The accounting cycle begins with the analysis of transactions. The proper analysis of business transactions is important because it ensures that entries in the journal are correct.

What are the Steps of Transaction Analysis?

Analysis of business transactions involves the following four steps:

- Ascertaining the accounts involved in the transaction

- Ascertaining the nature of the accounts involved in the transaction

- Determining the effects (i.e., in terms of increases and decreases in the accounts)

- Applying the rules of debit and credit

Ascertaining the Accounts Involved

Every business transaction involves two or more accounts. The process of analyzing a business transaction starts with identifying these accounts.

For example, suppose that Mr. John starts a business with cash amounting to $25,000. This is a transaction that involves two accounts: namely, the cash account and the capital account.

Ascertaining the Nature of Accounts

The second step of transaction analysis is to ascertain the nature of the accounts identified in the preceding step. In the above example, cash is an asset account and capital is an owner’s equity/capital account. Consider learning more about the classification of accounts.

Determining the Effects in Terms of Increase and Decrease

After ascertaining the nature of the accounts, it is necessary to determine which account is increasing and which one is decreasing as a result of the transaction. This is necessary for the proper application of rules of debit and credit on each account.

In the above example, the two accounts involved are the cash account and capital account, both of which are increasing.

Applying the Rules of Debit and Credit

The final step involved in transaction analysis is to apply the rules of debit and credit on accounts.

In this step, we determine which account is to be debited and which one is to be credited on the basis of the increase and decrease in accounts identified in the preceding step.

Using the same example, the cash account would be debited because, when an asset increases, its account is debited. The other account involved is John’s capital account, which would be credited. This is because the capital account is credited when capital increases.

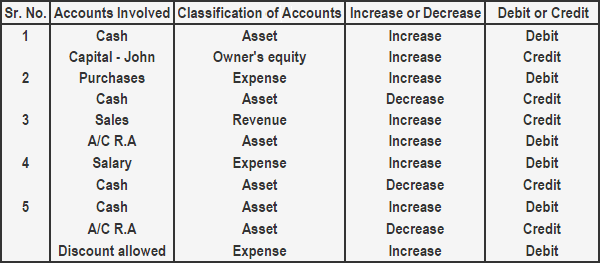

Example

Consider the following information:

- Mr. John started his business by investing $50,000

- He purchased merchandise for cash, amounting to $20,000

- He sold merchandise to Mr. Sam on credit for $5,000

- He paid an employee’s salary amounting to $700

- He received cash from Mr. Sam of $4,800 and allowed him a cash discount of $200

Required: Give a stepwise analysis of the above transactions.

Solution

Get to Know the Basics

Every recording of a business transaction entails that one should have an appropriate understanding of the nature of the transaction, the accounts affected, and the rules of debit and credit. Let us know how we could be of help in matters like this. Here’s a link to a financial advisor in Forest, VA who can assist you. If you live outside the place, please visit our financial advisor page for more information.

Do you want to test your knowledge about Transaction Analysis? We have prepared quizzes for you.