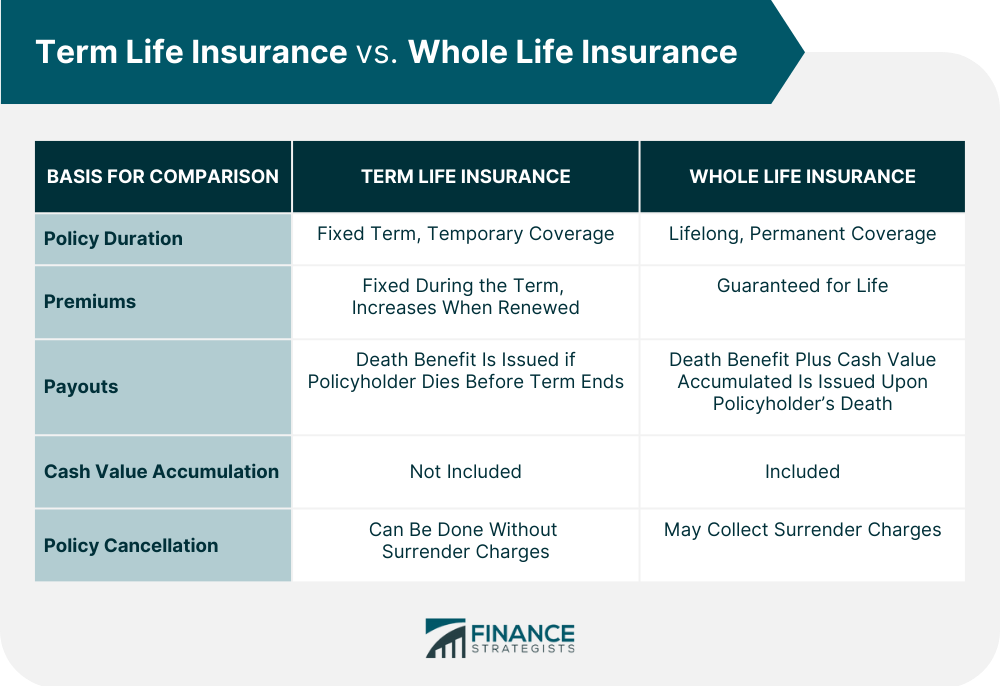

Life insurance is a necessary purchase that can provide financial security for the policyholder’s family in the event of their death. There are many types of life insurance, with different features that can suit various individuals. In this article, two types of life insurance will be discussed: term and whole life insurance. They differ in terms of duration of coverage, premium cost, payout composition, cash value inclusion, and cancellation rules. Each has its advantages and disadvantages. It is essential to understand the differences between them before choosing one. Term insurance might be more suited for individuals who prefer a less expensive and more flexible option. In contrast, whole life insurance suits those who want life-long coverage and cash value growth. Term life insurance is a temporary policy that provides death benefits for a specific period of time or a fixed term. They are usually a more affordable option as they offer lower premiums when compared to whole life insurance policies. With term life insurance, individuals can choose an amount of coverage that fits within their budget and select how long they want it to last. If they die during their policy term, the death benefit will be paid out to their designated beneficiaries. However, if they outlive the term, the policy will expire, and they will need to purchase a new one to stay insured, often at a higher premium. Whole life insurance is a permanent policy that provides death benefits for an entire lifetime. It remains valid for as long as the premiums are paid, regardless of the policyholder’s age or health status. A whole life insurance policy also has an investment component that builds cash value over time. These funds can be loaned anytime and used for various future expenses. Both the cash value and death benefit payments under this type of policy are typically tax-free. Whole-life policies usually have higher premiums than term-life policies due to their multiple features and longer life spans. A more in-depth differentiation can be made between term and whole life insurance policies based on the following factors: Term life insurance policies are designed to last only for a predetermined timeframe, ranging anywhere from 5 to 30 years. Policyholders choose a fixed term, usually in increments of 5 years, renewable once the time period is up. On the other hand, whole life insurance policies are designed to last the entire duration of the policyholder’s life. It remains in effect as long as premiums are paid on time. Generally, whole-life policies have higher premiums that are split into two components: the insurance cost and the cash value. Premiums are guaranteed, meaning the amount policyholders pay is the same for their entire lifetime. Term-life policies can have more affordable initial premiums that increase if policyholders renew after the coverage expires. However, due to changes in their age or health status, some individuals might be denied another term-life policy, even if they decide to renew. With term life insurance, beneficiaries will receive a one-time payout if the policy owner dies during the covered term. The total amount will depend on the death benefit stated in the policy. With whole life insurance, policyholders can borrow against or withdraw the cash value component while alive. At the time of the policy owner's demise, beneficiaries receive the death benefit and accumulated cash value. With a whole life policy, the insurer keeps track of the premiums and invests part of them, growing the cash value. Policyowners can access these funds if needed, although doing so can reduce the death benefit or increase premiums if they do not replenish them. In contrast, all the premiums under a term-life policy go to the insurance cost. Thus, these policies only offer a death benefit and do not accumulate any additional cash value. Policyowners can terminate either policy anytime, though term-life policies automatically expire after the set period. Nonetheless, policyholders can stop paying premiums and lose coverage without paying surrender charges. Cancelling whole life insurance may result in the payment of surrender charges. In addition, if policy owners stop paying premiums without formally cancelling their policies, their insurance provider can deduct premiums from the accumulated cash value until it is consumed. Term life policies come with both advantages and disadvantages. Term life insurance is typically much cheaper than whole-life policies, which makes it more affordable for those who want insurance on a budget. Individuals can choose how long they want their policy to be in effect, allowing them the flexibility to tailor the coverage to their needs. These policies also may not require a medical