Work-in-Progress (WIP) Definition

Written by True Tamplin, BSc, CEPF®

Updated on June 14, 2022

Work-In-Progress (WIP) is an accounting entry on a company’s balance sheet referring to the money spent on materials, processes, and labor to manufacture a product.

It is calculated as a sum of the following three elements used to fashion a product or service: cost of materials used in the production process, labor expenses for the product as it moves through partial completion stages, and overhead costs incurred in making the final product.

For example, a restaurant uses the three cost line items mentioned above to transform raw materials, in the form of cooking ingredients, into a finished meal.

It buys vegetables, meat, and spices to prepare a meal. Labor costs for the restaurant are salaries for chefs and line (to make the dishes) and wait staff (to deliver it to customers).

To protect itself against untoward incidents and keep its workers happy, the restaurant’s owners also spend on insurance and health benefits.

The restaurant may also have capital costs like monthly rent (or mortgage) payments for its premises and maintenance on equipment used to make food. These expenses are classified as overhead.

The WIP accounting on the restaurant’s balance sheet, therefore, will be a sum of entries for the costs of cooking ingredients (once they enter the food line assembly), facility expenses, employee salaries and benefits, and insurance costs.

WIP accounting does not include costs for items that have not entered the production assembly line. For example, raw materials that are still placed in factory stores are not included in WIP costs.

WIP accounting also does not include costs for finished items, which are classified as finished goods inventory after they have moved past the production floor.

Since manufacturing is a dynamic process of multiple constantly-moving parts, it is difficult to accurately calculate and account for WIP costs for each product. Instead, companies have adopted various methods to estimate or present WIP accounting in their balance sheets.

For example, Just-In-Time (JIT) manufacturing practices emphasize the importance of keeping inventory levels to low figures or zero to ensure efficiency. By using these practices and completing their backlog of WIP items, some companies regularly move all their WIP goods to the finished goods stage before accounting.

Manufacturing outfits with predictable assembly line times present WIP items as a percentage in their accounting. They derive this percentage based on previous estimates of completion and product manufacturing times.

How Is WIP Information Useful?

WIP inventory figures are useful information to measure metrics related to the production process. This enables production managers to calibrate the output of their assembly line with market vagaries. Thus, managers can tamp down or increase production based on the availability of materials in bins on the factory floor.

WIP can also be used to determine supply chain health. Too many items classified as WIP and not as many items in the finished goods stage is a sign of inefficiency on the production floor. It also translates to additional costs on the balance sheet because WIP items incur storage and warehousing expenses. These expenses cannot be moved elsewhere or re-invested to other departments within the manufacturing setup. That is why companies aim for as low as possible WIP numbers.

WIP is often classified as a current asset on a company’s balance sheet because available WIP inventory in different stages of completion can be converted to finished goods that, subsequently, may generate a sale profit for the company. This inventory stays on a company’s balance sheet or is written off based on the duration of time it spends on the production floor.

WIP represents an intermediate stage in the production process. It comes before the finished goods stage and after the raw materials are moved to the production floor from stores. Once the product has moved past WIP, it is classified as finished goods inventory. After the product is sold, WIP cost is one among several costs that are rolled up to determine the final cost of goods sold in the balance sheet.

Example of WIP

Consider the case of television manufacturer ABC. Its raw materials consist of an assortment of electronic circuits, cathode ray tubes, displays, and packaging materials. ABC already has $100,000 worth of raw material inventory left over from the previous year and makes additional purchases of $300,000 to manufacture new television sets for this year. At the end of the year, it is left with unfinished inventory (or inventory that was left over from its planning stage) worth $150,000.

