Bill of Exchange: Definition

A bill of exchange is defined as follows:

An unconditional order in writing, addressed by one person to another, signed by the person giving it, requiring the person to whom it is addressed to pay on demand or at a fixed or determinable future time a certain sum in money to (or to the order of) a specified person or to bearer.

Bill of Exchange: Key Points

To better understand the above definition of bill of exchange, the following points should be kept in mind:

Unconditional

Bearing no condition means that there is no condition attached to the bill.

Order

A bill of exchange is an order to pay certain money. It is not a request.

Giving Person

The person who makes (i.e., writes) the bill is the person who orders to pay the amount of the bill. This individual is called the drawer.

Addressed Person

The person upon whom the bill is drawn or the person to whom the order is given is known as the drawee. This individual accepts the bill by writing the word “Accepted” across the face of the bill and signing it.

On-Demand

The bill is payable whenever the amount of the bill is demanded (only in the case of sight bill).

Fixed Time

A clear and certain time in the future (e.g., 10 December 2019).

Determinable Future Time

A future time that can easily be determinable (e.g., 90 days after the date of drawing the bill).

Certain Sum in Money

The amount is payable in the form of money rather than a commodity or any other means. For example, a sum of $10,000 in money.

Payee

The payee is the person to whom the amount of the bill is paid.

The amount of the bill can be paid to the drawer, or to someone else, as per the order of the drawer or to the person who presents the bill on the due date.

This is why definition contains the phrase” to or to the order of a specified person or to bearer.”

Explanation

In this modern age of competition, credit selling is an evil that every businessperson has to engage in. This is because credit sales are one of the strongest tools to enhance net income.

The refusal to give credit means that competitors may win potential sales. However, no businessperson wants to sell goods on credit to customers who may not pay their debts.

Firstly, remember that businesspeople always seek to promote sales and, alongside this, to secure money and customers. A seller wants to realize the amount of goods sold as soon as possible, maximizing the goods sold and minimizing the chance of bad debts can be minimized.

In contrast to a seller, a buyer wants to get maximum credit period. Is there any method that satisfies both the parties? The answer is yes.

There is a payment method, known as bill of exchange, that provides the seller with evidence of amount receivables as well as the amount of goods sold. Noteworthily, this method also offers a sufficient credit period to the buyer.

The bill of exchange method of payment has several advantages compared to other methods.

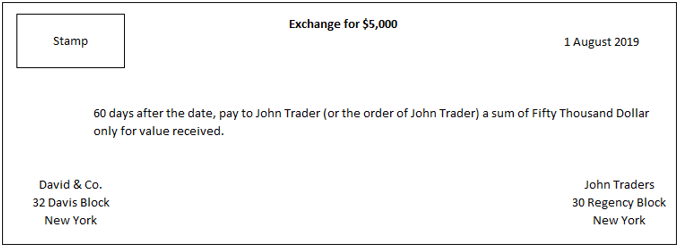

Specimen/Format of Bill of Exchange

Parties to a Bill of Exchange

There are three main parties involved in a bill of exchange: drawer, drawee, and payee.

Drawer

The drawer is the maker of the bill. They draw or writes the bill and they sign the bill. Although a bill can be accepted before receiving the drawer’s signature, their signature is required to complete the document.

Drawee

The drawee is the person upon whom a bill of exchange is drawn, or the drawee is the person who accepts the bill and promises to pay the amount. When the drawee accepts the bill, he becomes the acceptor.

Payee

The payee is the person who is named in the instrument as the individual who the amount of the bill should be directed toward to be paid. As such, the payee is the person who receives the amount of the bill.

The payee may be the drawer or someone else. If the drawer keeps the bill with themselves until the due date and receives the amount of the bill, then the drawer and payee are the same person.

There are also other parties involved in a bill of exchange, including:

- Holder

- Holder in due course

- Drawee in case of need

- Acceptor for honor

Holder of the Bill

The holder of a bill of exchange is the person who is entitled in their own name to the possession of the instrument and to receive the amount due thereon.

It is not only possession but also entitlement to possession that makes a person the holder of the bill. Thus, a person in possession of a stolen or lost bill cannot be a holder.

Holder in Due Course

Any person who, for consideration, becomes the possessor of a bill payable to the bearer is known as the holder in due course. Amy person who has received the bill from the previous holder is called a holder in due course.

