are efficient in tracking and monitoring investments. They offer automatic tax-loss harvesting and portfolio updating. A robo-traditional advisor is a hybrid between a human advisor and a robo-advisor. This advisor uses digital technology to create automated and customized portfolio recommendations. Still, it provides human guidance and advice for a moderate cost. Human advisors come at higher fees but work alongside investors. They typically meet with them in person to discuss complex financial goals, including retirement and estate planning. They provide detailed and comprehensive views of their client's investment portfolios. Costs are one of the most significant factors when deciding on a robo-advisor. They are an excellent alternative if you are on a tight budget and wish to invest as much as possible without incurring high costs. If your investment approach is passive and you do not need human guidance or advice, a robo-advisor might be ideal. Suppose you prefer to automate most of the process and are uncomfortable discussing your investment options with someone. In that case, this option is worth considering. If you prefer a robo-advisor, you need sufficient knowledge and understanding of the financial choices based on an algorithm and be adept at the digital tools to manage investment portfolios. A robo-advisor is an automated online investment service that uses a financial algorithm to assist individuals in making better investing decisions. Clients provide details about their goals, savings, and their risk tolerance. This information generates an algorithm that predicts the best portfolio allocation for them. Robo-advisors are beneficial because they have low fees, typically less than 1% of the AUM. They are more accessible and efficient. However, they offer limited investment options and offer no human interaction. They are regulated by the SEC to ensure guaranteed safety for customer investments. Examples of robo-advisors include Betterment, Schwab Intelligent Portfolios, and Wealthfront. A robo-advisor is suitable for those looking to invest with limited funds and simplify their investment process. It is also ideal for those who do not require human interaction.What Is a Robo-Advisor?

History of Robo-Advisors

How Does a Robo-Advisor Work?

Robo-Advisor Regulation

Benefits of Using Robo-Advisors

Low-Cost

More Accessible

Comprehensive Services

Efficient

Drawbacks of Using Robo-Advisors

Limited Investment Options

No Human-To-Human Interaction

May Require Multiple Accounts

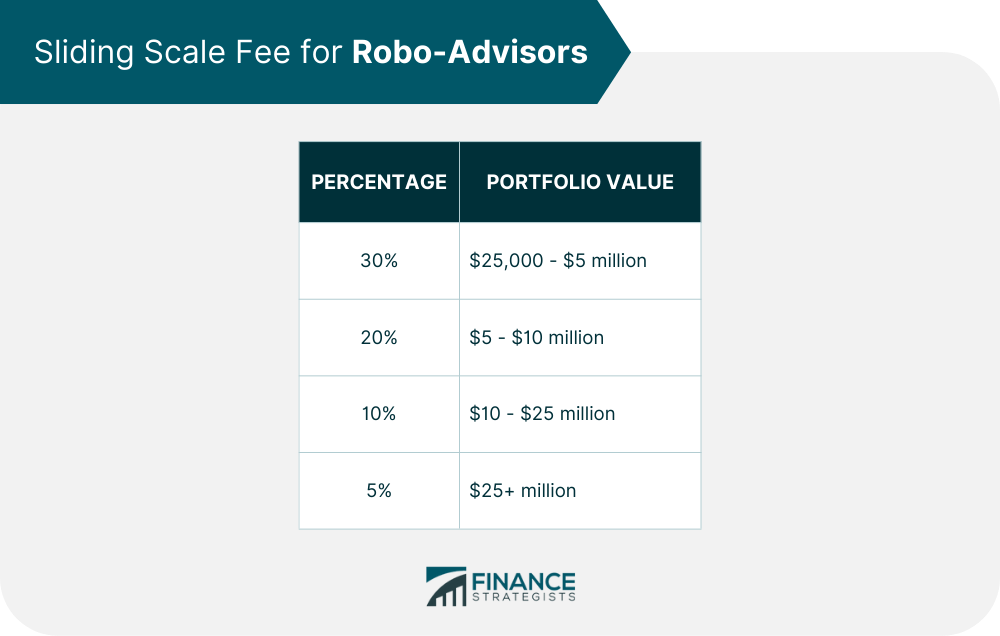

How Much Do Robo-Advisors Cost?

Examples of Robo-Advisors

Betterment

Schwab Intelligent Portfolios

Wealthfront

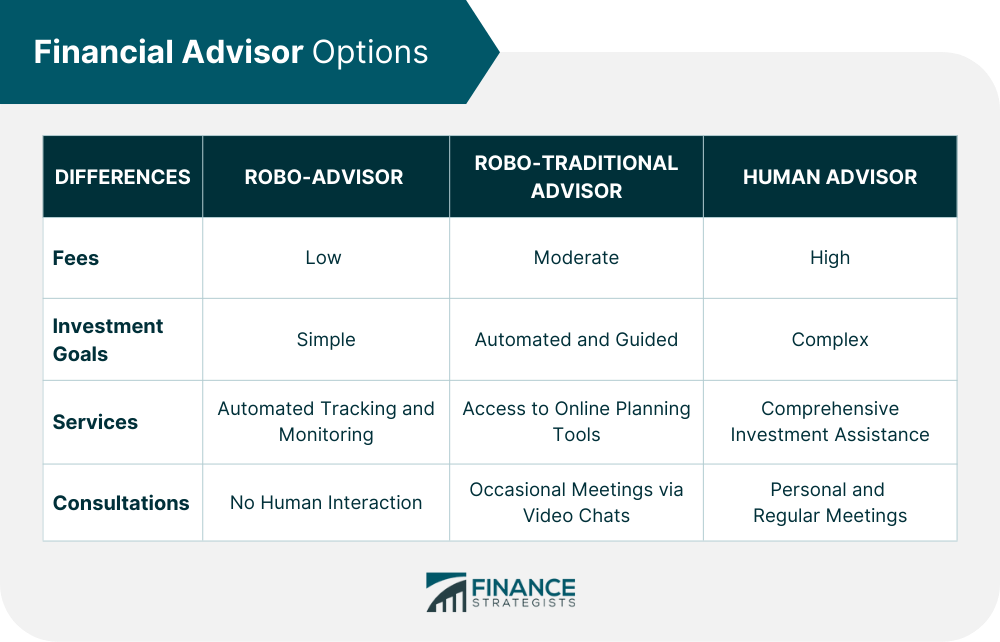

Robo-Advisors vs Robo-Traditional Advisors vs Human Advisors

Robo-Advisors

Robo-Traditional Advisors

Human Advisors

Is a Robo-Advisor Right For You?

Final Thoughts

Robo-Advisor FAQs

A Robo-advisor is an automated online service that uses a financial algorithm to assist individuals in making better investing decisions. It provides them with tailored financial advice based on their goals, risk tolerance, and other personal factors.

Robo-advisors are a great way for beginners to start investing without the help of an expensive human advisor. They provide tailored advice and have low fees, making them a good option for those looking to invest on a budget.

Robo-advisors typically charge a fee of less than 1% of the portfolio value. Still, some may offer discounts for larger deposits or have no fees.

Robo-advisors are an efficient and low-cost way to invest. They are accessible to investors with little to invest, have round-the-clock customer service, and are available anywhere as long as the investor has an internet connection.

Some popular robo-advisors include Betterment, Schwab Intelligent Portfolios and Wealthfront.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.