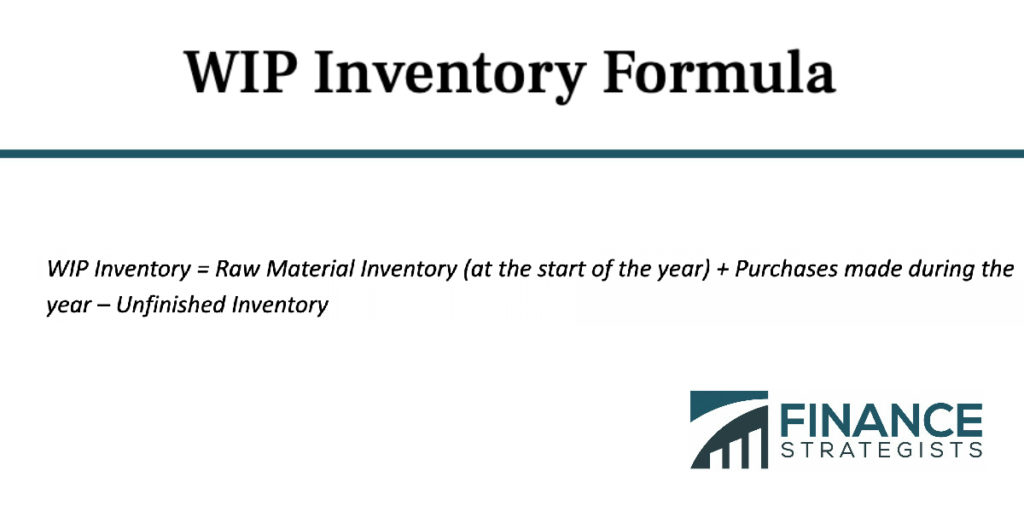

We use these three figures to calculate ABC’s raw material inventory.

WIP Inventory = Raw Material Inventory (at the start of the year) + Purchases made during the year – Unfinished Inventory

WIP Inventory for ABC = $100,000 + $300,000 – $150,000 = $250,000

ABC has five workers on its assembly line and they are each paid an annual salary of $40,000. Therefore, direct labor costs for ABC are $200,000.

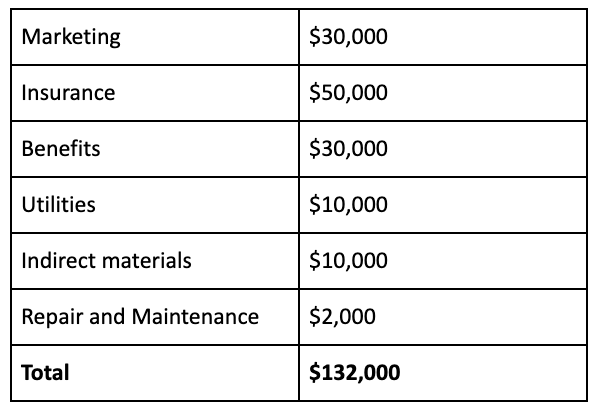

Besides these costs, ABC also incurs manufacturing overheads in the form of worker benefits, insurance costs, and equipment depreciation costs.

A full breakdown for ABC’s overhead costs is shown below:

Total WIP Costs are calculated as a sum of WIP Inventory + Direct Labor Costs + Overhead costs.

Thus, WIP costs for ABC = $250,000 + $200,000 + $132,000 = $582,000

Work-In-Progress Versus Work-In-Process

Work-In-Progress is often used interchangeably with Work-In-Process. Conceptually, both terms are similar in that they refer to the costs associated with a partially-finished good or service moving across the production floor.

But they can mean different things in specific instances. In general, Work-In-Process inventory refers to partially completed goods that move from raw materials to a finished product within a short time frame. For example, consulting and manufacturing projects often have custom requirements based on the client. The manufactured good moves through the production process in a relatively short amount of time before it is presented to the client or customer. Inventory is referred to as Work-In-Process inventory in such cases.

In contrast, Work-In-Progress refers to a production process that requires a longer time frame. Consider the situation in a construction company. The time required to make a good or product, in this case a building, is much longer and requires more material and manpower as compared to a factory or consulting project. Work-In-Progress is used in the construction industry to refer to a construction project’s costs instead of a product. The formula to calculate both terms, however, is mostly the same for accounting purposes.

More About Work In Progress

We hope this has been helpful in understanding the topic on Work In Progress. If you have any more questions, please feel free to reach out to a financial advisor in Escondido, CA. For those of you who don’t live locally, please visit our financial advisor page to connect with one closest to your area.

Work In Progress (WIP) FAQs

About the Author

True Tamplin, BSc, CEPF®

True Tamplin is a published author, public speaker, CEO of UpDigital, and founder of Finance Strategists.

True is a Certified Educator in Personal Finance (CEPF®), a member of the Society for Advancing Business Editing and Writing, contributes to his financial education site, Finance Strategists, and has spoken to various financial communities such as the CFA Institute, as well as university students like his Alma mater, Biola University, where he received a bachelor of science in business and data analytics.

To learn more about True, visit his personal website, view his author profile on Amazon, or check out his speaker profile on the CFA Institute website.