A sole proprietorship is a business that is owned and operated by an individual. The owner is responsible for all aspects of the business, including liabilities and debts. A sole proprietor can use any name for their business as long as it is not being used by another business in the same area. The initial stages of every business are just an idea in someone’s mind. They may choose to involve others to help turn their vision into a reality, or they may try and make a profit from the idea themselves. The most common type of business is a sole proprietorship, where only one person owns the company. The word “sole” is sometimes used to designate a single item, it is most often defined as “lone” and “single.” It is a kind of business that is only available to one person, just like the phrase “Sole Proprietorship” implies. It is basically a company formed and run by one guy. Most small grocery stores, car repair businesses, carpentry firms, restaurants, and barbershops are sole proprietorships. A sole proprietor is someone who creates and runs a business by themselves; they are the only business administrator. It has already been established that sole proprietorship is the most frequent and oldest form of business in the United States and worldwide. It is, without a doubt, not devoid of benefits. The following are some of the advantages of operating as a single proprietorship. Compared to proprietorships, other business entities require a much longer and more complex legal document for incorporation. The paperwork required by the government before a sole proprietor can set up his business is easy and straightforward. While the process of setting up a sole proprietorship is not easy, it is much simpler than that of other businesses. Nowadays, it is common for people to have more than one job or even own small side companies that they have not registered. The law does not prevent anyone from starting a sole proprietorship without registration, which gives those who can't pay incorporation fees the chance to start a business without any complex processes. This is a benefit since sole proprietorships let entrepreneurs do exactly as they want in regard to realizing their ideas and company goals. Because the decision-making process in other forms of enterprises necessitates the agreement of entrepreneurs, investors, and board members with interest in the firm and, in most cases, the founder's opinion, founders have less control over these businesses than they would if they started or founded them. A sole proprietorship is a type of business in which the owner assumes all managerial and financial responsibilities. The owner is responsible for everything regarding the company, including its management and finance. The firm's owner determines the pricing of his goods, exercises complete control over the production process in his company, and decides how much to invest in it and when to utilize the funds. The owner of a sole proprietorship is responsible for determining prices. Although the government regulates sole proprietorships like any other business, their regulations are fewer and more lenient. Many sole proprietors work from home on the internet without a separate office building, so most of the government's regulations regarding sole proprietorships concern tax remittance, legitimate product standards, and ensuring that businesses are not selling illegal goods or products embargoed by the government. It is common and sensible for people who put their time and money into a firm to profit from it. The profit generated in other types of enterprises is shared among investors and shareholders based on their respective contributions to the company. There is no sharing arrangement in a sole proprietorship since the sole proprietor takes all the business profits after paying for production costs. The sole proprietorship opens up many possibilities for the owner to interact with most of his clients and customers. A client or consumer of a sole proprietorship business dissatisfied with the quality of goods or services supplied by the company may communicate directly with the proprietor. In other types of enterprises, reports from one particular client or consumer are highly unusual, reaching the company's owners. Customers may be required to submit reports to a customer service department staffed by individuals who have never met the company's owners or shareholders before, for example. Even though a single proprietorship has a customer care service, the firm's owner would be immediately informed because employees report directly to the single proprietor. A solo proprietorship typically has a positive and beneficial relationship between the business owner and employees (if the sole proprietor's line of business necessitates the use of additional people). The sole proprietor personally inspires and encourages staff to be aware of company goals and objectives, fostering