Sales returns are a reduction in the actual sales which occurs when a customer, for whatever reason, returns the item for a cash refund or a credit to his/her account. The reason for a sales return is usually because of a product defect or a service failure. Sales returns can be thought of as reductions in sales, but they do not involve any cash outlay by the company. Sales returns are an important part of the sales process because it allows a company to continuously provide high-quality goods and services to their customers. Returning items, in a way, also helps in building good relationships with the customers, which is important for maintaining repeat business and for increasing new business. One of the most common reasons for product returns is when customers find that the item they are receiving does not match the product description.Types of Sales Returns

1) Cash-Refund Sales Returns

This includes refunds given to customers who return their items and receive cash as a refund.2) Credit-Memo Sales Returns

This involves the customer returning the item and in turn, will receive a credit memo for future purchases.3) Store Credits

These are issued by retailers where they give discounts on certain items due to returned items.Accounting Treatment for Sales Returns

Generally, a sale is recognized when the transaction occurs, whereas a return is not recognized until the product has been returned to the company. Sample Illustration of Sales Returns

Company ABC, Inc. has sales in the amount of $10 million for a certain month. However, there were sales returns in the same period in the amount of $200,000.

Impact of Sales Returns

Sales returns are considered a normal part of doing business because it is expected that there will be some sales return in the future due to the limited availability or imperfections of certain products. How to Minimize Sales Returns

Here are some tips businesses can consider in order to minimize sales returns:Have Quality Control in Place

Getting quality control in place will ensure that products are defect-free. Also, ensure that staff members are properly trained to prevent them from making mistakes in production.Describe Product Features Accurately

Study Product Trends

It is important to keep up with the latest trends in the market to make sure you are selling products that are obsolete.

Having a keen eye for product trends can help businesses keep up with their competitors and know which products are best to sell.Give Guarantees to Customers Regarding the Quality of Goods and Services They Purchase

Keep an Open Line of Communication With Your Customers

This will ensure you receive feedback and can address any problems with your products and services before they result in returns.Final Thoughts

Sales returns are an unavoidable part of doing business because it is impossible to make every customer completely satisfied with their purchase.

Sales Returns FAQs

Sales returns are a reduction in the actual sales which occurs when a customer, for whatever reason, returns the item for a cash refund or a credit to his/her account. The reason for a sales return is usually because of a product defect or a service failure. Sales returns can be thought of as reductions in sales, but they do not involve any cash outlay by the company.

The sales returns account is classified as a contra-revenue account. It causes a deduction from the gross sales and correspondingly, causes a decrease in the net sales figure.

