A testamentary trust is a type of trust that is established in accordance with the instructions outlined in a last will and testament. It is a legal arrangement that allows a trustee, a third-party individual or entity, to manage the assets of the deceased on behalf of the trust's beneficiaries. The primary importance of a testamentary trust in estate planning is ensuring that assets are distributed according to the deceased's wishes. By establishing a testamentary trust, individuals can provide for their loved ones and control the distribution of their assets, even after they pass away. Testamentary trusts can be particularly useful in situations where the beneficiaries are minors, individuals with special needs, or those who may not be able to manage their own finances. Have questions about Testamentary Trusts? Click here.

The structure of a testamentary trust is straightforward. A trustor or grantor creates a will that includes instructions for establishing the trust. The trustor names an executor or executrix in the will who will oversee the distribution of the estate and ensure that the trust is created as outlined. When the trustor passes away, the executor begins the probate process, which involves verifying the authenticity of the will and the executor's authority to distribute the assets of the estate. Once the probate process is complete, the trust is activated, and the estate assets are transferred into the newly created trust. The trustee is responsible for managing the assets held in the trust on behalf of the beneficiaries. The trustee has a fiduciary duty to act in the best interests of the beneficiaries and must follow the instructions outlined in the will when distributing the assets. One of the benefits of a testamentary trust is that it can be established with specific conditions for distributing the assets to beneficiaries. For example, the trust may state that the assets can only be accessed by a beneficiary for educational expenses until they reach a certain age, at which point the remaining balance is paid out. A testamentary trust can also be established to manage the charitable distribution of assets in accordance with the wishes of the deceased. This can allow individuals to continue supporting causes they care about even after they pass away. A testamentary trust is a legal arrangement that typically involves three parties: the grantor or trustor who creates the trust, the trustee who manages the trust's assets, and the beneficiary or beneficiaries named in the will. When setting up a testamentary trust, the trustor can create it within their will, which becomes effective upon their death. To establish a testamentary trust, the will must be probated, a legal process that involves verifying the authenticity of the will and appointing the executor or executrix. Once the probate process is completed, the executor is instructed to create the trust and transfer the property into the trust. The trustee then manages the assets until the trust expires and the beneficiaries receive their distribution. The trust's expiration date is usually tied to a specific event, such as the beneficiary reaching a certain age or completing a specific educational milestone. During the trust term, the probate court may periodically check in to ensure the trust is managed correctly. It is important to note that while the trustor can choose anyone to act as the trustee, the appointed trustee is not obligated to accept the role and may decline the request. In such cases, the court may appoint a trustee, or a relative or friend of the beneficiaries may volunteer to act as the trustee. Overall, setting up a testamentary trust requires careful planning, and it is crucial to seek the advice of a legal and financial professional. The testamentary trust can be a useful tool in estate planning, helping to ensure that assets are distributed in accordance with the trustor's wishes and managed responsibly until the beneficiaries receive their distribution. A parent establishes a testamentary trust for their minor child. The trust outlines that the child is to receive their inheritance when they turn 25. However, until the child reaches age 25, the trustee is authorized to distribute income from the trust to the child for certain purposes, such as education, healthcare, or basic living expenses. The testamentary trust also includes a spendthrift provision that prevents the child from accessing the trust assets before the age 25 or from using the trust assets to pay off debts or judgments. The parent is confident that this arrangement will ensure the child's inheritance is managed wisely and will not be squandered on frivolous expenses. In this example, the testamentary trust is established to provide financial support for the child during their formative years while still protecting their inheritance until they reach a certain age. Using a trust structure, the parent can ensure that the child's inheritance is managed responsibly and used for its intended purposes. Testamentary trusts can provide several benefits for estate planning purposes, including: By establishing a testamentary trust, the trustor can dictate exactly how their assets will be distributed to their beneficiaries after death. This can include conditions that must be met before assets are distributed, such as reaching a certain age or achieving specific milestones. This provides control over how assets are distributed and ensures that beneficiaries receive the assets responsibly and appropriately. One of the benefits of a testamentary trust is that it can protect assets from creditors. This is because the assets in the trust are separate from the beneficiary's personal assets and are not considered part of their estate. This means creditors cannot go after the trust assets to satisfy outstanding debts or judgments. Testamentary trusts can be established