exam, which means the requirements to obtain one are more lenient, and many individuals can quickly get approved. Term policies have limited lifespans, so their insurance coverage is not permanent. Premiums may increase upon renewal or extension. Moreover, since the policyholder is older and may have significant changes in health, they might be denied even if they want to renew their policy. Term-life policies also offer fewer features than whole-life policies. For instance, they do not accumulate any cash value over time. Therefore, they are not suitable as investment vehicles or financial planning tools. This type of permanent life insurance also has its benefits and drawbacks: Whole life insurance is permanent. If policyholders keep paying premiums, their policy will remain active until death. It can also provide financial predictability because insurance premiums are fixed and guaranteed for life. Whole life insurance also offers benefits such as possible rider options and a cash value component that can be accessed anytime through tax-free loans while policy owners are still alive. These funds are also paid out with the death benefit upon the policyholder’s demise. Whole life insurance premiums tend to be much higher than term-life policies, making them less suited to budget-conscious individuals. It is also less flexible than the latter since policy owners have less freedom to select the duration of their policy. Applying for whole life insurance is more complicated because it often requires a medical exam while cancelling one is more costly because it involves surrender charges. Lastly, loans from a whole life policy’s cash value can reduce the death benefit if they remain unpaid. Consider your situation when choosing between these two types of policies. Are you looking for something that covers a specific period, say until your children graduate college, or are you seeking long-term solutions? Do you want a policy with an investment component? Term life insurance is a more cost-effective way to protect yourself for the short term, while whole life insurance can provide you coverage into later years with some added features, like cash value accumulation. Determining which of the two best suits your needs can be challenging. To help simplify things, speaking with an experienced insurance broker might provide you with helpful insight to decide what works best for yourself and your loved ones. If you have considered the preceding, talked with an expert, and still could not decide between term or whole life insurance, you might want to look at these alternatives: Universal life insurance is also a type of permanent policy. Like whole-life policies, they provide coverage for the policyholder’s lifetime or as long as premiums are paid. They also typically come with a cash value component which can be borrowed or withdrawn in times of need. However, it provides more flexibility because policyholders can adjust death benefits, cash value, and premium payments. Furthermore, universal life insurance often has lower costs and more investment options than whole-life insurance policies. This type of insurance combines features of whole and universal life policies. It also provides a death benefit and cash value. However, unlike universal life policies, the cash value is invested in more high-risk yet high-reward financial vehicles. The total value of a variable life policy can increase or decrease depending on how its investments perform. These policies are more complex and require more active participation. Thus, getting the help of an expert before buying this type of policy might be helpful. This is also known as burial or funeral insurance. It is a type of permanent life insurance with a smaller death benefit amount intended for a specific purpose. Like term-life policies, they do not have a cash value component. This type of policy may be a good choice for individuals who want their families to be spared the financial burden of paying for their funerals. Hence, it is a popular choice for seniors. Life insurance is a great way to financially protect yourself and your loved ones in case something unexpected happens to you. Term and whole life insurance policies differ in several ways, including duration, premiums, payouts, cash value, and cancellation. These policies come with certain benefits and drawbacks. When considering between the two, consider your short- and long-term goals, needs, and financial capacity carefully. Also, factor in the other alternative policies available so you can make an informed decision. If all else fails, get help from a licensed insurance broker who can guide you through the process. Doing this will ensure that whatever type of life insurance you choose is right for you.Term vs. Whole Life Insurance: An Overview