organizational loyalty among them. Employees are more likely to work harder for a sole proprietorship since the owner is personally invested in the success of his business and encourages them to accomplish amazing things while employed there. As a sole proprietor, you are responsible for reporting your business income and expenses annually to the IRS and the state. The tax obligation of a single owner is lower and more simple than that of other types of companies. A single owner usually pays yearly taxes from his earnings working full-time in his firm. If a single owner has multiple sources of revenue, he is also charged income tax on all of them, including those earned through his sole proprietorship business. The pros and cons of a sole proprietorship are up for debate. However, it is difficult to deny that when a good and hardworking team has their eyes set on a goal, they usually reach it. Other businesses have more than one decision-maker, which provides objectivity to the company's choices. On the other hand, sole proprietorships often lack this objectivity because the owner may act based on emotions rather than rationality. What happens to a sole proprietorship if the owner gets sick or has an unexpected yet essential course of action to pursue? The preceding question and others that highlight the flaws of a sole proprietorship make it vital to pinpoint and analyze the drawbacks of a sole proprietorship, as described in the following paragraphs. In a sole proprietorship, one person owns and controls a business. There is no legal requirement for the sole proprietor to file for who will take over the administration of the business after their death or when they can no longer manage it. The future management and control of a sole proprietorship are usually unclear because there is usually no arrangement for that purpose. A sole proprietor may want his child, family, or friend to take over the firm after death, but they may not be interested in the business. If a person who has been given authority to assume control of the company refuses to do so at the death or incapacity of the sole owner, legal action cannot be launched against him since there is no relevant article or memorandum of association for a single proprietorship as there is in other forms of businesses. A sole proprietorship usually dies with the owner and cannot continue even if the owner wants it to. This lack of continuity affects not only the business itself but its customers as well. For example, what consequences will a person face if they paid for a product from a sole proprietor in advance but did not receive the merchandise before the owner's death? How could this person prove that payment was made if the spouse or child of the deceased did not discontinue running Sole Proprietorship after their death? Because the law does not need to detail a sole proprietorship's continuity plan, the continuation of a sole proprietorship is always in question. Before investing in a business venture, the entrepreneurs must study the project's feasibility to minimize risk factors. However, this does not mean that there is zero chance of failure. A company's success or failure cannot be anticipated before it is established. When other types of businesses fail, all the owners of the firm share in the loss, just as each member of successful business benefits from the profit. If a sole proprietorship fails, only the owner suffers any loss, as he gains alone if the company succeeds. This implies that having the mental toughness to deal with one's own investment losses is difficult. The most stressful outcome of this disadvantage is shouldering the blame and responsibility for a business failure that could have been avoided if the sole proprietor had teamed up with another entrepreneur from the start. Unfortunately, business often entails conflict and misunderstanding between parties, which can result in court cases. Conflicts can develop between the sole proprietor and clients, workers, the landlord, or even the government. When individuals with such disputes go to court, the sole proprietorship will sue or be sued since it is not a legal entity under current legislation. Corporate entities and business owners are generally not held liable for damages done by the company in a court of law. This means that legally speaking, the shareholders and owners of such businesses differ from the businesses themselves. In these cases, if damages are awarded against the company, it would be responsible for paying them out of its own funds, without taking any money from the shareholders or managers on a personal level. However, if such losses are awarded against a single proprietorship that has been set up, the sole proprietor would be responsible for them and would be sued on a personal basis since the sole proprietor is not a separate legal entity from the business they own and control. A sole