Drawee in Case of Need

Sometimes, in bills of exchange, the name of a third person is mentioned. If the original drawee does not accept or pay the bill, then this third person will accept and pay the bill. This third person is known as the drawee in case of need.

Acceptor for Honor

If the original drawee refuses the bill and the holder of the bill gets the bill noted and protested due to non-acceptance, then any person who is not already liable to accept the bill may accept the bill with the consent of the holder. This person is known as the acceptor for honor.

Types of Bill of Exchange

A bill of exchange can be classified based on the following three bases:

By Time Period

- Demand Bill of Exchange

- Term Bill of Exchange

By Objective

- Trade Bill of Exchange

- Accommodation Bill of Exchange

By Territory

- Inland Bill of Exchange

- Foreign Bill of Exchange

Demand Bill of Exchange

A bill with no fixed payment date. It is payable at the time when it is presented by the holder. Days of grace are not allowed on a bill of this kind. A demand bill is also known as a sight bill.

Term Bill of Exchange

A bill drawn for a specific time period. This type of bill has either a fixed future date or determinable future time.

Trade Bill of Exchange

A bill drawn and accepted due to the sale and purchase of goods on credit. This type of bill is drawn by the creditor (seller) and accepted by the debtor (buyer).

Accommodation Bill of Exchange

A bill drawn and accepted without the sale and purchase of goods. The main purpose of this bill is to provide financial assistance to one or both parties. The bill does not come into existence due to any trading activity.

Inland Bill of Exchange

A bill drawn, accepted, and payable in the same country. Both the drawer and acceptor of this bill live in the same country.

Foreign Bill of Exchange

A bill drawn in one country and accepted and payable in another country. Both the drawer and drawee of this bill live in two different countries.

Acceptance of Bill of Exchange

The drawee is not liable to pay the bill until they accept the bill. Therefore, the drawee’s acceptance of the bill of exchange is necessary to complete the instrument.

The act of signing and writing the words “Accepted” across the face of the bill by the drawee is called acceptance. The advantage of acceptance is that it fixes the liability on the drawee.

Types of Acceptance

Acceptance is of the following two kinds:

- General acceptance

- Qualified acceptance

General Acceptance

If the bill of exchange is accepted without any condition to the order of the drawer, the acceptance is termed as general acceptance.

Qualified Acceptance

When a bill of exchange is accepted with any qualification or condition to the order of the drawer, the acceptance is known as qualified acceptance.

Qualified acceptance is separated into the following types:

- Qualification as to time

- Qualification as to place

- Qualification as to partial payment

- Qualification as to parties

- Qualification as to the condition

Tenor of the Bill of Exchange

The time period after which a bill of exchange is matured is called the “tenor” of the bill.

For example, if a 90-day bill is drawn and accepted, the bill will be matured after 90 days. So, the tenor of this bill is 90 days.

Days of Grace

In the business community, when the due date of a bill is calculated, it is customary that after maturity of the bill, three extra days are given to the drawee for the payment of the bill. These extra days are called days of grace.

Usance

Usance refers to the period of time for the payment of the bill which is fixed by the tradition of the market.

For example, consider a 90-day bill that will be matured after 90 days. Therefore, tenor of the bill is 90 days. However, three extra days will be given to the drawee for payment of the bill. Here, the usance of the bill is 93 days.

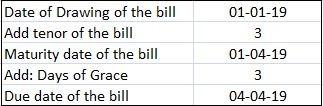

Maturity of Bill of Exchange

A term bill matures when its tenor expires. Therefore, maturity of the term bill may be defined as the end of the tenor of bill.

The date after the tenor ends is called the date of maturity, whereas the date at which the term bill becomes payable by the drawee is called the due date of the term bill. A bill becomes payable by the drawee after the days of grace.

For example, suppose a bill is drawn on 1 January 2019 for three months. Its date of maturity and due date are shown as follows:

Working of Bill of Exchange

How does a bill of exchange work? Let’s explain this with the help of a few examples.

