Profits or losses made by a firm should be divided among its partners per the provision of their partnership deed. However, if there is no written or oral agreement among the partners, the law prescribes that partners should share profits and losses equally.

Under the law, no partner is entitled to get anything out of their firm except a share in profits.

Thus, whatever benefits or allowances the partners may be entitled to by the provisions of their partnership deed must be given to them out of the firm’s profits only.

This statement implies that no allowance or benefit allowed to a partner can be debited to the firm’s profit and loss account.

If one of the partners is active and their partnership deed allows them a salary of, say, $600,000 per annum, this sum cannot be debited to the profit and loss account as an expense.

The law does not recognize any payment made to a partner by their firm as an expense.

At the end of each financial year, after the firm’s net profit (or loss) has been ascertained, i.e., after the firm’s trading and profit and loss account (or income statement) has been prepared, the profit and loss appropriation account is readied.

The profit and loss appropriation account indicates the distribution of profit or loss among the partners.

Net profit is transferred from the profit and loss account to the profit and loss appropriation account by:

- Debiting the profit and loss account

- Crediting the profit and loss appropriation account

In case of a net loss:

- The profit and loss appropriation account is debited

- The profit and loss account is credited

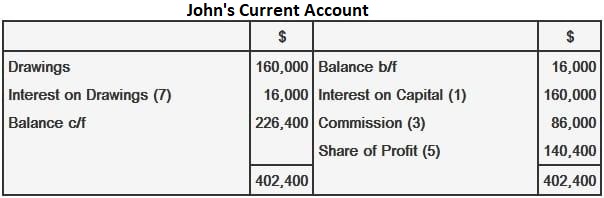

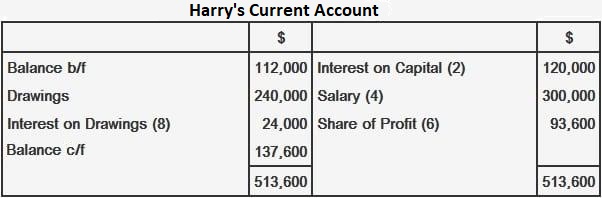

Any benefit or allowance made to a partner (e.g., interest on fixed capitals, salary, commission, bonus, and so on) is:

- Debited to the profit and loss appropriation account

- Credited to the current account of the relevant partner

Any charge made by the firm on the partners (e.g. ,interest on drawings) is:

- Debited to the current account of the relevant partner

- Credited to profit and loss appropriation account

Following the above adjustments, the balance left on the profit and loss appropriation account represents a distributable profit or loss. If the balance is a credit balance, it is a distributable profit which is:

- Debited to the profit and loss appropriation account

- Credited to the current accounts of the partners in their agreed profit and loss sharing ratio

If the balance left on the profit and loss appropriation account after the various appropriations is a debit balance, it is a distributable loss which should be:

- Debited to the current accounts of partners in their agreed profit and loss sharing ratio