proprietorship grows more slowly than other types of businesses for several reasons. The owner must provide all the capital needed to start and run the business, and they make all decisions without input from others. With other businesses, multiple people invest in its success and ensure their investment does not go to waste. This is why those businesses expand rapidly. A sole proprietor can only obtain bank loans with short durations, his own savings, or donations from relatives and friends. Investors who are prepared to fund a sole proprietorship to gain participation in the business would want the owner to convert it into a corporation where they may invest in return for shares and interests in the firm. A lack of cash might also prevent a sole proprietorship from surviving competition from other businesses with substantial funding that provide comparable products or perform similar services. If the sole proprietor is set in their ways, the business would be operated using methods that may not suit contemporary realities. Other forms of businesses encourage innovation because of shareholders' different backgrounds and experiences. Every person must pay their taxes on time. The money spent on taxes goes toward government projects that help improve our country. The owner of a sole proprietorship pays personal income tax on their own earnings, just as the owner of any other business does. The owner's payment for personal income taxes is calculated from the proprietor's income. This implies that if the sole proprietor runs the firm part-time while working at another company, as a sole proprietor, it is your responsibility to fill out your taxes accurately, including any profitable income or losses from the fiscal year. Your personal income tax will act as the tax for your sole proprietorship firm since you are not considered a separate person from the business. The procedure for submitting a personal income tax return form to the Internal Revenue Service (IRS) as an employee who receives compensation is very similar to that of a sole proprietor. The only distinction is that sole proprietors must record their profit or loss for the year in question. The amount of tax a sole proprietor owes is based on the profit they make from their business. This number is calculated by subtracting the expenses associated with running the business from the revenue earned. Future expenses or long-term debt owed are not considered when determining how much tax a sole proprietor will owe. In other words, a sole proprietor would only be taxed on the money they have saved in their bank accounts. A sole proprietor is allowed by law to write off the cost of production from their income tax. This includes employee salary, rental, advertisement, and office equipment expenses. By doing this, the sole proprietor's income tax will not include these necessary business costs. The Tax Cuts and Jobs Act, which was signed into law in 2017 and is effective from 2018-2025, allows single sole proprietors who earn over 157,500 US dollars but below 207,500 US dollars or married sole proprietors who earn over 315,000 US dollars but below 415,000 US dollars to take tax limited to a percentage of the wages paid to their workers. The category of sole proprietors mentioned above can also enjoy deductions if they have depreciable business property. It is crucial to note that the Tax Cuts and Jobs Act only applies to sole proprietors who incorporate their companies, that is, register their single business with the government. A single proprietor must keep track of both personal and company expenditures. The easiest method to do this is to set up a separate business account where money will be withdrawn to pay for company expenses. As a sole proprietor, you should also get into the habit of setting aside money for income tax which would be paid to the Internal Revenue Service at the end of the year. To avoid any pressure come tax season, contribute self-employment taxes which are 12.4% for Social security and 2.9% for Medicare. Self-employment taxes are paid by individuals who work for themselves and do not receive a salary or wages from an employer. Sole proprietorships are one of the most common types of businesses in the United States. This is because they are relatively easy and inexpensive to set up and maintain. Sole proprietorships offer entrepreneurs the opportunity to be their own boss and control their own business. However, sole proprietorships also come with a number of risks, such as unlimited liability. This means that the sole proprietor is personally responsible for all debts and losses incurred by the business. Sole proprietorships also tend to have difficulty raising capital, as there is only one owner. Overall, sole proprietorships can be a good option for entrepreneurs who are looking for a simple business structure with relatively low start-up costs.What Is Sole Proprietorship?