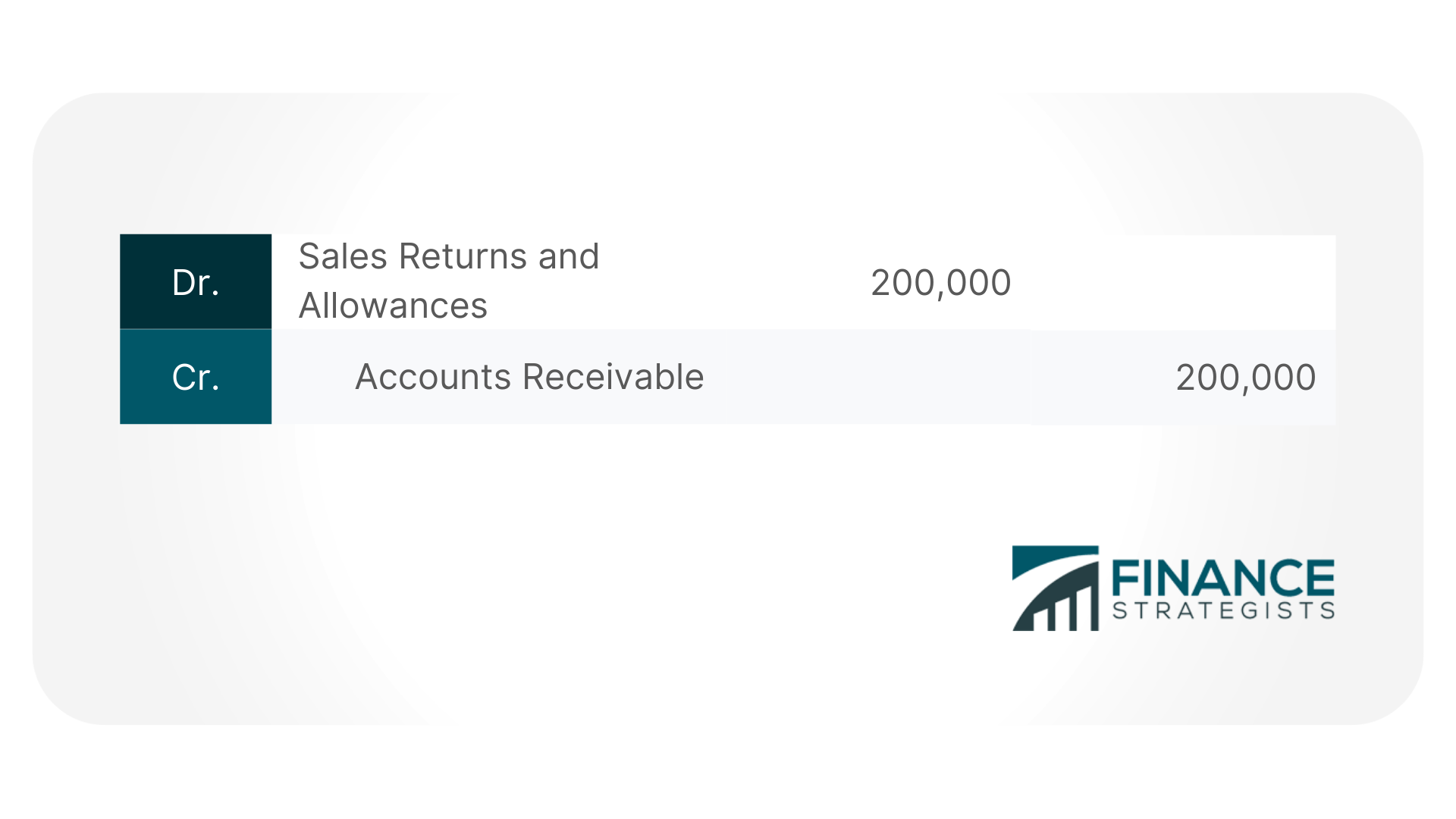

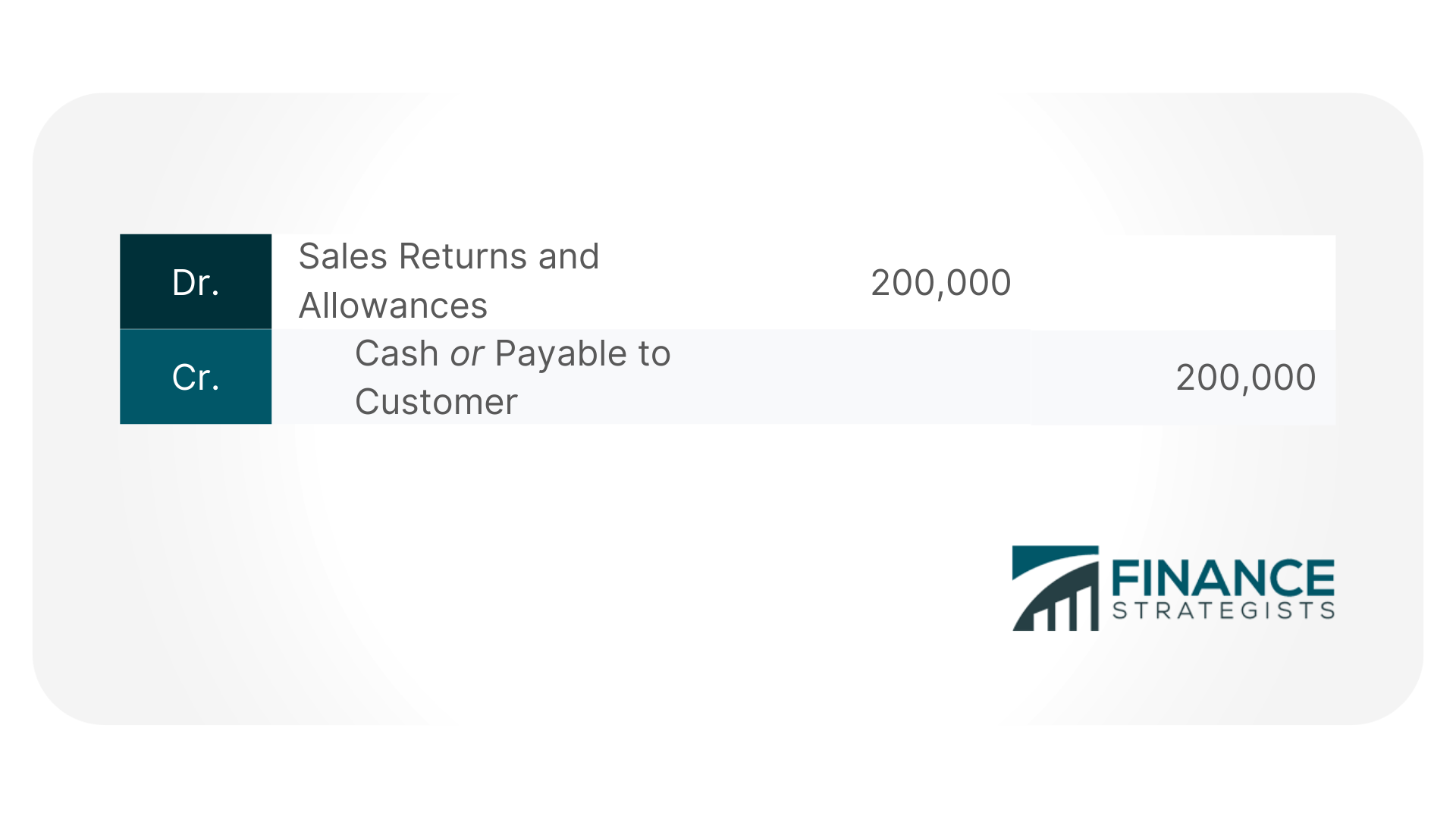

A seller will then have to record a sales return by debiting a Sales Return and Allowances account and crediting the Accounts Receivable account in a case where the sale is made on credit. The credit to the accounts receivable account will reduce the outstanding amount of accounts receivable. Conversely, if the sale was made against cash, the journal entry will require the same account to be debited but the credit will be against cash or payable to the customer account.

Sales returns are considered a normal part of doing business because it is expected that there will be some sales return in the future due to the limited availability or imperfections of certain products. Therefore, sales returns should not cause too much concern for companies. However, it should alarm the business if the sales returns and allowances account is increasing because ultimately, this will result in a decrease in the company’s revenue and income.

There are several ways to reduce sales returns. It will help businesses if they have quality control in place, especially during production because this will ensure defect-free products. It is likewise important to be able to provide accurate product descriptions to set customer expectations right. Businesses should also venture into studying the latest product trends to keep up with the demands of the market. An open line of communication between businesses and customers will also be helpful so that customer concerns are properly taken care of before a sales return happens.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.