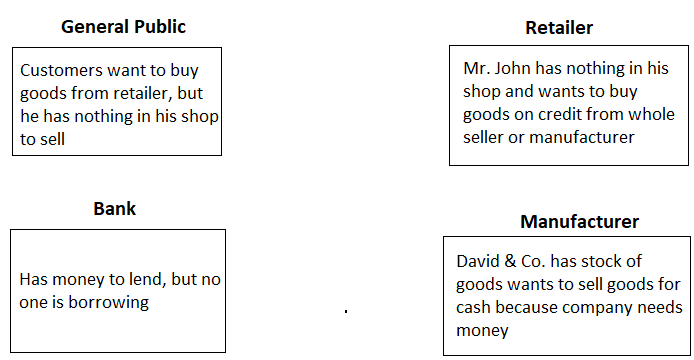

Example 1: Working Without a Bill of Exchange

The situation shown in the figure above can be understood using the following notes:

- Business activities stop because Mr. John the retailer has no money to buy goods. For his shop, on the other hand, David & Co. the manufacturer wants to sell goods for cash only.

- The problem can be solved if somehow goods are provided to the retailer on credit and the manufacturer is also paid immediately for his goods.

- A bill of exchange accepted by a reputed businessperson is also an acceptable document for the bank. The bank will easily lend money to the holder of the bill.

Now you will see how a bill of exchange helps to promote business activities.

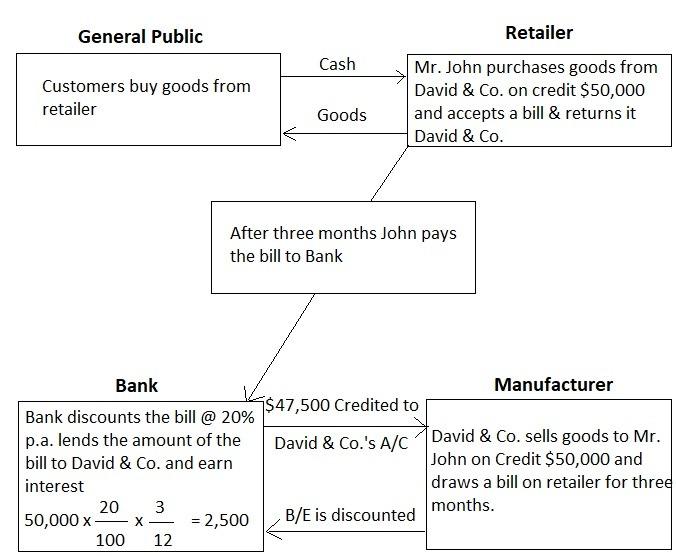

Example 2: Working With a Bill of Exchange

The following points are noteworthy in relation to this figure:

- David & Co. the manufacturer sells goods on credit to Mr. John the retailer. The retailer accepts a bill for the amount, and David & Co. gets the bill discounted and fulfills its cash needs.

- Now, the retailer has goods to sell, and he will simply pay the amount of the bill after three months.

- The bank discounts the bill and earns revenue in interest of $2,500.

This example shows how a bill of exchange helps to promote business activities.

Advantages of Bill of Exchange

The use of bills of exchange as a method of payment has several advantages compared to other methods of payment for the credit sale of goods. Some of these advantages are the following:

1. Legal evidence

A bill of exchange is a legal document; therefore, it is a legal evidence of the debt. As such, the drawer can sue for the recovery of the amount of the bill.

2. Specific amount and date

A bill of exchange is signed by both parties. For this reason, both parties are aware of the amount of the bill and its due date.

3. Discounting facility

Another advantage of a bill of exchange is that it can be discounted if the drawer or holder needs funds before the due date. The bill can be sold to the bank to receive the total amount in advance.

4. Negotiable

Negotiable means transferable. A bill of exchange payable to the bearer can be transferred by one person to another for the settlement of debt.

5. Drawee enjoys full credit period

The drawee is bound to pay the amount of the bill on the due date. They cannot be compelled to make the payment earlier. Therefore, the drawee enjoys the full credit period.

6. Change in relationship

Before a bill of exchange, the seller is a creditor and the buyer is a debtor. The bill of exchange converts this relationship into “drawer” and “drawee”.

7. Easy remittance

As bill of exchange is a negotiable instrument, just like a postdated cheque. Therefore, it can easily be remitted from one place to another, just like a cheque.

Two Aspects of Bill of Exchange

Earlier, it was mentioned that creditors (sellers) can draw a bill of exchange and become drawers. Since the amount of the bill is receivable by the drawer, the bill of exchange, from this point of view, is called the bill receivable.

On the other hand, the debtor (buyer) accepts the same bill and becomes the drawee. The amount of the bill is payable by drawee, and so from the drawee’s point of view, the bill of exchange is known as the bill payable.

Do you want to test your knowledge about Bill of Exchange? Take the Multiple Choice Questions we have prepared for you here.