What Are the Benefits of Owning a Sole Proprietorship?

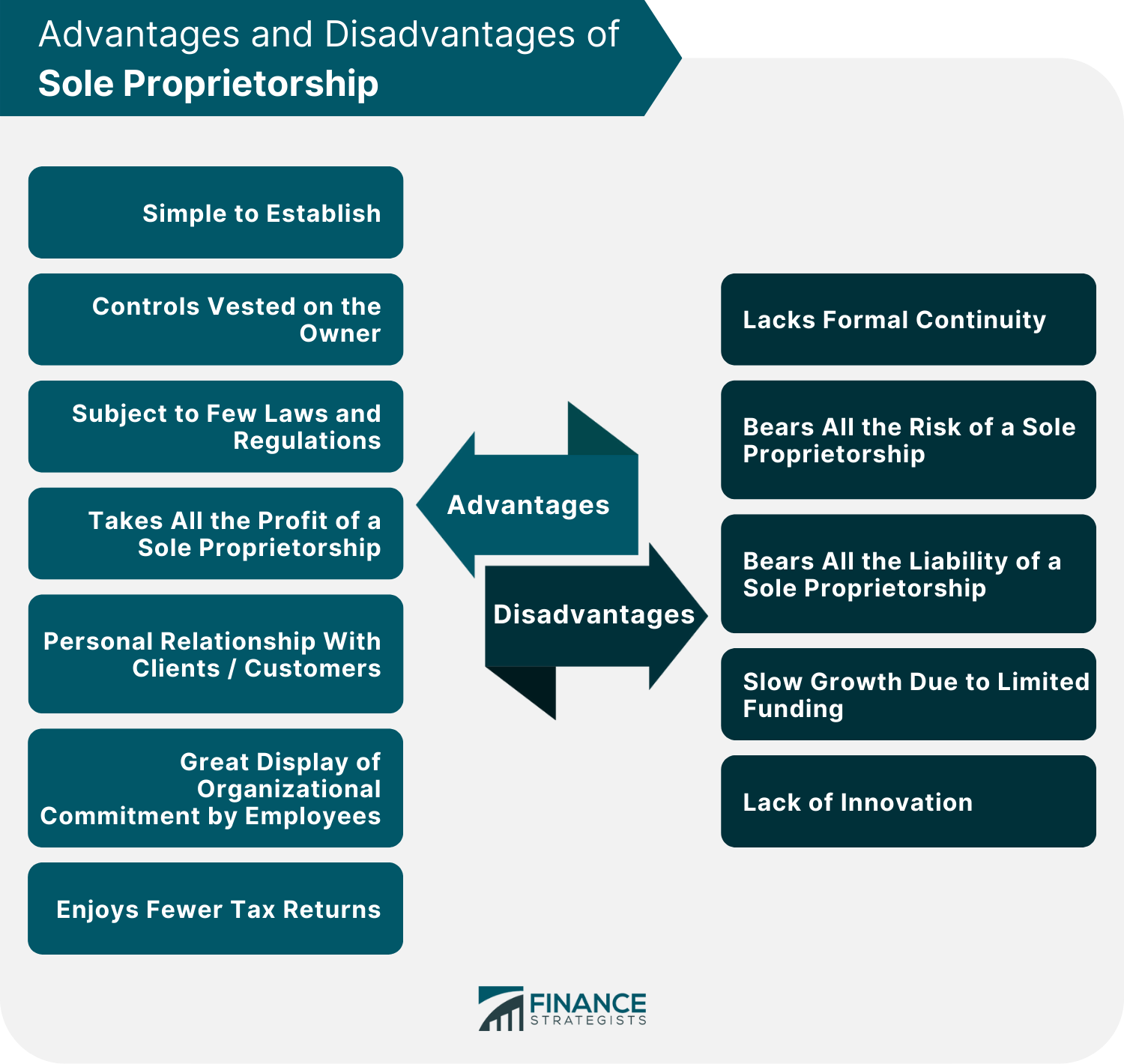

Simple to Establish

Controls Vested in the Owner

Subject to Few Laws and Regulations

Takes All the Profit of a Sole Proprietorship

Have a Personal Relationship With Clients and Customers

Great Display of Organizational Commitment by Employees

Enjoys Fewer Tax Returns

What Are the Disadvantages of Operating as a Sole Proprietorship?