to support minors financially until they reach a certain age. This can help ensure that the minor's financial needs are met while still protecting their inheritance until they are mature enough to manage it themselves. Testamentary trusts can also be used to reduce estate taxes by removing assets from the estate before they are subject to estate tax. This can help maximize the amount of assets that are passed on to beneficiaries and minimize the amount that is lost to taxes. Testamentary trusts can provide professional management of assets by appointing a trustee to manage the assets on behalf of the beneficiaries. This can be especially useful for complex assets or for beneficiaries who may not have the expertise or experience to manage the assets themselves. While a testamentary trust can provide several benefits for estate planning purposes, there are also potential drawbacks that should be considered. Some of the potential drawbacks of a testamentary trust include the following: One of the main drawbacks of a testamentary trust is that assets cannot be distributed until after the trustor has passed away and the probate process has been completed. This means beneficiaries may have to wait several weeks or months to receive their inheritance. This delay can be especially problematic if beneficiaries need the assets for immediate financial needs. Another potential drawback of a testamentary trust is that it can increase the costs and complexity of estate planning. This is because the trust must go through the probate process and may require the services of an attorney, trustee, or other professionals to manage the trust. This can add to the overall cost and complexity of the estate planning process. A testamentary trust is established through a will, which becomes a public record once it goes through the probate process. This means that the assets' distribution and the trust's terms become public information, which may not be desirable for some individuals. A testamentary trust is typically irrevocable, which means that the terms of the trust cannot be changed once the trustor has passed away. This lack of flexibility can be problematic if circumstances change after the trust has been established and the beneficiaries or trustees would like to modify the terms of the trust. Since a testamentary trust is established through a will, it is subject to the probate process. This means that the trustor's assets must go through a legal process before being distributed to the beneficiaries, which can be time-consuming and expensive. A testamentary trust is a trust established by the terms of a will and comes into effect upon the death of the trustor. The executor of the will appoints the trustee and is responsible for managing the trust's assets until the trust's expiration date. In contrast, a living trust is established during the trustor's lifetime and is managed by the trustee or the trustor. The trustor can serve as the trustee or appoint a third-party trustee to manage the trust's assets. One of the key differences between a testamentary trust and a living trust is the time at which they become effective. A testamentary trust becomes effective upon the trustor's death, while a living trust becomes effective during the trustor's lifetime. Another significant difference is the trustor's level of control over the trust's assets. With a testamentary trust, the trustor has no control over the trust's assets once the will is executed, and the trustor's heirs have no access to the assets until the trust term expires. In contrast, a living trust allows the trustor to manage and control its assets during their lifetime. One of the main benefits of a testamentary trust is that it is simple to set up and does not require the assistance of an attorney or financial advisor. Additionally, because the trust is established within the will, the trustor can change the terms of the trust by amending their will. However, a significant drawback of a testamentary trust is that it is subject to probate, a court-supervised process that can be lengthy and costly. Moreover, the trustor has no control over the trust's assets once the will is executed, and the trustor's heirs have no access to the assets until the trust term expires. One of the main benefits of a living trust is that it is effective immediately, and the trustor can manage and control the trust's assets during their lifetime. Additionally, a living trust is not subject to probate, which can save time and costs associated with probate. However, a significant drawback of a living trust is that it can be complex to set up and requires the assistance of an attorney or financial advisor. Additionally, a living trust can be more expensive than a testamentary one. The choice between a testamentary and living trust ultimately depends on the trustor's goals and circumstances. A testamentary trust is a simple and cost-effective way to transfer assets to heirs, but it is subject to probate and provides limited control over the trust's assets. On the other hand, a living trust is more complex to set up but allows the trustor to maintain control over the trust's assets and avoid probate. A testamentary trust is a useful tool for estate planning that can provide many benefits, including control over asset distribution, protection from creditors, and professional management of assets. However, there are also potential drawbacks, such as delayed asset distribution and increased costs and complexity. The decision between a testamentary trust and a living trust depends on the trustor's goals and circumstances, and the choice should be made after considering the advantages and disadvantages of each option. To make informed decisions about estate planning, consulting with a financial advisor who can provide tailored advice and guidance is recommended.What Is a Testamentary Trust?

