What Is a Single Column Cash Book?

The single column cash book resembles a T-shaped cash account in almost all respects. The pages of this book are vertically divided into two equal parts. The receipts are entered on the left (debit) side. Payments are entered on the right (credit) side.

A single column cash book has only one money column on the debit and credit sides to record cash transactions. This is the reason why it is called a single column cash book (or a simple cash book).

Explanation

A single column cash book records only cash receipts and payments.

This form of a cash book has only one amount column on each of the debit and credit sides of the cash book. All the cash receipts are entered on the debit side, and cash payments are entered on the credit side.

In essence, a single column cash book is nothing but a cash account. A cash account cannot show a credit balance on the principle that you cannot pay what you do not have. This means that a cash account always shows a debit balance or nil balance.

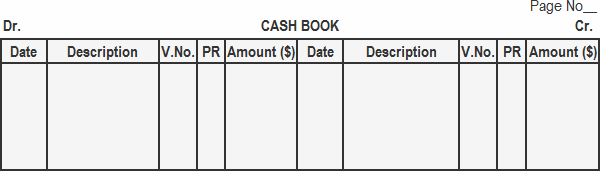

Format of a Single-Column Cash Book

The standard format of a single column cash book is shown below.

Functions of the Columns in a Single Column Cash Book

The format above consists of five columns on both sides of the cash book. The purpose/function of each column is briefly described in this section.

Date Column

The year, month, and day of the receipts and payments of cash are written in the date column on the debit and credit sides of the cash book. Don’t repeat the year and month for additional entries until a new month starts (or a new page is added).

Description Column

The description column starts with the words “balance brought down” or simply “balance.”

This column shows the cash balance at the start of the current period. After recording the opening balance in the description column, the cash transactions of the current period are recorded.

When cash is received on an account, the name of that account is written on the debit side. When cash is paid on an account, the name of the account is written on the credit side in the description column.

Voucher Number

For every entry recorded in the cash book, there must be a proper voucher.

When money is received, an original receipt is given to the payer and the payee retains a copy. This receipt is called a debit voucher because it supports the entries on the debit side of the cash book.

When a payment is made, an original receipt is obtained from the payee. This receipt is called a credit voucher because it supports entries on the credit side of the cash book.

The debit voucher’s serial number is recorded on the debit side, and the serial number of the credit voucher is recorded on the credit side in the cash book’s voucher number (V. No.) column.

Posting Reference

When entries from the cash book are posted to ledger accounts, the relevant account number is written in this column.

Amount Column

The amount column is used to enter the amount received or paid as a result of a cash transaction.

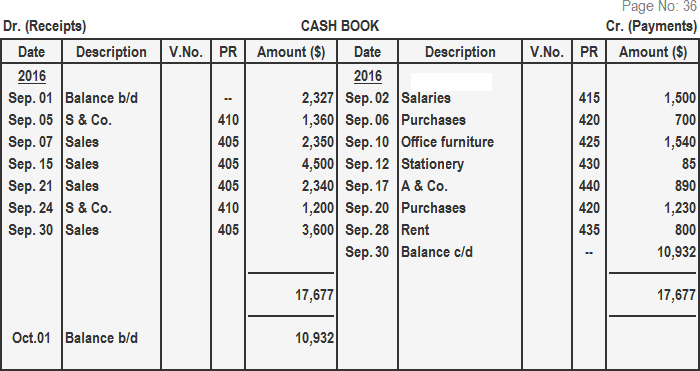

Balancing the Cash Book

At the end of the day, or at the end of the accounting period, the amount columns on both sides are totaled.

The cash column’s total on the debit side will always exceed the total of the credit side. This is because we cannot pay more cash than we have received. The difference represents the actual cash in hand, which should agree with the amount of cash in the cash box.

To make the two sides of the single column cash book equal, the difference is written on the credit side as “balance carried down” or simply “balance.”

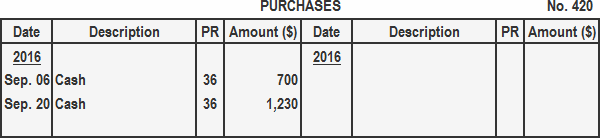

Posting the Single Column Cash Book to the Ledger

The following points should be kept in mind when posting the single column cash book to the relevant accounts in the ledger.

First, the opening and closing balances of the cash book are not posted.

Second, the items on the debit side of the cash book are posted to the credit sides of the accounts in the ledger, and the respective account numbers are entered in the posting reference column of the cash book.

Finally, the items on the credit side of the cash book are posted on the debit sides of the accounts in the ledger, and the respective account numbers are entered in the posting reference column of the cash book.

Example

Record the transactions shown below in a single column cash book and post to the ledger.

For the year 2016, the transactions are as follows:

- Sep. 01: Cash in hand (balance b/d) $2,327

- Sep. 02: Paid salaries for August $1,500

- Sep. 05: Cash received from S & Co. $1,360

- Sep. 06: Purchased merchandise for cash $ 700

- Sep. 07: Cash sales for the first week $2,350

- Sep. 10: Paid cash for office furniture $1,540

- Sep. 12: Purchased stationery for cash $85

- Sep. 15: Cash sales for the second week $4,500

- Sep. 17: Cash paid to A & Co. $890

- Sep. 20: Purchased merchandise for cash $1,230

- Sep. 21: Cash sales for the third week $1,200

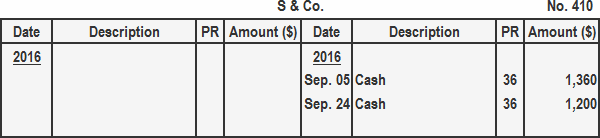

- Sep. 24: Cash received from S & Co. $1,200

- Sep. 28: Paid office rent $800

- Sep. 30: Cash sales for the last week $3,600

Solution

Cash Book

General Ledger

Ledger For Accounts Receivable

Ledger For Accounts Payable