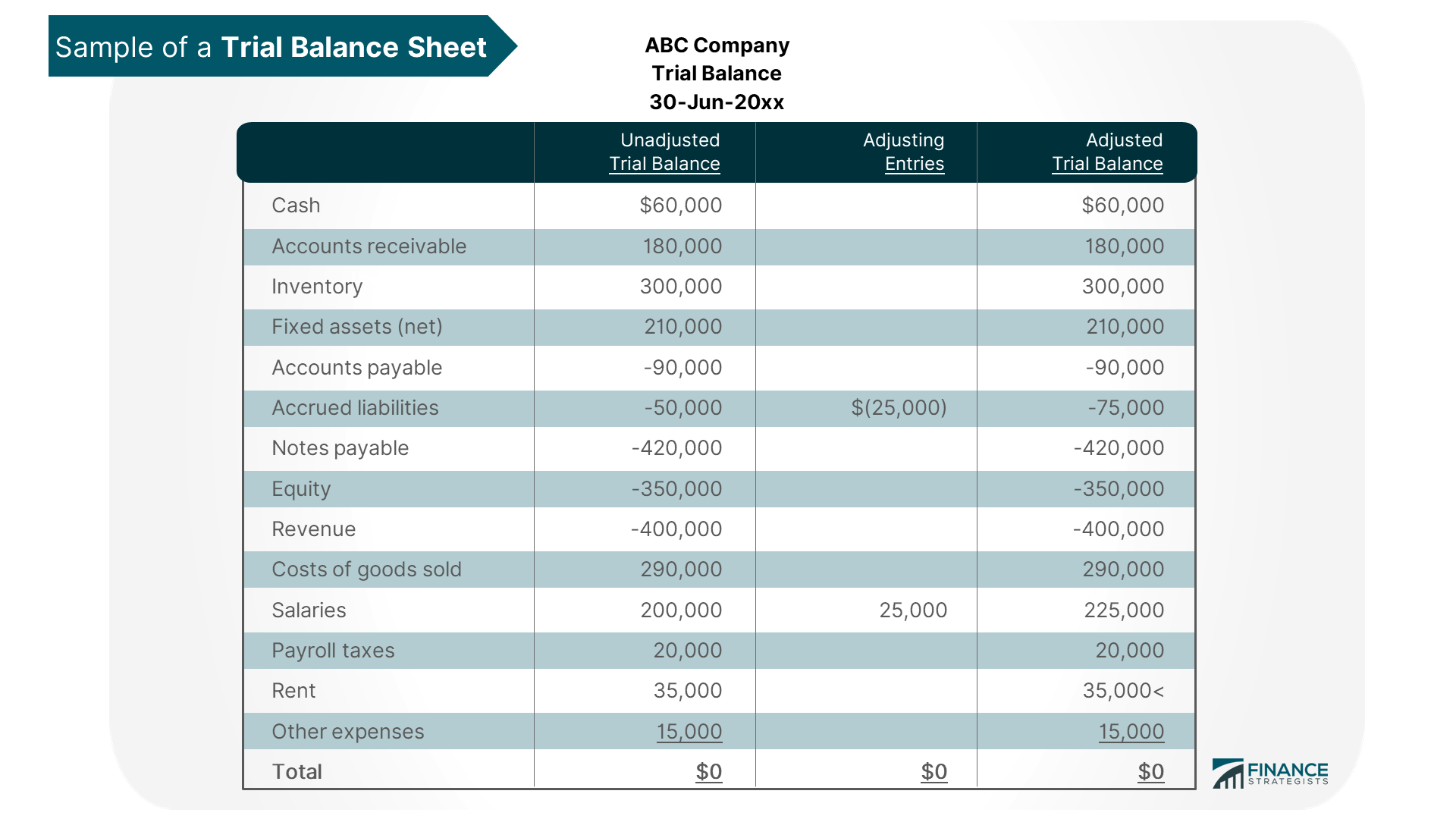

An unadjusted trial balance is a list of all accounts as of the end of an accounting period. The balances on this trial balance sheet are usually taken from an account ledger or bookkeeping records. The Unadjusted Trial Balance (UTB) document summarizes all of the accounts in an organization at a single point or period. It will include all revenue, expenses, and assets. It is considered unadjusted because no adjusting entries have been made yet. The Adjusted Trial Balance (ATB) is the same as UTB except that it also includes any adjusting entries made during an accounting period. In other words, a trial balance will show all of the balances of accounts after all transactions have been allowed for, including those which have not yet been entered into a general ledger or subsidiary ledgers. It is “adjusted” because all of the transactions that have affected the organization’s accounts (both debit and credit) are included on it. This makes it easier to prepare financial statements since they will contain one less step. Adjusting entries are necessary to bring the trial balance into alignment with the books of account and summary worksheets. These entries can include adjusting journals that summarize: 1. revenue and expenses, including depreciation expense; 2. supplies beginning and ending balances; and, 3. other miscellaneous adjustments such as bad debts, foreign currency translation, and gains or losses from marketable securities. These adjusting entries have the effect of making certain that the total debits equal the total credits in each account. Create a master list of accounts (assets, liabilities, equity, revenue & expenses) used in your company’s accounting system. Start entering the balances for each account into the 1st column of an unadjusted trial balance spreadsheet (UBTB). You can do this by either totaling the last period’s closing balances or you can enter balances as of the 1st day of this period. Enter all account transactions that have occurred during this accounting period into the 2nd column of UBTB. As you enter each transaction, the account’s balance will change accordingly in both the 1st and 2nd columns. Once you have entered all of your transactions for this accounting period, the 1st and 2nd columns of UBTB will contain the opening and closing balances for each account. You can now compare your 1st column with the last period’s closing balances or the 1st day of this period’s balances to ensure accuracy. In case of errors, simply edit the 1st and 2nd columns of UBTB until you get the correct balances. Having an unadjusted trial balance is important because it is the first step in creating financial statements. It will contain all assets, liabilities, and equity accounts so they can be used to prepare your company’s income statement and balance sheet. The unadjusted trial balance (UTB) is an important tool for