A sole proprietorship is a business structure owned and operated by one individual. There is no actual and legal difference between the owner and the enterprise, so the owner settles personal income tax on business profits. Sole proprietorships are the simplest and most common form of ownership. They are relatively easy and inexpensive to set up and maintain. Sole proprietorships offer some of the following advantages: A sole proprietorship is the most uncomplicated type of business to form. Sole proprietorships are ideally best for people who want to start a business quickly and with minimal inconvenience. Very little paperwork or legal requirements are involved in setting up a sole proprietorship. There are no special fees for filing necessary, thus making it inexpensive. Sole proprietorship taxes are also straightforward. The revenues and costs of the business are part of the owner's tax return, and the earnings are considered personal income. It is also important to understand the following disadvantages of a sole proprietorship: The owner is responsible for all the debts and liabilities if the business fails. There is no boundary between the owner and the business, so the owner is liable for any legal problems or claims that may arise. Since the business is small, it may not have the financial resources to expand or grow. It is challenging to invite investors for a sole proprietorship. The owner is limited in terms of how much personal money can be invested in the business. While filing taxes is relatively easy for sole proprietors, taxes can be a bit expensive for them because profits are subject to self-employment taxes. Self-employed individuals pay the employee's and employer's shares of Social Security and Medicare contributions. A limited liability company (LLC) presents a business structure that integrates the principles of partnerships, corporations, and sole proprietorships. Business owners can minimize their personal liability for business debts and obligations because the LLC is a separate enterprise. Small business owners favor LLCs because they offer the same limited liability protection as corporations but with fewer rules and regulations. Some of the benefits of LLCs are listed below. LLC owners are not liable for debts and obligations incurred by the business. This protection applies even if the business is unable to pay its debts. The personal assets of LLC owners, such as their homes and cars, are safeguarded from creditors. LLC revenue is often distributed directly to the owner, recorded on the owner's tax return, and taxed at the owner's personal rate. This eliminates the need for firms to pay double taxation. An LLC may often attract equity investors and get a company financing more easily. Furthermore, there is no requirement for sole owners to file a "doing business as" or D.B.A. notice with the state if they conduct business under a name other than the owner's first and last names. Let us also consider the disadvantages of establishing LLCs. Forming an LLC might be more expensive than setting up a sole proprietorship or partnership. This is because LLCs are required to file more paperwork with the state and may be subject to additional filing fees. Additionally, LLCs may be required to publish notices in local newspapers announcing their formation. Also, if they opt to be taxed as corporations, LLCs must submit separate tax returns from the owner. This increases the difficulty and cost of filing. Furthermore, the liability protection provided by an LLC is not absolute. A single-member LLC may be treated as a lone owner if a creditor successfully lifts the corporate veil. The owner can thus be held personally accountable for the company's obligations. Now that we have looked at the advantages and disadvantages of sole proprietorships and LLCs, let us compare these business structures based on how they are set up, their costs, management structure, operations, tax implications, liabilities, and compliance. Deciding whether to have sole proprietorship or LLC depends on the business needs, business goals and objectives, the amount of money available to be invested, the level of liability protection required, and the amount of paperwork and compliance the owner is comfortable with. Generally, business owners try out sole proprietorship first due to its convenience and freedom from cost burdens. When the business starts to grow, the owner might consider LLC for its liability protection features and tax flexibility that allows for saving more money. The following are steps for businesses that prefer to grow and convert from a sole proprietorship to LLC. Verify that the business name is available in the state where the articles of organization will be filed. Make sure that it does not infringe any trademark. Include details of the name and address of the LLC, name and address of the owners, description of the business, name and address of registered agents, and date of application on the articles of organization. An operating agreement indicates the rules of ownership and the obligations and rights of the members. A new EIN is needed for the LLC and can be obtained by filing Form SS-4. For better protection, reporting, and documentation, personal and business assets must now be separate. Updating licenses or applying for new permits might be required depending on the industry or laws by the state. There are several key differences between sole proprietorships and LLCs. These include the formation process, management structure, tax implications, and liability protection. Sole proprietorships are typically easier to set up and manage, but they offer no protection for the owner's personal assets if the business faces legal action. LLCs offer liability protection and tax benefits but are more expensive to set up and manage. Business owners should choose the business structure that best suits their needs. An LLC might be the best choice if liability protection is a priority. If convenience and low costs are a priority, then a sole proprietorship might be the best choice.What Is a Sole Proprietorship?

Advantages of a Sole Proprietorship

Disadvantages of a Sole Proprietorship

What Is an LLC?