What Is Term Life Insurance?

What Is Whole Life Insurance?

Term vs. Whole Life Insurance: Comparison

Policy Duration

Premiums

Payouts

Cash Value Accumulation

Policy Cancellation

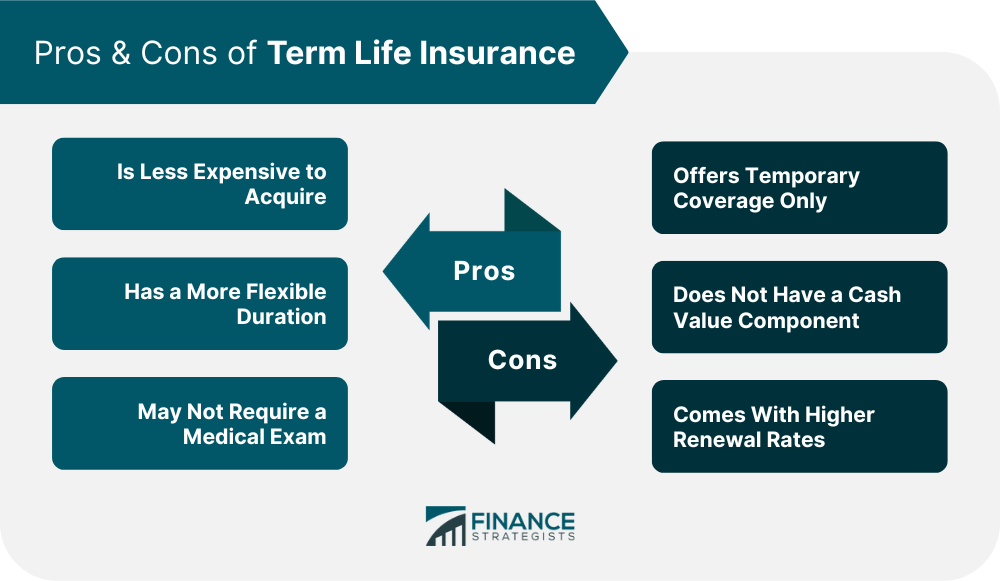

Term Life Insurance Pros & Cons

Pros

Cons

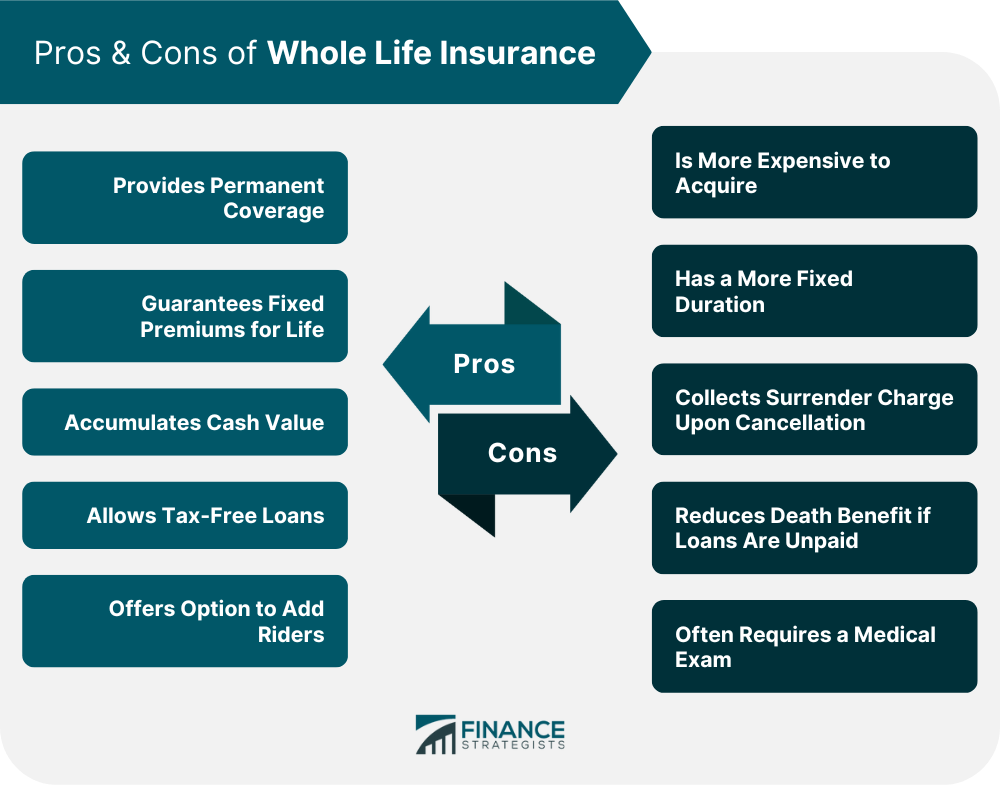

Whole Life Insurance Pros & Cons

Pros

Cons

Term vs. Whole Life Insurance: Which Is Right for You?

Other Life Insurance Alternatives

Universal Life Insurance

Variable Life Insurance

Final Expense Insurance

The Bottom Line

Term insurance might be more suited for individuals who prefer a less expensive and more flexible option. In contrast, whole life insurance suits those who want life-long coverage and cash value growth.

Term vs. Whole Life Insurance FAQs

Term life insurance provides coverage for a set period with lower initial premiums, which may increase upon renewal. In contrast, whole-life policies offer lifelong coverage and cash value accumulation, which you can borrow from or use as an asset in retirement planning. Whole life insurance premiums are higher but do not change during the policy's life.

Since term life insurance policies do not have a cash value component, policyholders cannot cash them out. Instead, cancelling the policy or reaching the end of the term means the conclusion of the insurance coverage.

Your insurance coverage ends at the end of the policy’s term. You can convert it into a whole-life policy before it expires or extend it, which typically results in higher premiums. You may also get quoted for a new term life insurance policy altogether.

The most suitable insurance policy depends on your situation, needs, and goals. Term insurance might be more suited for individuals who prefer a less expensive and more flexible option. In contrast, whole life insurance suits those who want life-long coverage and cash value growth.

Death benefits from life insurance policies are generally not considered taxable income. However, if the policy is considered part of a decedent’s estate and the death benefit exceeds the estate tax exemption, the excess amount will be taxed. In contrast, the cash value from a whole life insurance policy may be taxed as ordinary income when withdrawn.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.