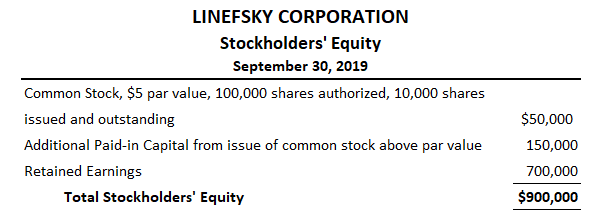

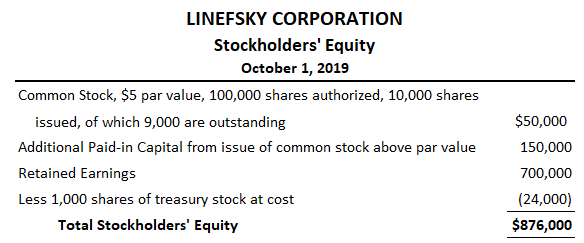

Treasury stock is the corporation’s own capital stock, either common or preferred, that has been issued and subsequently reacquired by the firm, but not canceled. Such stock, which is held in the corporate treasury, loses its right to vote, receive dividends, or receive assets upon liquidation. In computing earnings per share (EPS), treasury stock is not considered outstanding and must be deducted when determining the weighted average number of shares outstanding. The shares of treasury stock are held by the issuing corporation, which cannot exercise any of the rights of ownership apart from the right to sell them. With the exception of the possible impact on the amount of legal capital, these shares are in substance the same as unissued shares and should generally be accounted for under that assumption. There are a number of valid business reasons why a firm may reacquire its own capital stock. Specifically, a firm may need to acquire additional shares for the following purposes: A corporation’s board of directors may decide to acquire treasury shares for various reasons. One reason for this action is to obtain shares for re-issuance when all authorized shares are issued and outstanding. By purchasing shares from stockholders, the corporation can use them, for example, as part of the compensation to executives without having to go through the legal difficulties of amending the Charter to allow additional shares to be issued. Many corporations also acquire treasury shares as a way of investing in corporate funds. For example, the board of directors may believe that the capital market has undervalued the company’s shares and, accordingly, decide that an investment of funds in treasury stock is worthwhile. This practice is subject to legal limitations. First, the amount of treasury stock is generally limited by state law to the balance of retained earnings. Second, securities laws restrict the amount of purchases and sales by the board due to the potential for manipulation, as well as their access to insider information not available to the public. Third, the fiduciary responsibilities of the board require it to protect the interests of all creditors and stockholders such that an excessive amount of funds should not be spent to obtain shares. Treasury stock is also acquired in order to retire the shares of one or more stockholders. At an extreme, a few influential stockholders may decide that they would like exclusive control over the corporation by buying out the others. This process of going private is often accomplished through treasury stock purchases because corporate funds are used instead of the personal resources of the surviving stockholders. Another reason for acquiring treasury stock exists for corporations whose shares are not traded on an active basis. In these cases, the board may accommodate stockholders by agreeing to buy their shares when they wish to liquidate their holdings. Treasury stock is not considered an asset; it is a reduction in stockholders’ equity. Nor can a firm record a debit on the subsequent sale of treasury stock. Any difference between the reacquisition price and the selling price is either an increase in paid-in capital (if the shares sold at a gain) or a decrease in paid-in capital and/or retained earnings (if the shares sold at a loss). Finally, no treasury stock held by the corporation has any dividend or voting rights. To show how the purchase of treasury stock is recorded, assume that the stockholders’ equity section of the Linefsky Corporation’s balance sheet on 30 September 2019 is as below: On 1 October, the corporation repurchased 1,000 shares of its common stock at $24 per share. This transaction is recorded by debiting the stockholders’ equity account (i.e., Treasury Stock) and crediting Cash for the cost of the purchase as follows: Immediately after this purchase, the stockholders’ equity section of the Linefsky Corporation appeared as follows: As this partial balance sheet shows, treasury stock is not shown as an asset but as a negative item in stockholders’ equity. The effect of the transaction is to reduce both assets and stockholders’ equity by $24,000. The corporation can sell its treasury stock at any time. The subsequent resale can be either above or below its repurchase price. However, in no case is the net income for the current period affected. When treasury stock is resold above its cost, Cash is debited for the entire proceeds. Treasury Stock is credited for the total cost of the shares sold, and the account Additional Paid-in Capital from the Sale of Treasury Stock Above Cost is credited for the difference. The Additional Paid-in Capital account is credited for the economic gain because current accounting and tax rules do not allow corporations to record a profit and, in this way, increase retained earnings by dealing in its own stock. To demonstrate, let’s continue with the example of Linefsky Corporation introduced earlier in this article. Suppose that on 29 November 2019, 500 shares of treasury stock purchased at $24 per share were sold at $30 per share. To record this sale, Linefsky Corporation makes the following entry: If treasury stock is resold below cost, an economic loss will occur. This loss does not affect the current period’s income but reduces the credit balance in the paid-in capital account that resulted from other treasury stock transactions. If there are no previous treasury stock transactions, if the balance in this paid-in capital account is not large enough to cover the loss, or if there is no other paid-in capital account from the same class of stock, Retained Earnings is debited. To illustrate, now assume that the remaining 500 shares of treasury stock were resold on 24 December at $15 per share. The following entry is made to record this sale: In this case, Paid-in Capital From Sale of Treasury Stock Above Cost is debited for only $3,000 (i.e., the balance in this account that resulted from the previous resale). The remaining $1,500 difference of the $4,500 economic loss is charged to Paid-in Capital From Sale of Common Stock Above Par. If there had not been a credit balance in this account, the difference would have been debited to Retained Earnings. Like cash dividends, treasury stock purchases return cash to stockholders. The essential difference between dividends and treasury stock is that all shareholders receive cash when dividends are issued, but only stockholders who resell the stock to the corporation receive cash from treasury stock transactions. Thus, one way the corporation can avoid dividend restrictions is to purchase treasury stock. As a result, when creditors require restrictions on dividend payments, they also often require restrictions on treasury stock purchases.Treasury Stock: Definition

Treasury Stock: Explanation

Reasons for the Acquisition of Treasury Stock

Accounting for Treasury Stock

Recording the Purchase of Treasury Stock

Recording Resale Above Cost

Recording Resale Below Cost

Restrictions of Retained Earnings and Treasury Stock

Treasury Stock FAQs

Treasury Stock is the corporation’s own capital stock, either common or preferred, that has been issued and subsequently reacquired by the firm, but not canceled.

There are a few potential benefits for companies that buy back their own shares. First, it can help to boost the value of the remaining shares by reducing the number of outstanding shares. This can make the stock more attractive to investors and help to drive up the share price. Additionally, buying back shares can be a way for companies to return money to shareholders, and it can also help to reduce the company's overall financial risk.

There are a few potential risks associated with Treasury Stock. First, if a company buys back its shares at a price above the current market value, it can reduce the overall value of the company. Additionally, buying back shares can be a way for companies to return money to shareholders, which can impact the company's ability to reinvest in its business or pay down debt. Finally, if a company holds too much Treasury Stock, it can actually increase the company's financial risk.

If a company has purchased treasury shares at a total cost of $25 per share, then sells those shares for $24, this transaction would cause an increase in Revenues and a decrease in Cash.

If a company purchases treasury shares and then does not re-sell them, there would be no effect on either assets or Retained Earnings.

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), author of The Handy Financial Ratios Guide, a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website or view his author profiles on Amazon, Nasdaq and Forbes.