monitoring your company’s operating results. It will allow you to spot-check the accuracy of the first step in preparing your company’s financial statements – that is, entering balances from your account ledger into a spreadsheet. In summary, the unadjusted trial balance (UTB) lists all accounts in an organization at a given point or period of time. It will include both debit and credit balances, but no adjusting entries have been made yet. Whereas, the adjusted trial balance (ATB) is the same as UTB except that it also includes any adjusting entries made during an accounting period. In order to create a true picture of your business, you should always prepare an income statement and balance sheet for the current month’s closing date. It is only after all financial statements have been prepared that any adjusting entries can be entered into a general ledger or subsidiary ledgers. This will ensure all revenues, expenses, gains, and losses are accounted for. In the end, making sure you have a UTB to compare with your ATB is important because it will ensure that all accounts in your organization are accurate and complete. It will also help you avoid missing closing entries or incorrectly entering adjusting entries into UTB or ATB.How Does It Differ From the Adjusted Trial Balance?

Why Is It Important to Adjust the Balance Trial?

How to Calculate Unadjusted Trial Balance

Step 1:

Step 2:

Step 3:

The Importance of the Unadjusted Trial Balance

Why You Should Care About the Unadjusted Trial Balance

The Bottom Line

Unadjusted Trial Balance FAQs

An unadjusted trial balance is a listing of all the company's accounts and their balances at a specific point in time, usually at the end of an accounting period before any adjusting entries have been made.

While every company maintains a record of its account balances in its general ledger, financial statements can only be complete and accurate if all accounts are prepared accurately. Unadjusted and Adjusted Trial Balance is done to prepare final accounts which can then be used as a basis for recording adjusting entries to prepare the adjusted trial balance.

The unadjusted trial balance is prepared to check if all accounts have balances. It helps ensure that all transactions for a given period are accounted for before adjusting entries are made.

There are three steps in preparing an Unadjusted Trial Balance: 1) Enter opening balances from the general ledger; 2) Enter all transactions, whether debits or credits that have occurred during a given accounting period into a document; and 3) Prepare a list that compares the 1st column with either the last period's closing balance or the 1st day of the accounting period's balance.

It consists of three parts: Accounts, Debits, and Credits. It has a separate column for each account, which is then broken down by debit and credit balances.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.