How Testamentary Trusts Work

Requirements for a Testamentary Trust

Example of a Testamentary Trust

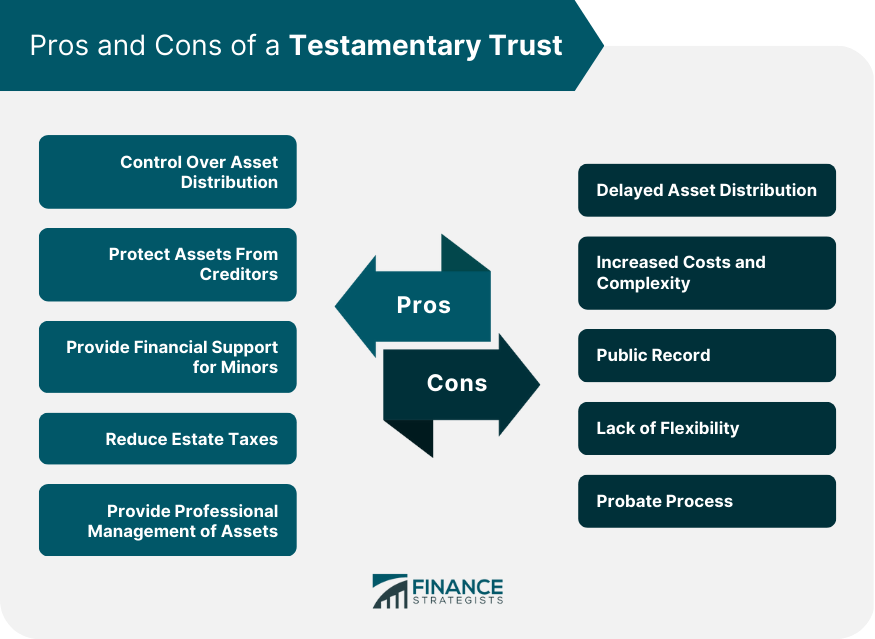

Pros of a Testamentary Trust

Control Over Asset Distribution

Protect Assets From Creditors

Provide Financial Support for Minors

Reduce Estate Taxes

Provide Professional Management of Assets

Cons of a Testamentary Trust

Delayed Asset Distribution

Increased Costs and Complexity

Public Record

Lack of Flexibility

Probate Process

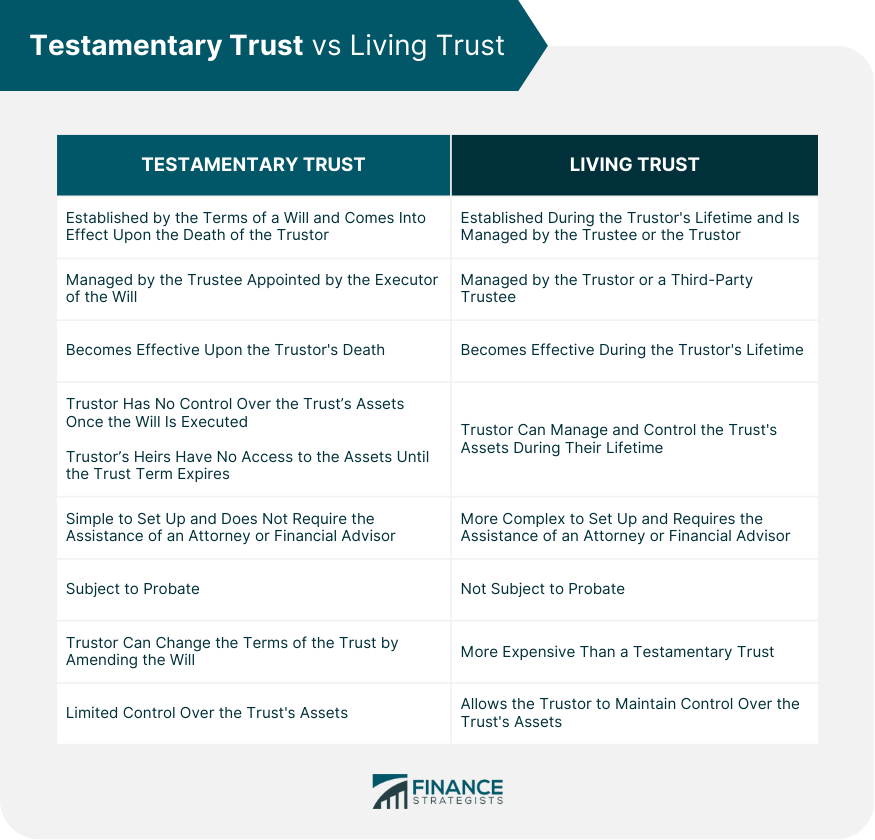

Testamentary Trust vs Living Trust

Final Thoughts

Testamentary Trust FAQs

A testamentary trust is established in accordance with the instructions outlined in a last will and testament. It comes into effect after the trustor's death and is managed by a trustee who oversees the distribution of the estate's assets.

A testamentary trust can provide several benefits for estate planning purposes, including control over asset distribution, protecting assets from creditors, providing financial support for minors, reducing estate taxes, and providing professional management of assets.

Some potential drawbacks of a testamentary trust include delayed asset distribution, increased costs and complexity, lack of flexibility, the probate process, and the trust becoming a public record.

A testamentary trust is established by the terms of a will and comes into effect upon the trustor's death, while a living trust is established during the trustor's lifetime and is managed by the trustee or the trustor. A testamentary trust is subject to probate, while a living trust is not.

Any competent adult, including family members, friends, or financial institutions, can be named as a trustee. It is important to choose someone who is trustworthy, responsible, and has some experience managing finances.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.