Sole Proprietorship Lacks Formal Continuity

Bears All the Risk of a Sole Proprietorship

Bears All the Liability of a Sole Proprietorship

Slow Growth Due to Limited Funding

A Lack of Innovation

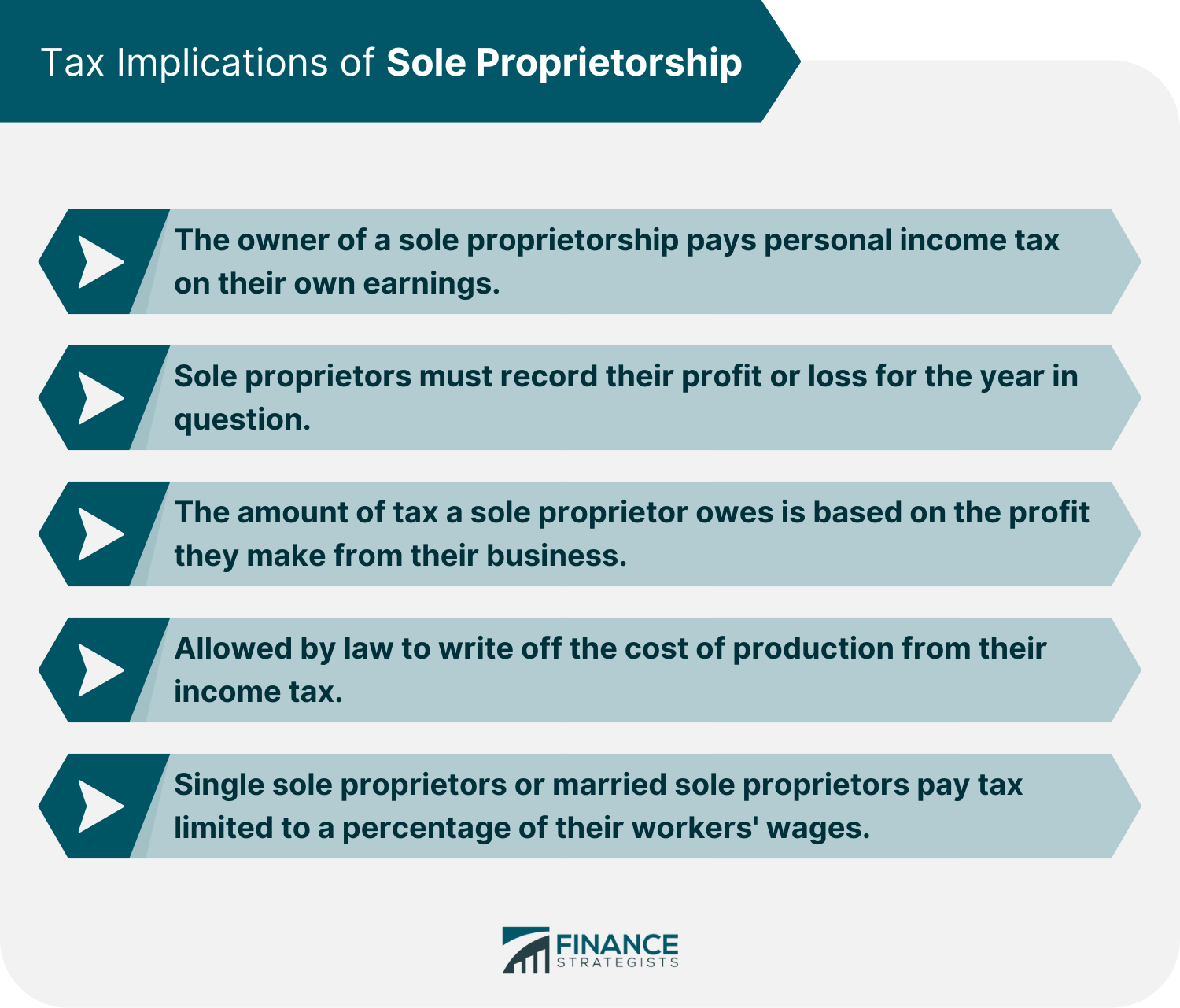

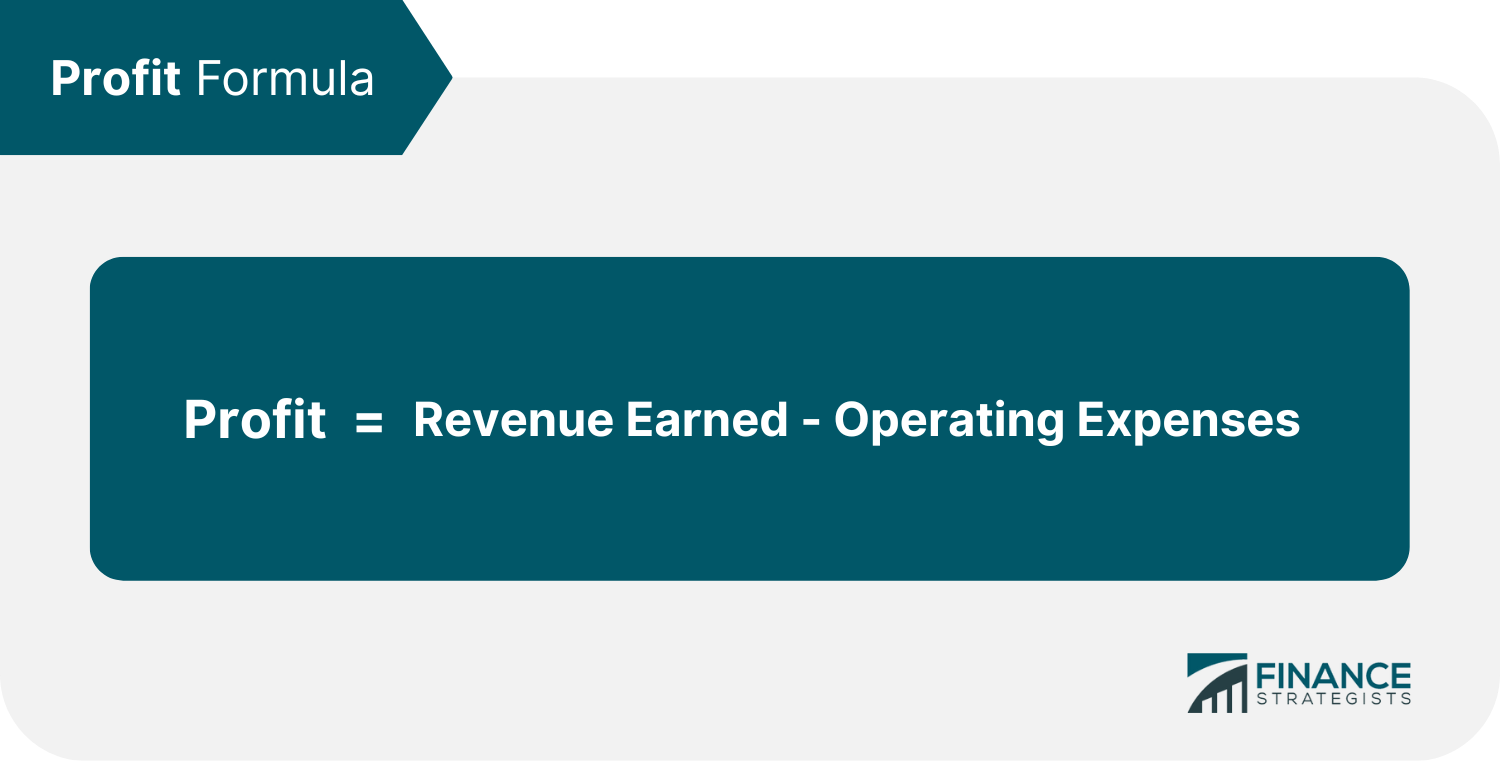

What Are the Tax Implications of Sole Proprietorship?

Conclusion

Sole Proprietorship FAQs

A sole proprietorship is a type of business ownership where there is only one owner. The owner has complete control over the business and is personally responsible for all debts and losses incurred by the business.

Some of the advantages of a sole proprietorship include being your own boss, having complete control over the business, and relatively low start-up costs.

Some of the disadvantages of a sole proprietorship include unlimited liability, difficulty raising capital, and lack of stability.

There is no formal process for setting up a sole proprietorship. You can simply start doing business yourself. However, you may need to obtain a business license or permit from your local government.

The characteristics of sole proprietorship are as follows: there is only one owner, the owner has complete control over the business, the owner is personally responsible for all debts and losses incurred by the business, and has relatively low start-up costs.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.