- Credited to the profit and loss appropriation account

Example

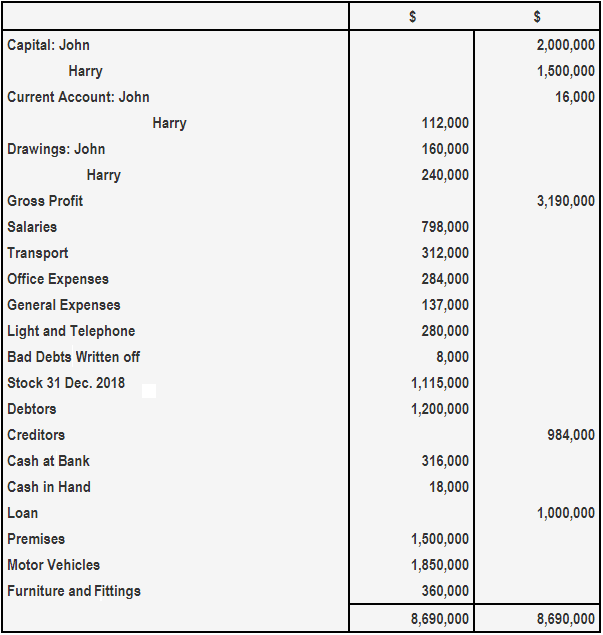

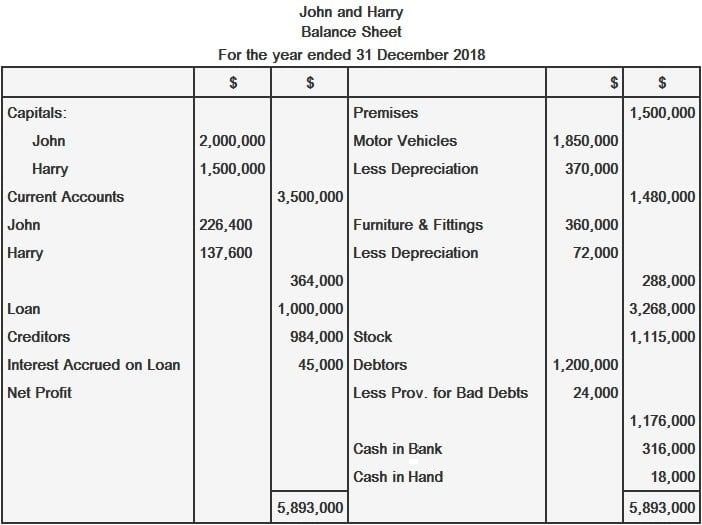

The balances left in the ledger of John and Harry after they prepared their trading account for the year ending 31 December 2018 are given below. Based on these balances and additional information, prepare:

- The firm’s profit and loss account for the year 2018

- The firm’s profit and loss appropriation account for the same year

- The partners’ current accounts, in ledger form

- The firm’s balance sheet on 31 December 2018

Additional Information

- 20% depreciation is to be provided on motor vehicles, furniture, and fittings

- A provision for bad debts is to be created at 2% of debtors

- The loan was acquired on 1 July 2018 and carries 9% interest. No interest payment has been made in the year

- John is entitled to 10% of net profit as commission, while Harry is entitled to a monthly salary of $25,000

- 8% interest is to be allowed on fixed capitals, and 10% interest is to be charged on drawings

- The balance of the profit or loss is to be shared in the ratio of 3:2 between John and Harry

Solution

Preliminary Calculations

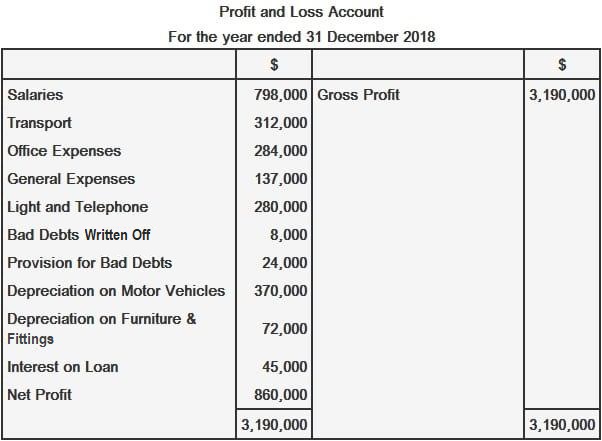

Depreciation on motor vehicles: 20% on $1,850,000 = $370,000

Depreciation on furniture and fittings: 20% on $360,000 = $72,000

Provisions for Bad Debts: 2% of $1,200,000 = $24,000

Interest on Loan (for half a year): 1/2 x 9% of $1,000,000 = $45,000

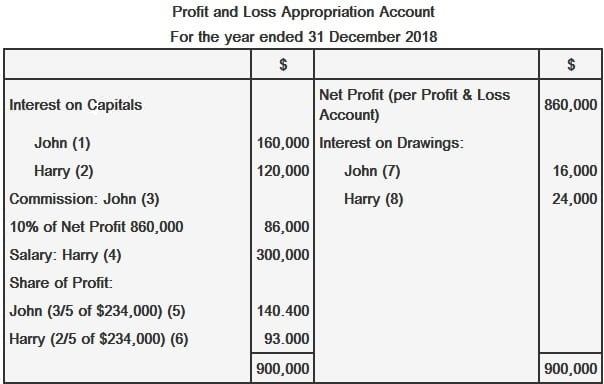

Interest on Capitals: John: 8% of $2,000,000 = $160,000.

Harry: 8% of $1,500,000 = $120,000.

Interest on Drawings: John: 10% on $160,000 = $16,000.

Harry: 10% on $240,000 = $24,000.

Harry’s Salary: $25,000 per month x 12 = $300,000 for the year.

Team Up with the Specialists

We hope this article has been a useful resource in explaining the subject on the distribution of profit in a partnership. Let us know where else we could help. Contact a financial advisor in Newport Beach, CA today or scan through our financial advisor page if you don’t live within the locale.