Advantages of an LLC

Disadvantages of an LLC

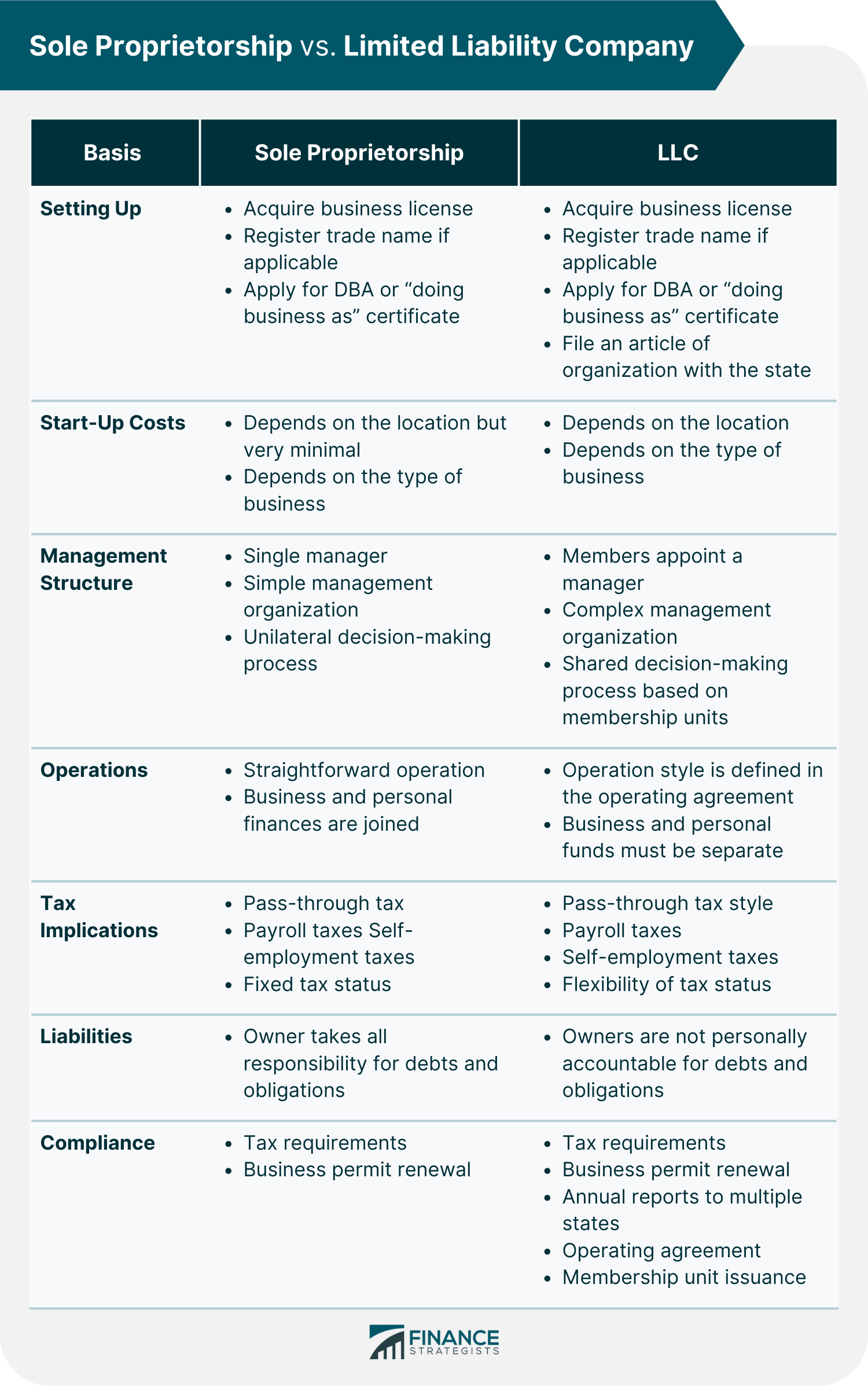

Sole Proprietorship vs LLC: Key Differences

Sole Proprietorship or LLC: Which One Should I Choose?

Shifting From Sole Proprietorship to LLC

Step 1: Validate Business Name

Step 2: File Articles of Organization

Step 3: Draft an LLC Operating Agreement

Step 4: Obtain an EIN

Step 5: Create a New Bank Account

Step 6: Acquire Licenses and Permits

Final Thoughts

Sole Proprietorship vs LLC FAQs

The ultimate choice depends on specific needs, objectives, goals, and available resources. Since sole proprietorship has little paperwork and is inexpensive to initiate, it is common for new business owners to test the waters with this business structure.

LLC means limited liability company, a business structure that offers its owners protection from personal liability for the financial obligations and debts of the business.

Yes, sole proprietorships can be converted to LLCs. This can be done by filing the necessary paperwork and articles of organization, changing the business registration, and updating permits. The owner will also need to open separate bank accounts and obtain an Employer Identification Number from the IRS.

Business owners need to file articles of organization with the state and pay associated fees, write an operating agreement, obtain necessary licenses or permits, open bank accounts, obtain an Employer Identification Number and announce their LLC.

Both sole proprietorship and LLCs have their pros and cons. A sole proprietorship may be better if convenience and low fees are preferred. If liability protection is important, an LLC may be the better option.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.